The current week created considerable turbulence for the markets, with the market mood shifting thus altering the direction of trading instruments. As for the coming week we expect it to also be very interesting and definitely more loaded than the one we leave behind us. On the monetary front, we expect the interest rate decisions of BoC on Wednesday as well as BoJ and ECB on Thursday. Please note that no Fed policymakers are expected to speak in the coming ahead of the bank’s November meeting, so it may be quieter from the US side. As for high impact financial releases they become more frequent near the end of the week. Yet we still would like to note Germany’s Ifo indicators for October on Monday and on Tuesday the US consumer confidence for October. On Wednesday, we get Australia’s CPI rates for Q3, and the US durable goods orders for September. On Thursday we get Germany’s preliminary HICP rate for October while the highlight is expected to be the US GDP Advance growth rate for Q3. On Friday we note France’s, Germany’s and the Eurozone’s preliminary GDP rates for Q3 as well as Eurozone’s preliminary HICP rate for October.

USD – GDP rates eyed

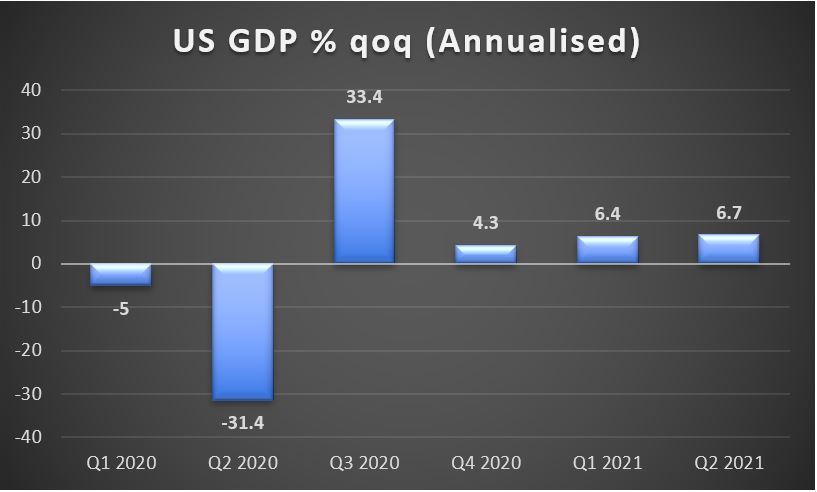

The USD seems about to end in the reds for a second consecutive week against a number of its counterparts. On the monetary front expectations for a tightening of the Fed’s monetary policy are still present. It’s characteristic how Fed Board Governor Waller stated that “a more aggressive policy response” may be required should inflationary pressures be maintained in the US economy. Some analysts tended to interpret the statements as a possibility of earlier rate hikes by the bank. On the flip side it should be noted that market attention tended to be drawn towards the US stockmarkets as the earnings season is on. Also we would like to see how the US yields would behave as they too could influence the market’s opinion. A possible rise of US yields could provide support for the greenback and vice versa. As for financial releases , after a quiet Monday we note on Tuesday the release of the Consumer confidence for October as well as the new home sales figure for September. On Wednesday we get the US Durable goods orders growth rates for September, while on Thursday we note the release of the weekly initial jobless claims figure and we highlight the release of US GDP rate advance for Q3 on an annualised, which could create considerable volatility for the markets. Finally on Friday we get the Consumption rate for September as well as the final University of Michigan consumer Sentiment for October.

