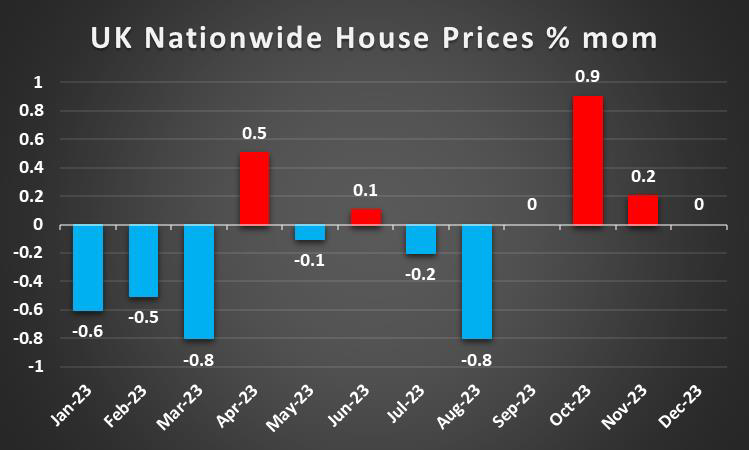

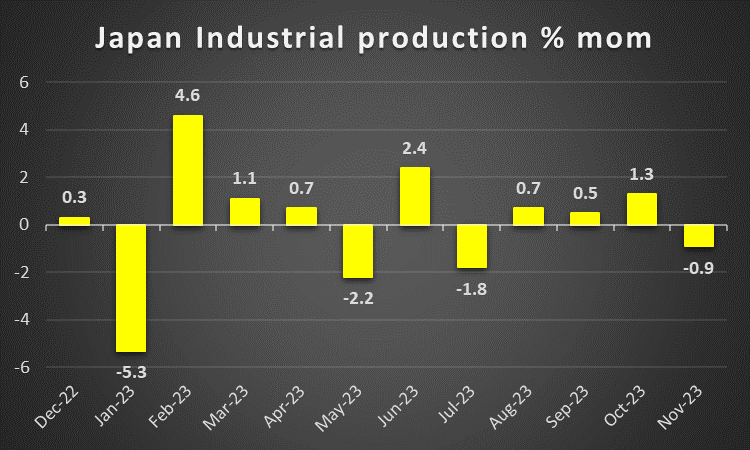

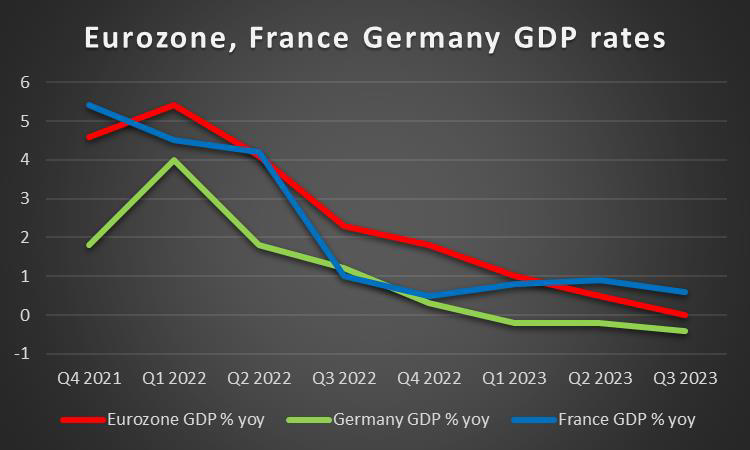

As the week draws to a close we open a window at what next week has in store for the markets. On a monetary level, the scenery is dominated by the interest rate decisions of the Fed on Wednesday and UK BoE’s on Thursday, yet on Thursday we also note from Sweden Riksbank’s interest rate decision. As for financial releases we make a start on Monday with Sweden’s preliminary GDP rate for Q4, while on Tuesday we get Q4’s preliminary GDP rates of France, the Czech Republic, Germany and the Eurozone, while we also note the release of Australia’s retail sales for December, Switzerland’s KOF indicator, Eurozone’s economic sentiment for January and from the US the December JOLTS Job Openings. On Wednesday we begin with the release of Japan’s preliminary industrial output for December, Australia’s CPI rates for Q4, Chinas’ NBS manufacturing PMI figure for January, UK’s nationwide house prices for the same month, France’s and Germany’s preliminary HICP rates for January, the US ADP national employment figure for January and Canada’s GDP rates for November. On Thursday we note the release of Australia’s building approvals for December, China’s Caixin manufacturing PMI figure for January, Eurozone’s preliminary HICP rates for January, the US weekly initial jobless claims figure, Canada’s manufacturing PMI figure for January and the US ISM Manufacturing PMI figure for January. On Friday we highlight the release from the US of the employment report for January and also note the release of the factory’s orders for December and the final University of Michigan consumer sentiment for January.

