The ripple effects from the US Presidential elections are still being felt. In terms of financial releases, we make a start on Monday, with Germany’s Ifo figures for November. On Tuesday we get the US Consumer confidence figure for November. On Wednesday, we get Australia’s CPI rate, the UK’s nationwide house prices rate for November, the US core durable goods orders rate for October, the US revised GDP rate for Q3, the US weekly initial jobless claims figure and the US Core PCE rates for October. On Thursday, we get the Eurozone’s final consumer confidence figure, followed by Germany’s preliminary HICP rates for November. Lastly, on a busy Friday we get Japan’s unemployment rate for November and unemployment rate for October, followed by Japan’s preliminary industrial production and retail sales rates for October, Turkey’s GDP rate for Q3, France’s final GDP rate for Q3 and preliminary HICP rate for November, Switzerland’s KOF indicator figure for November, the Czech Republic’s final GDP rate for Q3, Germany’s unemployment rate for November, the Eurozone’s preliminary rate for November and finally Canada’s GDP rate for Q3. On a monetary level, we would like to note the release of the FOMC’s November meeting minutes on Tuesday and New Zealand’s interest rate decision on Wednesday

USD – Inflation data to provide the Fed with the excuse to remain on hold?

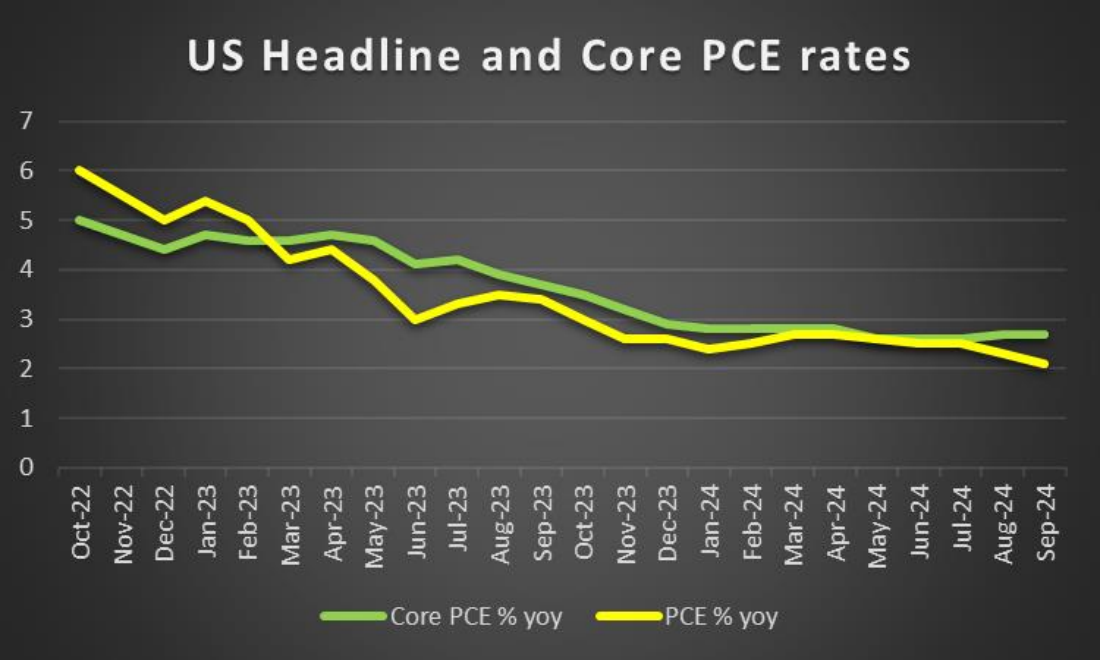

Fundamentally for the USD, the impact from the US Presidential election is still being seen, as the incoming administration’s cabinet is still being formed. In particular, the position of Treasury Secretary has yet to be decided and could by itself impact the dollar’s direction given the cabinet position’s significance. Moreover, the President-elect’s economic policies appear to have the Fed gearing up for an upward battle, as the risks of inflationary pressures appear to be increasing which in turn could lead to a pause in the Fed’s monetary policy easing cycle. In particular, we are referring to the comments made last week in which Fed Chair Powell stated that “the economy is not sending any signals that we need to be in a hurry to lower rates”. Moreover, the preliminary Atlanta FedGDPNow rate for Q4 came in better than expected at 2.6% implying a continued economic expansion in the US economy which could further enhance Fed Chair Powell’s comments last week. Nonetheless, the key test for dollar traders