GBP – Fundamentals to take the lead

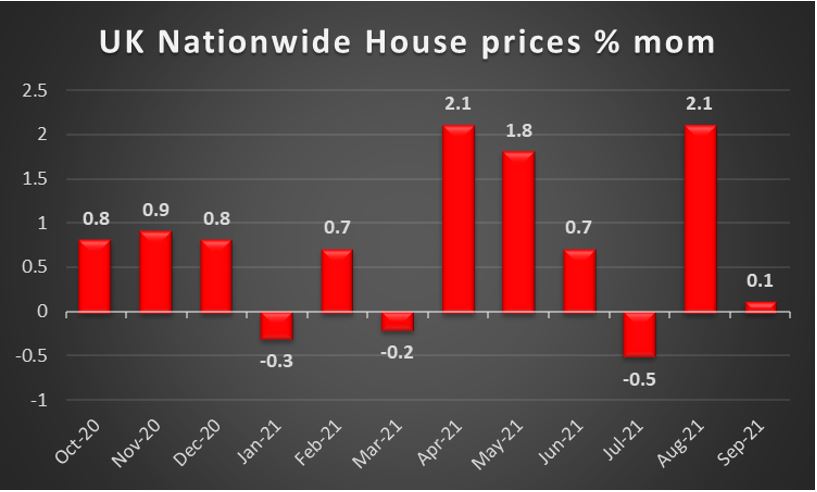

The pound seems about to end the week slightly higher against the USD for a third consecutive week while it weakened against the EUR and CHF. On the monetary front the pound could be supported by the market’s expectations for an earlier tightening of BoE’s monetary policy, despite the tick-down of the headline CPI rate for September. It’s characteristic that BoE Governor Bailey last Sunday stated that “Monetary policy cannot solve supply-side problems – but it will have to act and must do so if we see a risk, particularly to medium-term inflation and to medium-term inflation expectations,”. On a fundamental level we note the continuation of supply shortages and the energy crunch the UK is experiencing, while at the same time we also note the rise of coronavirus cases in the UK. It should be noted that despite some ideas among scientists for renewed measures, the UK government has ruled out the possibility of new lock down measures at least for now. Also any tensions in the relationships of the UK with the EU over Brexit’s Northern Ireland protocol could weigh on the pound. On the fiscal front we note the planned speech of the Chancellor of the Ex Chequers on Tuesday, where Mr. Sunak is expected to provide a semi-annual update on public finances and economic outlook. Overall we expect fundamentals to take the lead in guiding the pound as only a few high impact financial releases are expected next week. Nevertheless, we would like to note on Tuesday the release of the CBI distributive trades also for October, an indicator which could provide more clues about UK’s retail sector and on Thursday the nationwide house price index also for October.

JPY – BoJ’s dovishness to remain

JPY’s six week loosing streak against the USD seems to be halted currently yet the situation remains fluid. In JPY’s fundamentals we cannot miss out on the Japanese political scene which is still fluid and elections are scheduled for the 31st of October. On the other hand the tensions in the relationships of Japan with China and Russia seem to be escalating as Chinese and Russian military ships sailed through

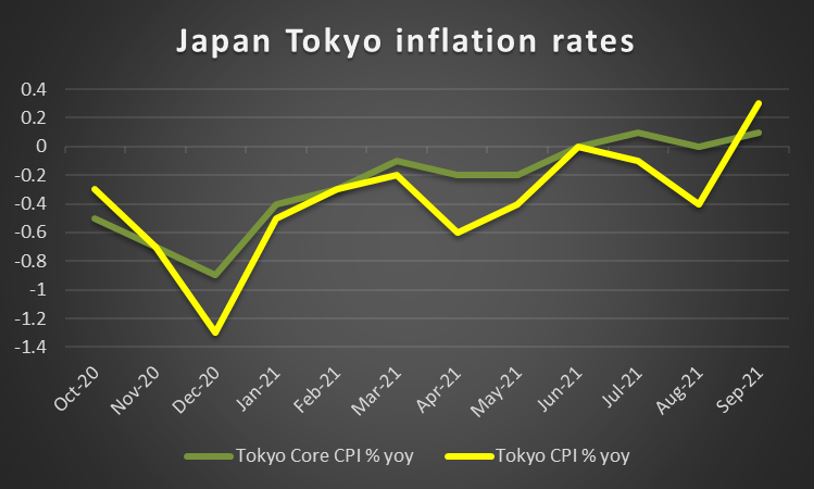

the Japan straits. On a more economic level we tend to maintain our worries for the Japanese economy given the shortage of semicoductor chips which the country’s key industrial sector badly needs. The necessity for the creation of the role of an economic security minister by Prime Minister Kishida, could exactly highlight the sensitivity of the Japanese economy to a wide degreee of threats. On the monetary front we highlight the release of BoJ’s interest rate decision on Thursday’s Asian session. The bank is widely expected to remain on hold at -0.10% and currently JPY OIS imply a probability of 96.32% for such a scenario to materialise. Besides the interest rate decision as such we also expect the bank to maintain a dovish tone given the uncertainty surrounding the Japanese economy at the moment. It’s characteristic that BoJ Officials over the past two weeks made no effort to conceal their dovish inclinations. As for financial releases we note on Friday the release of Tokyo’s CPI rates for October, Japan’s employment data for September and the preliminary industrial output growth rate for September as well.