USD – Fed’s decision and US January employment data

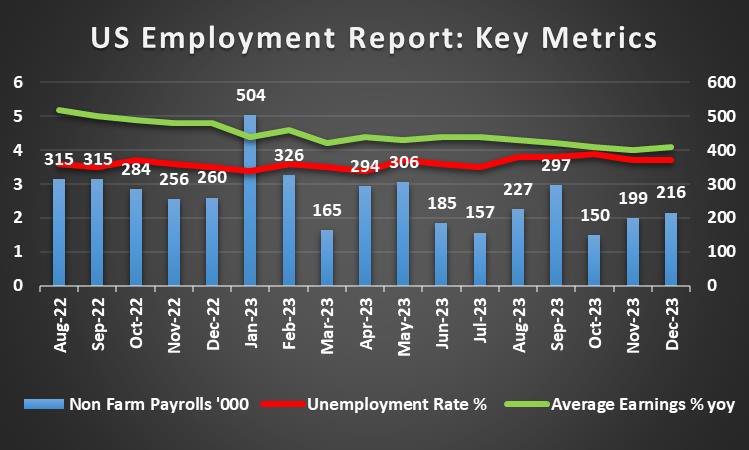

The USD is about to end the week in the greens against its counterparts and may have gotten also some support from the less-than-expected deceleration of the US GDP advance rate for Q4, which tends to underscore the narrative for a possible soft landing of the US economy. For the coming week, we highlight two issues with the first being the Fed’s interest rate decision on Wednesday. The bank is widely expected to remain on hold in the range of 5.25-5.5% and currently, Fed Fund Futures imply a probability of 97.5% for such a scenario to materialise. Yet the market tends to expect the bank to start cutting rates from May onwards and deliver a total of 6 rate cuts in the current year. Hence we expect market attention to be placed on the accompanying statement and Fed Chairman Powell’s press conference later on. Should the bank contradict market expectations and imply that rate cuts are to be delayed beyond the May meeting, we may see the USD getting some support. On the flip side, the bank may opt to keep its options open which may be perceived as a confirmation of the market’s suspicions and in such a scenario, we may see the USD losing ground. The second event we highlight would be the release of the US employment report for January on Friday. The data are expected to show an easing of the US employment market’s tightness in December. Characteristically the Non Farm Payrolls figure is expected to drop to 162k if compared to December’s extraordinary 216k, yet the unemployment rate to remain unchanged at 3.7%. Such data could weaken the USD as they would imply a crack in the tightness of the US employment market. Yet forecasts of the US employment data have been disproven a number of times in the past, thus an element of uncertainty is present for the release which may raise volatility for the markets. Should the data show that the employment market has not lost from the tightness reported in December we may see the USD gaining asymmetrically, as it would add more pressure on the Fed to keep rates at high levels for a prolonged period, given the bank’s dual mandate. Please note that both releases are expected to have ripple effects beyond the FX market, possibly affecting also US stock markets and gold’s price as well.

GBP – BoE’s interest rate decision under the spotlight

The pound is about to end the week stronger against the EUR yet near the same levels against the JPY and USD. On a macroeconomic level, we note the better-than-expected preliminary Services PMI figure for January, showing that economic activity in the UK services sector expanded at a faster pace than anticipated, thus improving the outlook for the UK economy and supporting the pound. An additional sign of improvement was that the contraction of economic activity in the manufacturing sector seems to have been narrower than expected. Yet the CBI indicators showed wide pessimism for industrial orders. On a monetary level, we highlight the release of BoE’s interest rate decision that may prove to be the main event for pound traders next week. The bank is widely expected to remain on hold, with GBP OIS implying a probability of 98.28% for such a scenario to materialise. It should be noted that the UK CPI rate slowed down considerably over the past year, yet jumped slightly in December at which period prices rose at the rate of 4% yoy. The release tended to showcase that there is still work to be done before inflation returns to the bank’s 2% target. It’s characteristic that GBP OIS imply that the market expects the bank to start cutting rates in the June meeting and deliver in total, 4 rate cuts within the year. Hence we would expect the bank to maintain a confident tone in the accompanying statement, implying that rate cuts may happen within the year, yet that it would be premature to start discussing them. Such a scenario may provide some support for the pound, especially if it’s implied that the rate cuts are due after the summer. On the other hand, should the bank seem uncertain we may see the pound slipping. Also, we note the vote count in taking the decision, as should more MPC members vote in favour of rate hikes, we may see the pound getting some support.

