Market worries for a US default on a fundamental level, tend to have been alleviated as we glance into what next week has in store for the markets. On the monetary front, we note the release of New Zealand’s RBNZ interest rate decision and highlight the release of the FOMC May meeting minutes, both due out on Wednesday. On Thursday, we also note the Turkish Central Bank’s monetary policy meeting. As for financial releases, we make a start on Monday with Japan’s Machinery Orders for March followed by the Eurozone’s Preliminary consumer confidence figure for May. On Tuesday, we get the preliminary PMI figures for Australia, Japan, Germany, France, the Eurozone, the UK and the US for May. On Wednesday, we note New Zealand’s retail sales for Q1 followed by UK’s CPI rates for April and Germany’s IFO figures for May. On a crucial Thursday, we make a start during the European session with Germany’s Gfk Consumer sentiment for June followed by Sweden’s unemployment rate for April and France’s Business manufacturing climate for May and during the American session we note Canada’s business barometer figure for May and we highlight the US GDP 2nd estimate rate for Q1 and the preliminary Core PCE prices for Q1. Lastly, on Friday, we note Japan’s Tokyo’s CPI rates for May, followed by Australia’s final retail sales rate for April and during the European session we note the UK’s retail sales for the same month and we highlight the US final University of Michigan consumer sentiment figure.

USD – US sings kumbaya as a debt ceiling deal nears

The USD seems about to end the week higher against its counterparts. On a fundamental note, we highlight the positive developments made by legislative leaders during this week, in regards to raising the US debt ceiling. Following the meeting between President Biden, House and Senate leadership at the White House this Tuesday, leaders from across the aisle have made key comments to the press that there has been some progress and that they would not allow the US to default. On the monetary front, we note that we had a number of Fed policymakers in the past days making statements and more or less all of them tended to lean on the hawkish side, with some forecasting that rates are to remain at high levels and no rate cuts are on the horizon, while others stated that they would feel comfortable with more rate hikes. On a macroeconomic level, we note the fact that the US retail sales growth rate on a mom level for April accelerated yet did not meet market expectations as it would appear that perhaps the consumers are

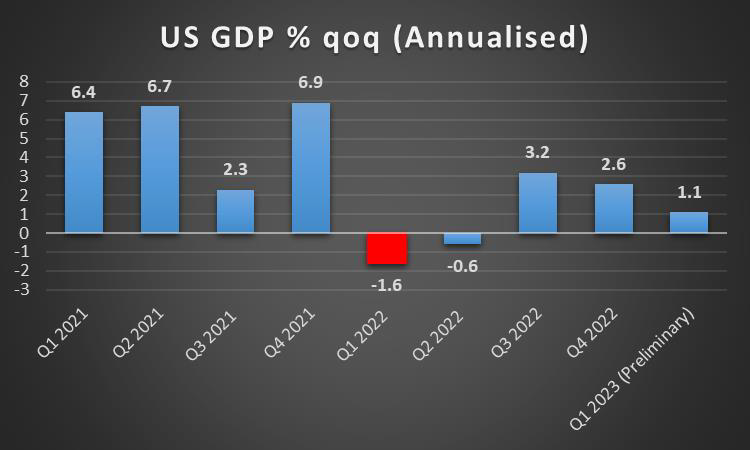

slowly feeling the impact of continued high-interest rates, eating away at their disposable income that had been accumulated for the past two years due to the covid restrictions. We also got some positive data from the production side of the US economy as the industrial output growth rate accelerated as well for April, surpassing market expectations. However, traders will most likely be placing heavy emphasis on next week’s 2nd GDP estimate for Q1. Hence should market worries for a possible default of the US government continue to subside we may see the USD gaining, as it could also in the case of the Fed maintaining its hawkish approach. Hence we highlight the release of the Fed’s meeting minutes on Wednesday.