will be the flurry of financial releases from the US next week, with a heavy emphasis being placed on the release of the US Core PCE rates, where should inflationary pressures remain persistent or even accelerate, it may provide the Fed with some leeway should the wish to remain on hold in their final meeting of the year and vice versa. In our view, we would not be surprised to see the Fed remain on hold and should the Core PCE rates showcase stubborn inflationary pressures it may provide the Fed with the excuse to do so, given the increased inflationary risks of the incoming administration’s economic policies. Lastly, dollar traders may also look forward to the release of the FOMC’s last meeting minutes next week, in which we would not be surprised to see policymakers opting for a more gradual rate cutting approach.

GBP – UK Inflation worries

On a macro level we highlight the release of the UK’s CPI rates for October on Wednesday which came in higher than expected at 2.3% versus the expected rate of 2.2% and even higher than the prior rate of 1.7%. The hotter-than expected inflation print showcased an acceleration of inflationary pressures in the UK economy, which may increase pressure on the BoE to withhold from aggressively cutting interest rates in their next meeting. On the other hand, the preliminary manufacturing PMI figure for November which was released earlier on today, showcased a widening contraction of the UK manufacturing sector. In turn this may be of concern for the BoE as should the economic situation deteriorate they may opt for a more “dovish” approach. On a political level, with the Labour Government’s decision to increase employment national insurance payments, the BoE may take a more cautious approach to it’s monetary policy path,as was stated earlier on this week from BoE Governor Bailey who stated that “a gradual approach to removing monetary policy restraint will help us to observe how this plays out”. Overall, it appears that the BoE is concerned and may wish to take a breather from cutting interest rates, in an attempt to assess the true impact on the UK economy from the Governments recent announcements, yet a flailing economy may force the BoE’s hand. In our view, we would not be surprised to see the BoE adopt a wait-and-see approach, which may have been enhanced following the hotter-than-expected inflation print earlier this week.

JPY – To hike or not to hike?

