The earnings season has kicked off, while the message of the Fed for fewer rate cuts and rates remaining high for longer seems to have started to impact the markets, and Elon Musk seems to have made some comments that make Tesla shareholders feel awkward. In this equities report, we are to discuss the earnings released from big banks, the Fed’s message, and Tesla’s updates, and for a rounder view, conclude with a technical analysis of the S&P 500.

The earnings of big banks

One of the highlights of the past few days may have been the release of the earnings and equities reports of big US banks. We make a start by noting that JPMorgan (#JPM) and BlackRock (#BLK) reported better than expected earnings per share (EPS) and revenue figures than expected. Bank of America (#BAC) missed its revenue target, while Wells Fargo (WFC) missed its earnings target. Even worse, we note that Citigroup (#C) reported a negative EPS figure and a lower-than-expected revenue figure, creating worries among investors about its outlook.

On an annual level, we note that Morgan Stanley (#MS) and Goldman Sachs (#GS) have reported the lowest level of profitability in four years, highlighting the downsizing of investment banking in the past year. It should be noted, though, that despite the disappointment at an annual level, on a quarterly level, Goldman Sachs outperformed both the EPS and the revenue figure expectations of the market, which may imply a rebound for the investment bank. In an aggregated manner, the releases tend to send mixed signals about the situation in the US banking sector and the conditions in the US financial environment, which more or less failed to excite traders and lead the markets to a more risk-taking approach.

Equities: The Fed’s message

We had already expressed our worries in a number of past equities reports about the divergence of the market’s expectations for extensive rate cuts in 2024 by the Fed and what Fed policymakers were saying. It should be noted that the market expects the bank to deliver six 25-basis-point rate cuts in the current year, starting in March. It should be noted that the US employment market remained relatively tight for December, while inflationary pressures in the US economy remained resilient for the same month.

Both releases could be adding pressure on the Fed to keep rates at high levels for longer. It should also be noted that Fed policymakers have made statements since last month, actually warning markets that the pace of rate cuts may be slower than anticipated and that the bank may begin cutting rates at a later stage than expected.

It was characteristic that Fed Board Governor Waller recognized that rate cuts are likely this year yet warned the markets that the bank may take its time bringing interest rates down. It’s understandable that Fed policymakers may want to push back against extensive dovish market expectations for the Fed. Should Fed policymakers continue to repeat their warnings in the next few days, we may see US equity markets dropping as the market may be forced to reposition itself.

Elon Musk causes turmoil once again

A firestorm was instigated among market participants and Tesla investors in particular about Elon Musk’s controversial comments yesterday. Elon Musk stated on X that “I am uncomfortable growing Tesla to be a leader in AI and robotics without having ~25% voting control enough to be influential, but not so much that I can’t be overturned,” and “Unless that is the case, I would prefer to build products outside of Tesla.”

Mind you that Musk currently controls 13% of the share capital after selling shares to fund the purchase of Twitter and paying tax obligations. The statement tends to set the technological edge enjoyed by Tesla into doubt and, in our opinion, has a “blackmailing” element included for existing Tesla shareholders. The statement could fundamentally weigh on Tesla’s share price, yet it may also serve as a prelude to Elon Musk’s intentions to rebuy shares of Tesla, which could turn the share’s price higher.

Equities Technical Analysis

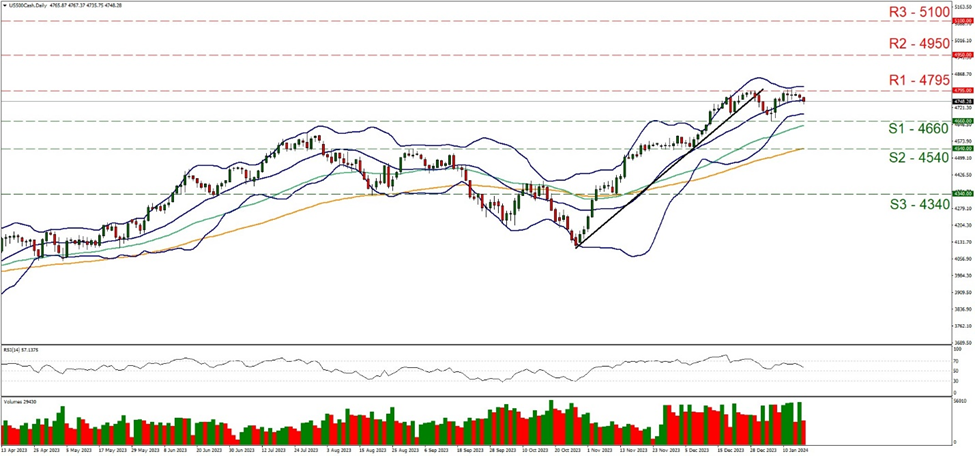

US 500 Daily Chart

Support: 4660 (S1), 4540 (S2), 4340 (S3)

Resistance: 4795 (R1), 4950 (R2), 5100 (R3)

The S&P 500 seems to have hit a ceiling at the 4795 (R1) resistance line over the past few days, forcing the index to stabilise by breaking the upward trendline guiding it from the 27 of October until the 2 of January. Please note that the 20, 50, and 100 moving averages continue to point upward, implying a bullish movement. Nevertheless, for the time being, we tend to maintain a bias for a sideways motion of the index between the 4795 (R1) resistance line and the 4660 (S1) support line that prevented the index from falling on the 5 of January.

It should be noted that the RSI indicator is descending, nearing the reading of 50, implying that the bullish sentiment of the market seems to be fading away. It’s also characteristic how the Bollinger bands narrowed, implying less volatility that could allow the sideways motion to be maintained until the equities market makes up its mind for the direction of the index’s next leg.

Should the bears be in charge of the index’s direction, we may see the S&P 500 break the 4660 (S1) support line and take aim at the 4540 (S2) support level that held its ground from the 21 of November until the 7th of December last year. For a bullish outlook, we would require the index’s price action to clearly break the 4795 (R1) resistance barrier, with the next possible target for the bulls being set at the 4950 (R2) resistance level. Yet we have to note that the R1 is near all-time high levels, which may cause some hesitancy on the part of the bulls to proceed.

If you have any general queries or comments relating to this article, please send an email directly to our Research team at

سلب مسئولیت:

This information is not considered investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced or hyperlinked in this communication.