GBP – BoE warns for further rate hikes

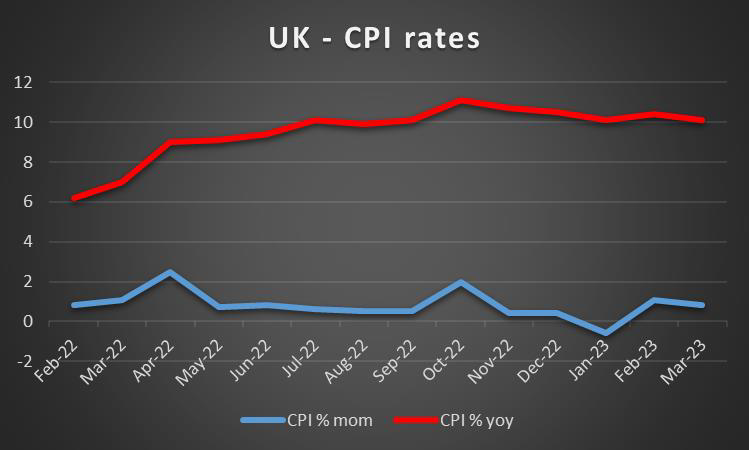

The pound is about to end the week higher against the Yen and the euro, yet lower than the dollar. On a fundamental note, we note the blow towards the London stock exchange as the UK loses its financial markets appeal. Also, we note that the UK Government is trying to open new trading routes for the economy and that is evident from the negotiations with Switzerland for new trading conditions as well as the agreement for new defence and economic deals with Japan. However, we would like to see more concrete evidence to be persuaded on a fundamental level that Brexit is to be beneficial for the UK on a macro level. On a monetary level, we highlight BoE Governor Bailey’s statements on Wednesday, who for the first time acknowledged that the UK is facing “second-round effect” in regards to inflationary pressures still persisting in the economy. Furthermore, Governor Bailey addressed comments made by fellow colleague Silvana Tenreyro, implying that MPC Member Tenreyro’s models were slightly flawed. Please note that MPC Tenreyro will be replaced with Economist Greene and as such her vivid dovish commentary may not be reflected in the next meeting. Lastly, Governor Bailey indicated a strong willingness to continue hiking rates in order to combat the “second round” of inflationary pressures on the UK economy, which may provide support for pound traders. On a macroeconomic level, we note the Unemployment rate for March which actually ticked up, while the average earnings growth rate ticked down to 5.8% yoy. Nevertheless, BoE Governor Bailey had attributed the “second-round effect” to persistently tight labour markets and high wages, implying that the UK employment market may have to loosen up. Given the importance of the cost of living crisis in the UK, we highlight the release of UK’s CPI rates, which are

expected to fall sharply according to BoE. A possible failure of the rates to slow down could provide substantial support for the pound.

JPY – JPY faces safe haven outflows

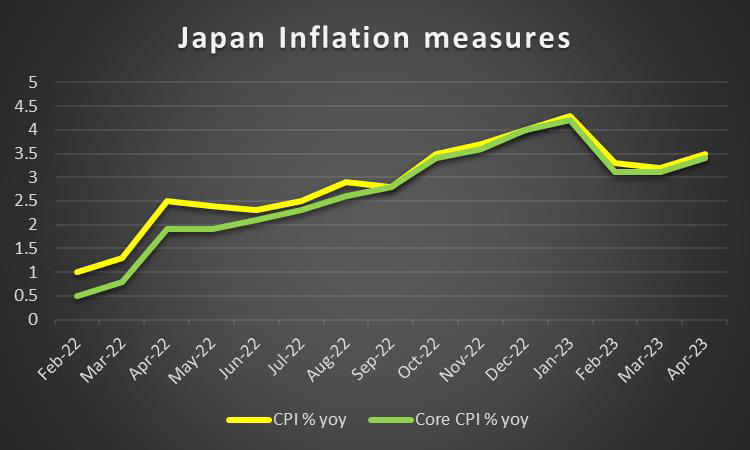

The JPY is about to end the week in the reds against the common currency the pound and the greenback. Fundamentally, the Yen is experiencing safe haven outflows as the potential constitutional crisis in the US appears to have been avoided with the nation’s leadership appearing to make progress on raising the debt ceiling, thus alleviating the risk of a US default and the US President potentially invoking article 14. On a macro level, we note the release of Japan’s Preliminary GDP rates for Q1, indicative of the economy growing at a faster pace than predicted. The faster-than-anticipated rate could support the Yen in the long run, as the Japanese economy appears to be resilient to external shocks and that the current path of the BoJ appears to be yielding positive results. At this point, we note the persistent ultra-dovish stance of the bank despite the acceleration of Japan’s CPI rates for April. However, what was also interesting was the release of Thursday’s export data on a yoy basis for April which increased at a relatively slower rate than what was anticipated, potentially hinting at some long-term issues should Japan’s exports continue to decline at this rate. Despite the Trade Balance improving, the data indicates that the positive result was due to the rate of imports decreasing at a much larger rate, rather than an increase in exports which could foreshadow an economic downturn in the long run.