EUR – ECB meeting in the epicenter

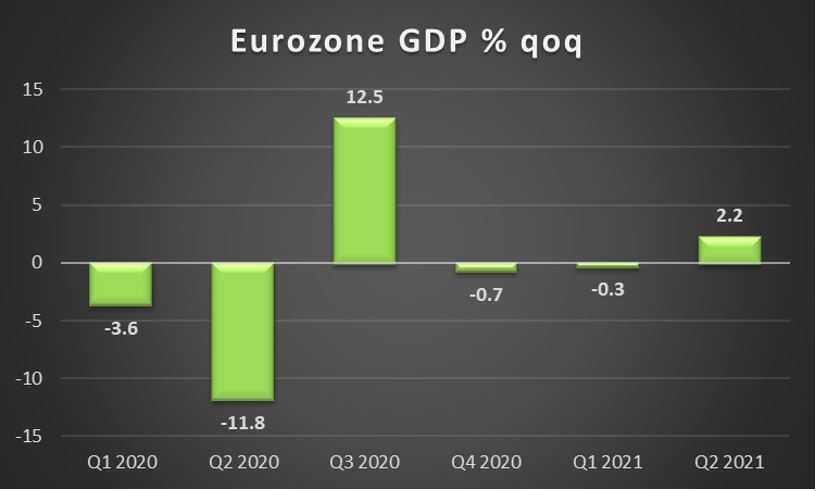

EUR seems to continue to gain against the USD for a second week in a row. It should be noted that the common currency is losing ground against the GBP and CHF which could imply that EUR/USD’s rise is more a matter of USD weakeness rather that EUR strength. On the monetary front ECB’s interest rate decision is expected to provide new clues regarding the bank’s intentions. Currently the bank is widely expected to remain on hold keeping the deposit rate at -0.50% and the refinancing rate at 0.00%. BuBa President Weidman’s resignation currently signals that the ECB hawks are at minus one, yet the gravity of his opinions may still be substantial at the meeting. Overall, though we tend to expect the bank to maintain a more balanced yet still rather dovish tone and if so could weaken the EUR. Also we would highlight the press conference of ECB President Lagarde which is to follow the release and could also create considerable volatility for EUR pairs. On EUR’s fundamentals we highlight gas supplies as a main fundamental issue. In recent headlines it seems that Russia did not actually show interest in increasing its gas supplies to Europe, despite some hints in Russian President Putin’s recent comments to the contrary. Should the energy crunch be extended, we may see the economic recovery of the area slowing as could also intensify inflationary pressures in the area. Hence we would highlight the release of October’s preliminary HICP rates for Germany on Thursday and for France and the Eurozone on Friday. Prior to that we would note the release of Germany’s Ifo indicators for October on Monday while on Friday we highlight the release of the preliminary GDP rates for Q3 of Germany, France and the Eurozone which could also create volatility for EUR pairs.

AUD – Focus on the inflation rates

AUD continues to strengthen against the USD for a fourth consecutive week, despite some weakening on Thursday. High commodity prices in combination with a positive market sentiment tended to support the AUD in the past days. Also rising Australian yields could have created some support for the Aussie. Some analysts tend to note that there may also be market expectations for RBA to start finally tightening its monetary policy, speculating for earlier rate hikes than the bank’s statement for the earliest rate hikes being placed in 2024 however we would still advise caution for this scenario. It’s characteristic that RBA Governor Lowe stated yesterday that inflationary pressures are transitory and effectively pushed back against earlier rate hikes. On a fundamental level we note the easing of the covid related restrictions and Melbourne is about to exit lockdown. On the worrying side, Victoria’s cases are reported to have jumped. On second note we maintain our worries regarding the possibility of an escalation in the tensions of the US-Sino relationships and the Sino- Australian relationships, which could have adverse effects on AUD. As for financial releases we highlight the release of Australia’s CPI rates for Q3 on Wednesday. Should the rate accelerate further, we may see the pressure on RBA to start tightening its monetary policy increasing, despite the recent soft employment data for September, thus creating some support for AUD. We would also note the release of the final retail sales growth rate for September on Friday.

