With the week nearing its end, we note the BRICS summit that was hosted in South Africa, seems to have resulted in positive news for the bloc, with new invitations being extended to Saudi Arabia, the UAE and Iran amongst others, potentially increasing their sphere of influence on the Global stage. In regards to financial releases, we make a start on Tuesday with the Czech Republic’s Final GDP rates for Q2 followed by the US JOLTS Job openings figure for July. On Wednesday we make a start with Australia’s building approvals figure for July, followed by the Eurozone’s economic sentiment figure, Germany’s Preliminary CPI print and the US ADP Employment figure, all for the month of August. Followed by the US 2nd GDP rate estimated for Q2 and the Core PCE rates for Q2. On a busy Thursday, we note China’s NBS Manufacturing PMI figure, France’s Final GDP rate for Q2, Preliminary CPI rates for August, Producer prices rate for July, followed by Turkey’s GDP rate for Q2 the Eurozone’s Preliminary HICP rate for August and Unemployment rate for July and closing of the day with the US Core PCE rates for July and weekly initial jobless claims figure. Finally on Friday, we begin with Australia’s Judo Bank final Manufacturing PMI figure for August and Japan’s JiBunk final Manufacturing PMI figure for August, China’s Caixin Final Manufacturing PMI figure for August, France’s and Germany’s Manufacturing PMI figures for August, the Eurozone’s Final Manufacturing PMI figure for August, the US Employment data for August, Canada’s GDP rate for Q2, Manufacturing PMI figure for August and the US S&P and ISM Manufacturing PMI figures for August.

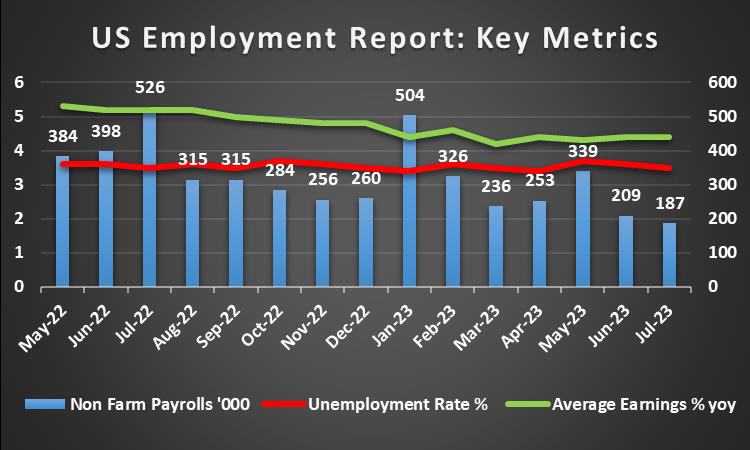

USD – US Economy starting to feel the brunt of high interest rates?

The USD continued its upward trajectory against its counterparts for the 6th week in a row. On a fundamental level, we highlight that following a Fitch credit rating analyst allegedly claiming that they may be forced to downgrade a number of US bank, S&P has also joined on the downgrading bandwagon, having downgraded multiple US banks on Tuesday after citing “tough” lending conditions. The “tough” lending conditions, appear to be in line with fears that the banks may be overexposed to commercial real estate, seems to be at the top of the credit rating agency’s concerns. On a monetary level, we highlight the expected speech by Fed Chair Powell at Jackson Hole Today, where he is widely anticipated to answer questions on the Fed’s current interest rate policy, with investors potentially hoping to hear re-assurances by the Fed Chair that the Fed is on track to cut rates by mid-2024. The Fed Chair’s speech is due to garner attention following last week’s statements by Minneapolis Fed President Kashkari who hinted that more rate hikes may be required. On a macroeconomic level, we highlight the US PMI preliminary PMI figures that were released on Wednesday which where indicative of a continued contraction in the US manufacturing industry and a slowdown in the US services industry. In addition to the lower-than-expected existing home sales figure for July, seems to be spiking fears about the resilience of the US economy. Looking into what next week has in store for us, we would be highlighting the US JOLTS Job openings figure on Tuesday, the US ADP Employment data, US Preliminary GDP rate for Q2 and the Preliminary Core PCE Prices rate for Q2 on Wednesday and on a busy Friday the US Employment data for August followed by the S&P Final and ISM Manufacturing PMI figures for August.

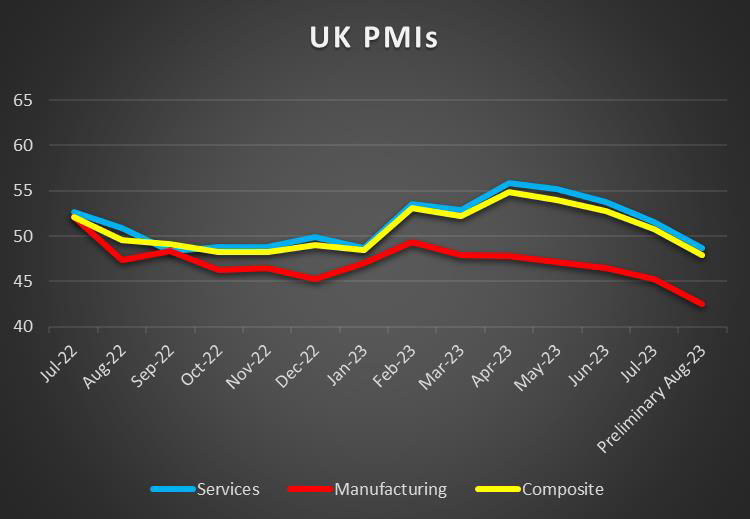

GBP – The UK economy seems to be bleeding

The pound seems about to end the week lower against the USD the JPY and the EUR. On a fundamental level, we note the confirmation that British Chip maker Arm Ltd will be snubbing London, in favour of a listing on the US based NASDAQ. On a monetary level, we note no major new’s stemming from the Bank of England. On a macroeconomic level however, the UK’s CPI UK’s Preliminary PMI figures on Wednesday, where indicative ofa continued deterioration in economic activity in the UK. The lower than expected figures could, be concerning as recent financial release could hint that inflationary pressures may still persist in the economy, whilst economic activity deteriorates. The afformentioned combination of high inflation and a reduction in economic activity could potentially lead to a grave economic situation in the UK, potentially causing the UK to enter a recession if the current economic environment continues.