EUR – EU Economic outlook boosted as the area is expected to grow

The common currency weakened against the dollar and the pound but gained against the yen. Fundamentally, we note that the protests in France against President Macron’s Government, appear to have finally subsided or are not as vocal as they were at the start of the month. Hence the lack of news or coverage, may signal a return to normality for one of Europe’s largest economies. On a monetary front, we highlight the release of ECB’s Vice President De Guindos whose rhetoric appeared to edge slightly on the dovish side, stating that “There is still scope to keep raising rates. But most of the tightening has already been done”. Implying that there is still a cause for raising interest rates, yet it is possible that the bank may remain on hold sooner rather than later. This could potentially weaken the common currency as market analysts begin to anticipate a greater

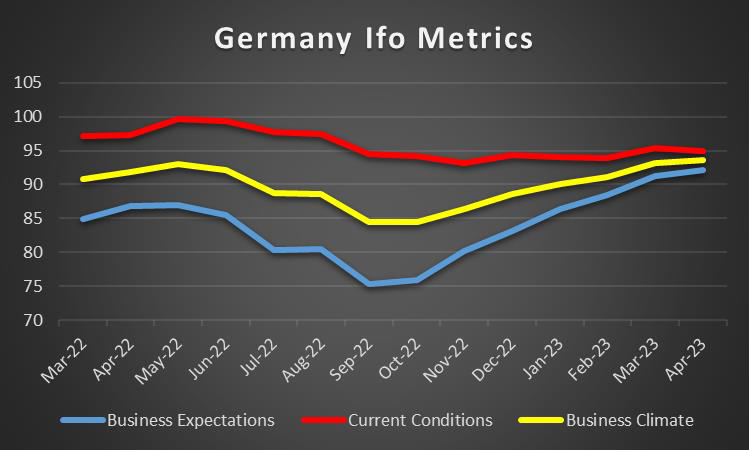

possibility of the bank remaining on hold. For the time being, we expect the bank to hike rates twice in the next meetings and remain on hold from September onwards. On a macro outlook, we note the release of the EU’s 2023 Spring economic forecast which highlights an improved economic outlook for the euro area. The EU Commission argues that the euro area has avoided a technical recession as the revised GDP growth figure now stands at 1.1% for 2023 and 1.6% for 2024. Furthermore, the commission claims that despite core inflation being revised higher, it is expected to gradually decrease having potentially peaked in the first quarter as was previously anticipated. Leading to the common currency potentially gaining in the long run should Germany’s IFO surveys and consumer confidence due out next week, reflect the positive economic sentiment seen in the Eurozone’s economic forest. We also consider as critical, the faster expansion of economic activity, hence we highlight the release of the area’s preliminary PMI figures, with special attention being placed on the “problem child” which is the reading for Germany’s manufacturing sector.

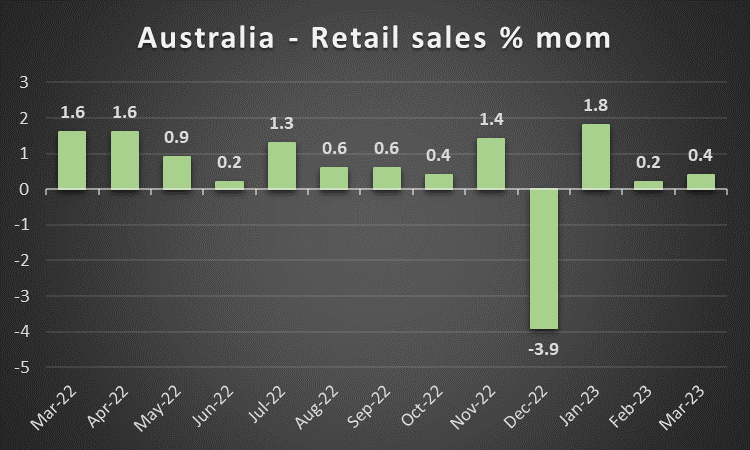

AUD – RBA minutes suggest potential hikes in the future, yet data implies that may not be the case

The Aussie appears to remain unchanged against the USD as the week draws to a close. On a fundamental note, we note the cancellation of the meeting between Japan, India, Australia and the USA, otherwise known as the “Quad Summit” following President’s Biden announcement to cut his trip short. On a monetary note, we note that the release of RBA’s May meeting minutes on Tuesday which were hawkish in nature. Within the meeting minutes, it could be deduced that the rationale behind the RBA surprising markets with a 25 basis point hike in early May, was in part to avoid any “upside surprises to inflation”. This would suggest that the Bank may continue raising interest rates, as it was implied that a tight labour market also aided to the persistent inflationary pressures. Yet, on a macroeconomic level, we note that Australia’s Employment change figure for April was in the negatives, despite market expectations of a positive figure which in addition to the Unemployment rate rising may force the bank to ease on its hawkishness. As such we may see monetary policy outlook differentials weighing on the Aussie as the bank may pause its interest rate hike path. Lastly, traders may set their sights on Monday’s Judo Bank preliminary manufacturing PMI, as it may provide some indication as to the industrial resilience of Australia’s economy.