JPY – BoJ remained on hold

JPY is about to end the week with some slight gains against the USD and the EU and remains relatively unchanged against the GBP. On a monetary level, we note that BoJ remained on hold, as was widely expected in its interest rate decision on Tuesday. Moreover, in the bank’s accompanying statement, the BOJ said that it “will continue with Quantitative and Qualitative Monetary Easing (QQE) with Yield Curve Control, aiming to achieve the price stability target, as long as it is necessary for maintaining that target in a stable manner”. Yet during the BOJ Press conference, Governor Ueda’s re-affirming that the BOJ will end its negative interest rate policy once 2% inflation is achieved, may have provided some support for JPY, as the bank seems to maintain a tendency towards normalising its ultra-loose monetary policy. Yet the release failed to excite JPY traders and may be an indication that the market requires more solid evidence for the bank’s intentions. On a macroeconomic level, the slowdown of inflationary pressures on a headline and core level for December, as mentioned in last week’s report tends to decrease the creditworthiness of BoJ’s narrative and could intensify carry trade which in turn could weaken JPY. Furthermore, we also note the slow-down of Tokyo’s CPI rates for January, which tends to act as a barometer for inflation nationwide given the density of the Japanese megacity’s population. Also, economic activity seems to be improving despite the contraction in the key manufacturing sector, which may be a positive sign for Japan’s economic outlook as well as the turning of the trade deficit into a surplus in December. On a more fundamental level, we note the dual nature of JPY as a safe haven and national currency, hence should a more risk-oriented approach be adopted by the market next week we may see JPY experiencing some outflows.

EUR – ECB signals a delay in rate cuts

The EUR is about to end the week lower against the USD, the GBP and JPY, in a sign of a wider weakness. It should be noted that the EUR is falling even despite ECB’s interest rate decision. The bank as was widely expected remained on hold, keeping the refinancing rate at 4.5% and the deposit rate at 4.00%. In the bank’s accompanying statement there were no major surprises, yet the bank mentioned that “Tight financing conditions are dampening demand, and this is helping to push down inflation” which may imply that the bank is set to continue keeping monetary policy conditions tight. It’s characteristic that in her press conference, ECB President Christine Lagarde stated that there was a consensus at the table that it’s premature to talk about rate cuts. Overall we tend to see the case for the bank to push any rate cuts for a later stage than what was expected by the market, possibly around summer 2024. For the time being the market, seems to remain unconvinced and expects the bank to deliver 6 rate cuts within the year and the meeting may have contributed to the bearish tendencies of the EUR. On a macroeconomic level, we note that the confidence of the average eurozone consumer for January is turning more pessimistic, while in the same month the outlook of Eurozone’s economic powerhouse, Germany seems to be deteriorating for the next months. On a more positive note, economic activity, in Germany’s manufacturing sector, despite shrinking we note that it seems to have contracted to a lesser degree in January according to the preliminary PMI figures for the current month. Overall the situation seems to be improving for the manufacturing sector of the Eurozone as a whole, yet the fact that economic activity is still contracting seems to be clipping the optimism for the outlook of the Eurozone. We expect the area to have a difficult first half of 2024, something that may be reflected in the preliminary GDP rate for Q4 next week.