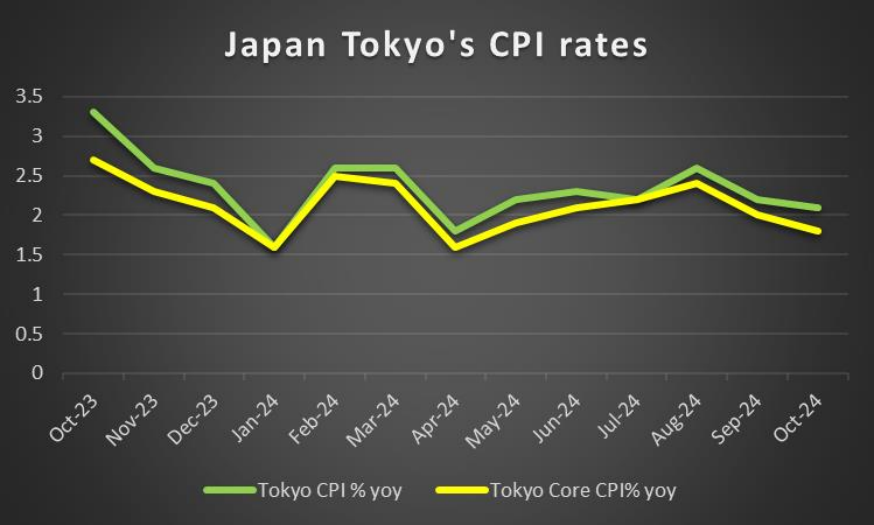

The BOJ appears to be facing a dilemma, which is whether the bank should hike interest rates or remain on hold during their next monetary policy meeting. It appears that BOJ Governor Ueda is also facing the particular predicament, as he stated earlier on Thursday that “It’s impossible to predict the outcome of the meeting at this point” and went on to say that “The next meeting is December, but there’s still a month to go. The vast amount of data and information will become available between now and then.” Essentially BOJ Governor Ueda is implying that the decision by the bank on whether or not to hike could be decided during the meeting and that the bank itself is still currently unsure as to which path they should take. On a macroeconomic, level we would like to note Japan’s trade balance figure for October which came in lower than expected, yet when looking at the improved export rate which came in at 3.1% versus the expected 2.2%, it may provide some positive indications for the Japanese economy. Moreover, Japan’s Core CPI rate for October which was released earlier on today came in hotter than expected, which may aid the JPY, as it may tilt the scales slightly in favour of a more restrictive monetary policy approach by the bank. Furthermore, we would also like to note that Japan’s Tokyo CPI rates are set to be released next week, where should it be seen that inflationary pressures are increasing, it may further tilt the balance in favour of the hawks within the BOJ, as a more restrictive monetary policy stance may be seen which in turn may aid the Yen. On the flip side, should the Tokyo CPI rates showcase easing inflationary pressures it may have the opposite effect and thus could weigh on the JPY.