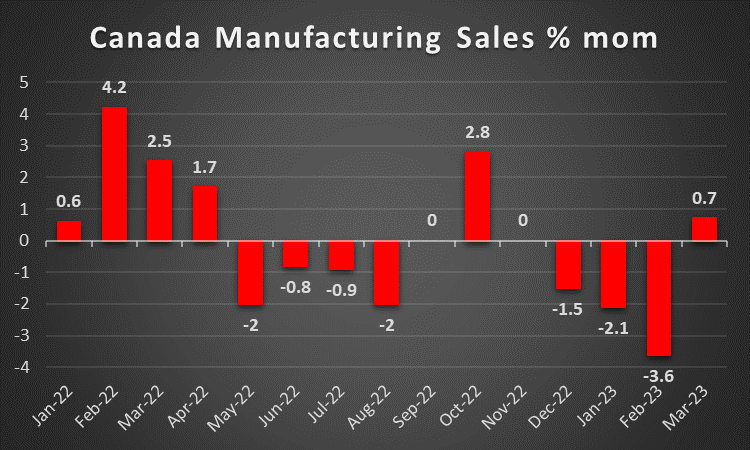

CAD – Alberta wildfires in the spotlight for the Loonie

The Loonie appears at the time of this report, to have gained against the dollar for the week. Fundamentally we note that the wildfires in the Alberta region, as was mentioned in last week’s report are continuing with news agencies reporting 92 active wildfires with 27 of them being out of control since Wednesday. According to news articles, companies have been forced to reduce Oil and Gas production as a precaution to the wildfires, which may lead to oil and gas prices spiking up, as the region remains under the “extreme” or “very high” wildfire warnings system. Hence should the issue persist we could see the CAD weakening should the reduction in oil production outweigh the gains made by possible higher oil prices, as Canada is heavily reliant on its Oil exports. On a monetary tone, we note BoC Governor Macklem’s speech on Thursday, at which he stated that it’s still too early to be thinking of interest rate cuts and noted the bank’s concerns for households facing financial pressures. Yet BoC’s Governor also stated that he expects inflation to continue to ease and avoided to lock-in another rate hike. Furthermore, we note the BoC’s Financial system review which highlighted potential risks surrounding Canada’s exposure to foreign banking sectors and as such should be monitored closely, despite being limited. On a macroeconomic level, we note the higher-than-expected headline CPI rate for April, indicative of inflationary pressures in the Canadian economy. However, the Core CPI which is predominantly the favorite inflationary measure for central banks, ticked down for the month of April, implying that underlying inflationary pressures are easing on the economy and that the headline CPI rate is lagging behind due to high energy prices. Thus we may see the CAD weakening in the long

run as the markets may begin to hesitate about future rate hikes by the bank. For the time being the market expects the bank to proceed with another rate hike before remaining on hold again.

General Comment

As a general comment we expect, due to the high number of financial releases as well as monetary policy speakers to keep traders on edge due to the high impact and frequency of the speeches with the possibility to overturn previous market sentiments on a day-to-day basis. Also given that the majority of companies have already released their financial earnings for Q1 we have a relatively quiet earnings week with no major releases expected. On a macroeconomic level, US stock market participants have gained this week, with all three major indexes gaining as the probability of a US default has significantly declined, yet not removed from the equation just yet as a deal has not been made. Furthermore, gold’s price seems about to end the week lower. The shiny metal may have seen safe haven outflows as no major releases surrounding potential bank crashes have emerged, in addition to the greenback receiving a boost of confidence from traders, as the risk of a default has been reduced, have led to the precious declining.

اگر در مورد این مقاله سوال یا نظر ی کلی دارید، لطفاً ایمیل خود را مستقیماً به تیم تحقیقاتی ما بفرستیدresearch_team@ironfx.com

سلب مسئولیت:

این اطلاعات به عنوان مشاوره سرمایه گذاری یا توصیه سرمایه گذاری در نظر گرفته نمی شود ، بلکه در عوض یک ارتباط بازاریابی است. IronFX هیچ گونه مسئولیتی در قبال داده ها یا اطلاعاتی که توسط اشخاص ثالث در این ارتباطات ارجاع و یا پیوند داده شده اند ندارد.