AUD – Market sentiment to move the Aussie

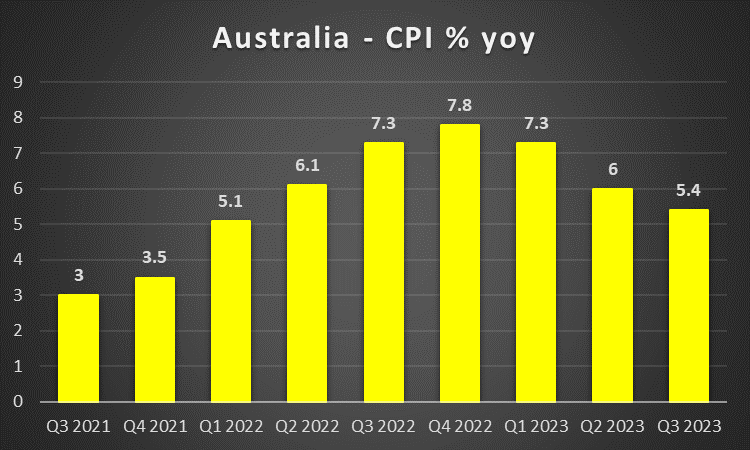

AUD is about to end the week relatively unchanged against the USD, after three consecutive weeks of losses. On a fundamental level, we note the intentions of the Australian government to deliver a tax cut, which may increase the money flow within the Australian economy and serve as a boost on a fiscal level. Furthermore, we note that the Aussie tends to remain sensitive to the market sentiment given its nature as a commodity currency. Hence we expect that should a more positive approach emerge by market participants in the coming week we may see the Aussie getting some support. Yet, Aussie traders are also expected to keep a close eye on developments in China, given the close Sino-Australian economic ties. We note that Chinese factories seem to be struggling to increase economic activities, hence we highlight the release of China’s manufacturing PMI figures for January on Wednesday and Thursday. Should economic activity in China’s manufacturing sector contract, we may see it weighing on AUD as it would imply a possible easing of Australian exports of raw materials to the Chinese mainland. On a macroeconomic level, we highlight the release of Australia’s December and Q4 CPI rates on Wednesday’s Asian session. The release gains on importance given the release of RBA’s interest rate decision six days later. Should the rates continue to decelerate, we may see the Aussie losing ground as RBA would be justified to ease on its hawkishness, while a possible failure of the rate to slowdown may instigate worries for the bank to maintain rates high for a longer period. For the time being the market expects only one rate cut in 2024 and that may be delivered in the August meeting. Should we see RBA Governor Bullock’s comments over the past few months, it does not seem to be the case that the bank is in any kind of hurry to cut rates. Hence we may see the Aussie being supported on a monetary level.

CAD – BoC stands pat, as expected

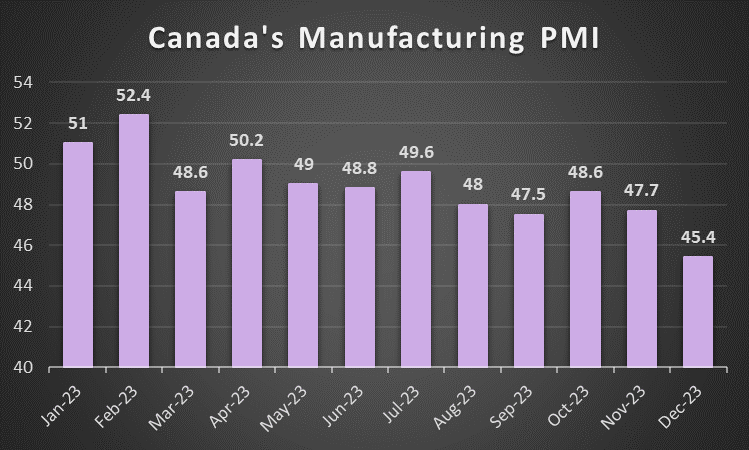

The Loonie is losing ground against the USD for the fifth week in a row. On a macroeconomic level, we note that last week, the producer prices contracted deeper into the negatives for December in a prelude for a possible further easing of inflationary pressures in the Canadian economy. The idea was further enhanced by a contraction of the retail sales growth rates for November, both on a month-on-month as well as on a year-on-year level. On the other hand, the business barometer for January seems to have improved, implying a greater degree of optimism for Canada’s economic outlook. In the coming week, we note the release of Canada’s GDP rate for November and a possible contraction could weaken the Loonie, as it would imply that the Canadian economy shrunk ahead of the Christmas period. On a monetary level, we note that BoC remained on hold, as was widely expected, keeping rates at 5%, yet quantitative tightening continues, straining Canada’s financial environment indirectly further. In its accompanying statement, the Bank highlights that “ The Council is still concerned about risks to the outlook for inflation, particularly the persistence in underlying inflation”. The statement could be perceived as implying that the bank may delay any rate cuts given the persistence of underlying inflation. The market expects the bank to deliver 4 rate cuts in 2024 and the bank may have contradicted them, yet seems to have failed to change the market’s mind. On a fundamental level, we keep an eye out for oil prices given the traditional positive correlation of the CAD with oil prices. The rise of oil prices seems to have failed to provide some support for the Loonie in the current week. For the time being it seems that the weather conditions in the US, the tight US oil market, China’s stimulus package and rising tensions with Houthi rebels, could provide some support for oil prices. Should oil prices rise in the coming week we may provide some support for the CAD as well on a fundamental level.

اگر در مورد این مقاله سوال یا نظر ی کلی دارید، لطفاً ایمیل خود را مستقیماً به تیم تحقیقاتی ما بفرستیدresearch_team@ironfx.com

سلب مسئولیت:

این اطلاعات به عنوان مشاوره سرمایه گذاری یا توصیه سرمایه گذاری در نظر گرفته نمی شود ، بلکه در عوض یک ارتباط بازاریابی است. IronFX هیچ گونه مسئولیتی در قبال داده ها یا اطلاعاتی که توسط اشخاص ثالث در این ارتباطات ارجاع و یا پیوند داده شده اند ندارد.