EUR – Steady is the ship of inflation in the Zone

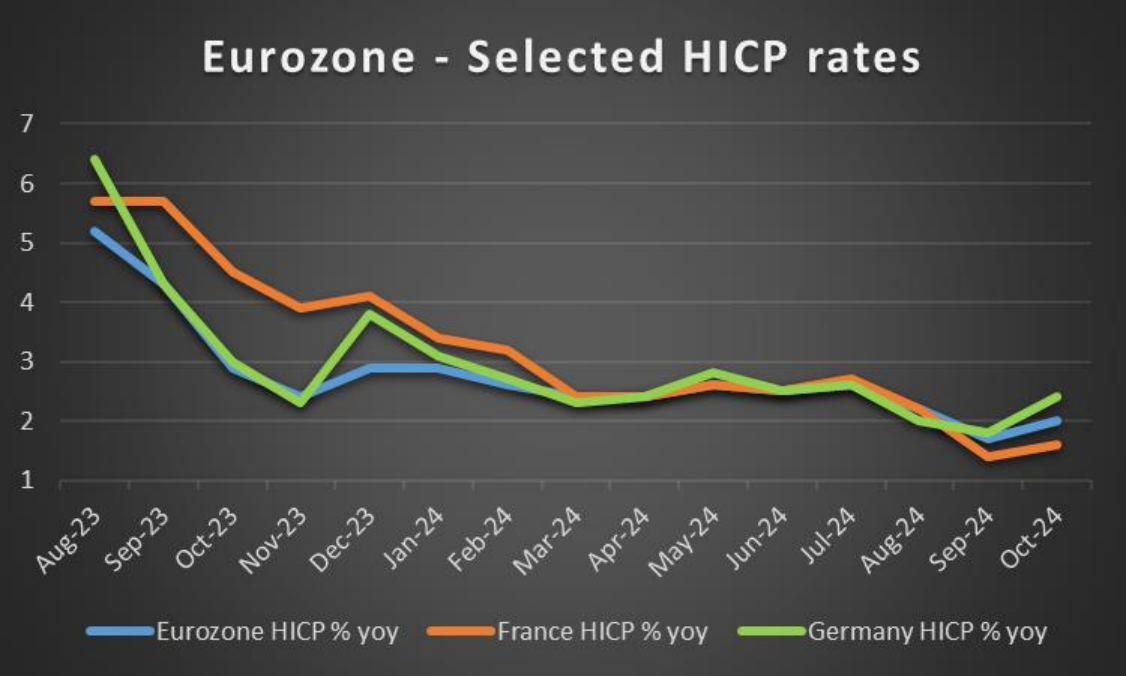

The USD is continuing is strengthening against the EUR with some analysts continuing to highlight the possibility of the pair reaching parity levels. On a political level, there a widespread concerns that the war in Ukraine is entering a new phase, with Russia having altered its Nuclear doctrine and having launched the first ICBM to be used in war against Ukraine per Kyiv. An ICBM has been traditionally designed to deliver long-distance nuclear strikes and thus its significance in being used in a conventional war cannot be overstated. In turn, the turning of the page of the war in Ukraine, may cause widespread concerns for the Zone and thus could weigh on the EUR in turn. On a monetary level, we would like to point out the comments made by ECB President Lagarde that “we are breaking the neck of inflation” which tends to imply that inflationary pressures in the Zone may be on the decline and thus could allow the bank to continue on their monetary policy easing path. On a macroeconomic level, we would like to note that the preliminary HICP reading for the Zone for the month of October are due out next Friday and thus should the inflation print remain steady as did the headline rate which was released earlier on this week, we may see ECB policymakers adopting a more dovish approach. Whereas should the HICP rates showcase an acceleration of inflationary pressures, we may see policymakers showcasing some hesitancy to continue cutting rates which in turn could aid the EUR. In our view, the Zone may be left with little to no choice but to continue on their monetary policy easing path, as concerns about the overall resiliency of the bloc are now being thrust into the spotlight.