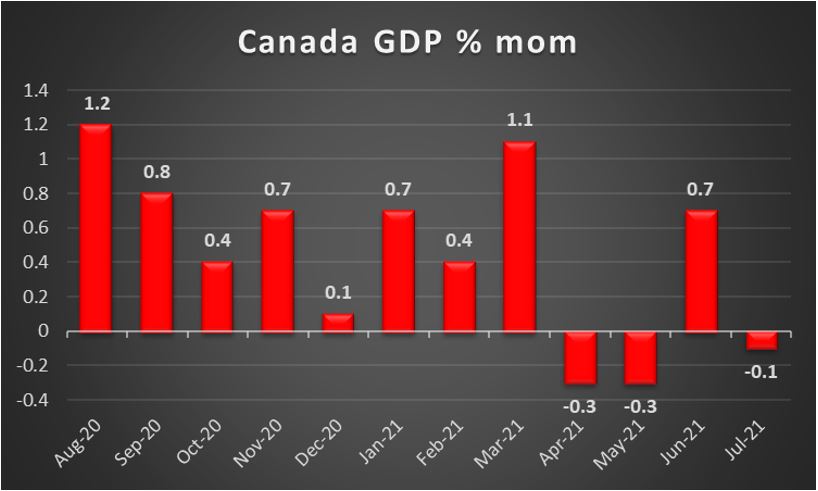

CAD – BoC confidence could be maintained

Also the Loonie is about to end the week stronger against the greenback. Fundamentally the Loonie gets support from higher oil prices as well as the positive market sentiment which dominated the markets yesterday. Oil prices continued to rise, stoked by expectations for stronger demand and a surprise drawdown reported Wednesday by EIA regarding last week’s US oil inventory levels. Fundamentally we expect the possibility of higher oil prices to continue to support the CAD. On the other hand, the higher than expected CPI rates for September released on Wednesday confirmed the inflationary pressures in the Canadian economy increasing the pressure on the BoC to tighten its monetary policy. BoC is to release its interest rate decision on Wednesday’s American session and is widely expected to maintain its rate unchanged at 0.25%. Overall we may see the bank maintaining its confidence, especially given the inflationary pressures in the Canadian economy, which could translate into a hawkish tone. After the release please note the scheduled press conference of BoC Governor Tiff Macklem to discuss the bank’s monetary policy. As for financial releases we note the release of Canada’s GDP rate for August on Friday as well as the Producer Prices for September at the same time.

General Comment

As a closing comment we would like to note that volatility in the markets is expected to be maintained as there are ample of high impact financial releases. We expect the USD to also maintain the initiative over other currencies. Yet given that there also high impact releases and events stemming outside the US, we may see other currencies grabbing the markets’ attention from time to time. As for US stockmarkets, better than expected figures tended to attract attention creating a positive market mood, in a more risk on fashion that may have cost the USD some safe haven outflows. We see the case for the earnings season to continue to interest investors in the coming week, given that high profile companies such as Facebook and Apple are due to release their earnings reports for Q3. Also for US stockmarkets we tend to keep our worries for the possible ripple effects which the situation with the Chinese property market may have. On the other hand, Gold’s prices tended to rise for the past few days benefiting from the weakening USD. Yet gold’s upward movement seems to be somewhat capped, prevented possibly by higher US yields which pose an attractive alternative, which should also be watched out for in the coming week.

اگر در مورد این مقاله سوال یا نظر ی کلی دارید، لطفاً ایمیل خود را مستقیماً به تیم تحقیقاتی ما بفرستیدresearch_team@ironfx.com

سلب مسئولیت:

این اطلاعات به عنوان مشاوره سرمایه گذاری یا توصیه سرمایه گذاری در نظر گرفته نمی شود ، بلکه در عوض یک ارتباط بازاریابی است. IronFX هیچ گونه مسئولیتی در قبال داده ها یا اطلاعاتی که توسط اشخاص ثالث در این ارتباطات ارجاع و یا پیوند داده شده اند ندارد.