AUD – RBA’s meeting minutes could generate interest for Aussie traders

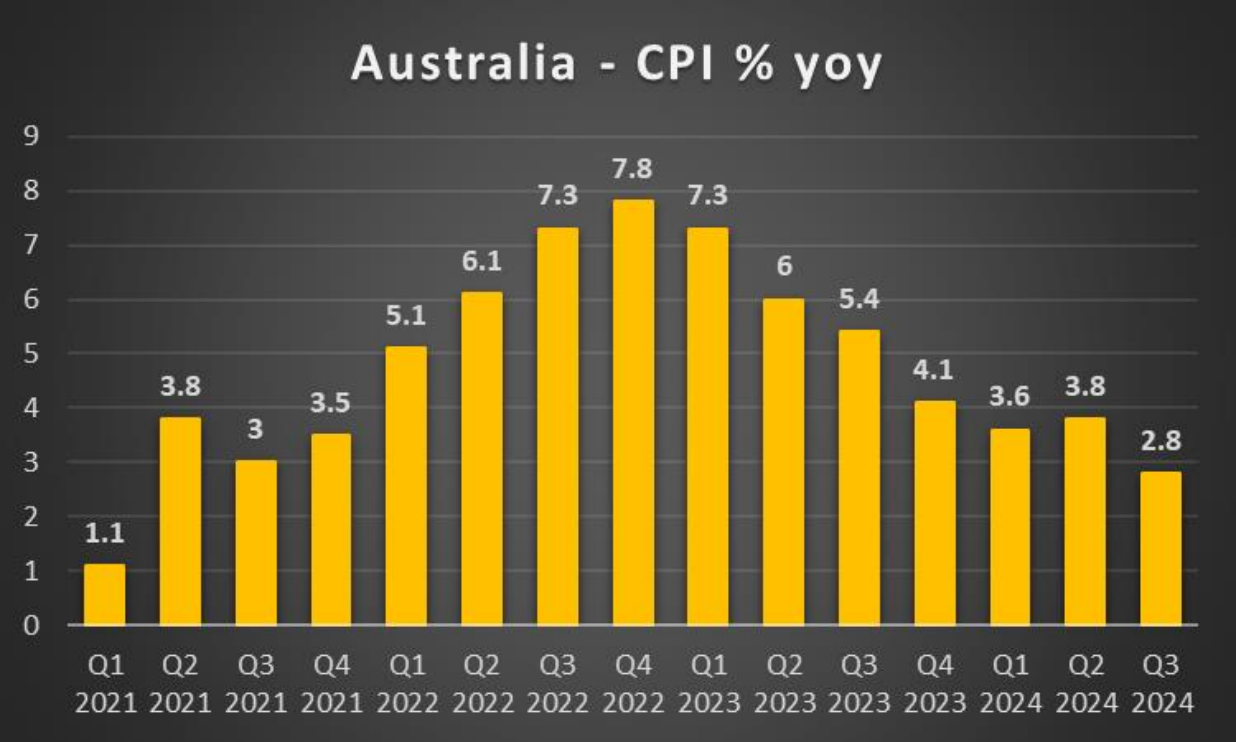

The calendar of economic releases this week was rather empty for Aussie traders, hence heavier emphasis may have been placed on the RBA’s last meeting minutes. In the RBA’s meeting minutes, policymakers stated that “members recognized it was important to be ready to adjust the future stance of monetary policy as the economic outlook evolves. Members therefore considered the conditions that might warrant either a future change in the cash rate target or a decision to hold it at its present level for a prolonged period”. Essentially the RBA’s meeting minutes may have implied that the bank may keep interest rates higher for longer, which may have aided the Aussie. On a macroeconomic level, the nation’s CPI rate for October is set to be released next week, and thus could also influence the direction of the RBA’s tone until the end of the year. In particular, should the CPI rates accelerate thus implying a persistent of inflationary pressures in the Australian economy, calls for the bank to remain on hold may increase which may aid the AUD. On the flip side, should inflation showcase easing inflationary pressures it may increase pressure on the RBA to change its tone, which may imply future rate cuts and thus may weigh on the AUD.

CAD – The sting of October’s CPI rates for Canada

On a macroeconomic level, Canada’s CPI rates for October which were released earlier on this week came in hotter than expected, implying a persistence of inflationary pressures in the Canadian economy. The hotterthan-expected inflation print may increase pressure on the BoC to remain on hold in their next monetary policy meeting and thus may have aided the Loonie during the week. Moreover, we would not be surprised to see BoC policymakers implying that the bank may need to take a pause to ensure that inflation does not spiral out of control and that the current levels may be sufficiently restrictive. In turn, this may be perceived as hawkish for the CAD which may aid the currency. However, traders may be looking towards next week’s financial release of Canada’s GDP rate for Q3. Should the GDP rate come in higher than the previous reading, it may imply economic growth in the Canadian economy and thus with an uptick in inflation, the bank may opt to withhold from further cutting interest rates. On the flip side should the GDP rate come in lower than the prior rate, it may imply economic weakening which may prove to be a thorn in the bank’s side.

General Comment

As an epilogue, normally we should expect the influence of the USD over the FX market to increase given the number and gravity of high impact financial releases from the US is increasing. Nonetheless, with the incoming administration’s cabinet positions still being decided we expect interest to be maintained about what’s ongoing in the US on a fundamental basis. As for gold we would like to note that with Russia having fired the first ICBM in a conventional war, the war has turned a page and the geopolitical risks may be funneling safe haven inflows into the precious metal.

اگر در مورد این مقاله سوال یا نظر ی کلی دارید، لطفاً ایمیل خود را مستقیماً به تیم تحقیقاتی ما بفرستیدresearch_team@ironfx.com

سلب مسئولیت:

این اطلاعات به عنوان مشاوره سرمایه گذاری یا توصیه سرمایه گذاری در نظر گرفته نمی شود ، بلکه در عوض یک ارتباط بازاریابی است. IronFX هیچ گونه مسئولیتی در قبال داده ها یا اطلاعاتی که توسط اشخاص ثالث در این ارتباطات ارجاع و یا پیوند داده شده اند ندارد.