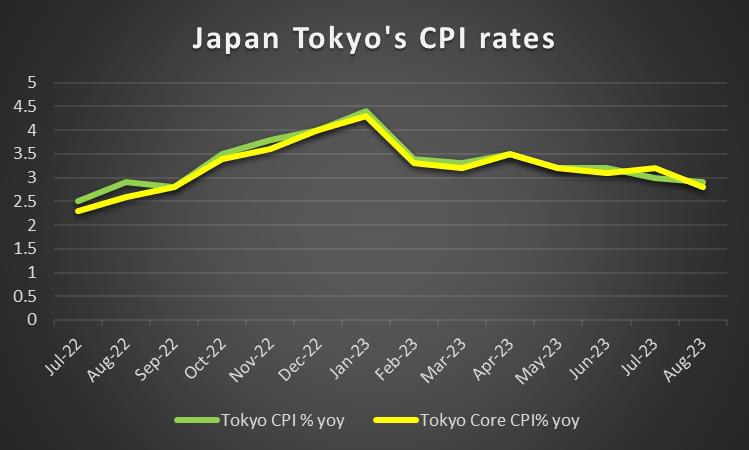

JPY – Japan’s CPI data sends mixed signals

JPY is about to end the week lower against the USD but stronger against the EUR and the pound. On a fundamental level, we note that Japan has begun released treated nuclear water from its Fukushima nuclear plant, which appears to have drawn some ire from Chinese officials, potentially further escalating tensions

in the region. On a monetary level, we note the relatively quiet front from BOJ officials, which no major statements made during the week. On a macroeconomic level, we note Japan’s JiBun Manufacturing PMI figure which can in better than expected, hinting at a resilient manufacturing industry in Japan. In addition, Japan’s Tokyo Core CPI rate came in lower than expected today, potentially hinting at easing inflationary pressures, which could aid the BOJ’s current monetary policy which appears to be working in their favour. Yet, the BOJ’s Core CPI rate which was released on Tuesday, came in higher than expected. The higher than expected figure, contradicts the lower than expected Tokyo CPI rate which was released earlier on today, therefore it could lead to increased volatility in the market, as traders may be uncertain as to how to interpret the contradicting financial releases. Lastly looking at what next week has in store for Japan, we note no major financial releases, thus the currency could cede control to its counterparts.

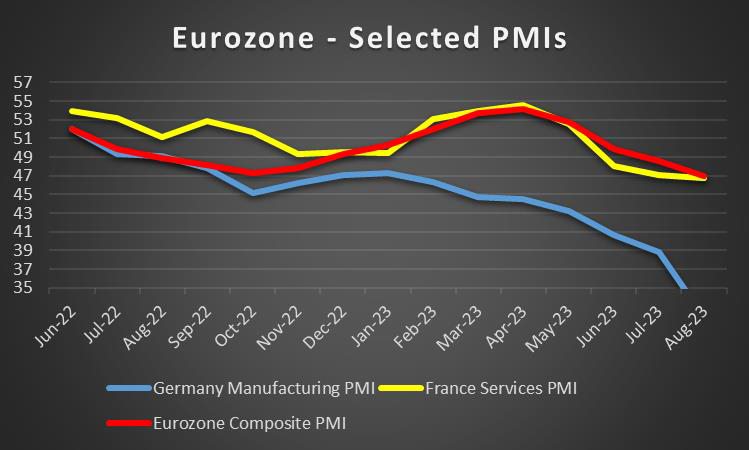

EUR – PMI figures across the Eurozone might be sounding some alarm bells in Europe

EUR is about to end the week in the reds against the JPY and the greenback but higher against the pound. On a fundamental level, we highlight the ongoing efforts by the Greek Government to combat the current wildifres, with the EU mobilizing more planes and firefighters to be sent to the country’s aid. On the monetary front, we note the anticipated speech by ECB President Lagarde today at the Jackson Hole conference, in which she may shed some light on the banks next actions. On a macroeconomic level, the continued deterioration in the services PMI figure for France, Germany and the Eurozone as a whole, which could be concern on a general level , as many economies in the Eurozone are services orientated, it could be a warning sign of a deterioration in the overall services industry. Surprisingly, the manufacturing PMI figures for France, Germany and the Eurozone, as a whole have seeming improved slightly, albeit still in a contraction but an improvement, nonetheless. The better than expected , manufacturing PMI figures could provide some hope for the Eurozone, as Germany which is one of the largest EU economies, is reliant on its manufacturing industry and as such the improvement could potentially provide some support for the common currency. Looking into next week, market participants may be interested in the Eurozone’s economic sentiment figure , Germany’s Preliminary CPI rates for August, which are due to be released on Wednesday. Followed by France’s Final GDP rate for Q2, Preliminary CPI rate for August and Producer prices rate for July followed by, the Eurozone’s Unemployment rate for July and Preliminary HICP rates for August, which are all due to be released on Thursday.

AUD – Will the LNG Companies in Australia manage to avoid a strike?

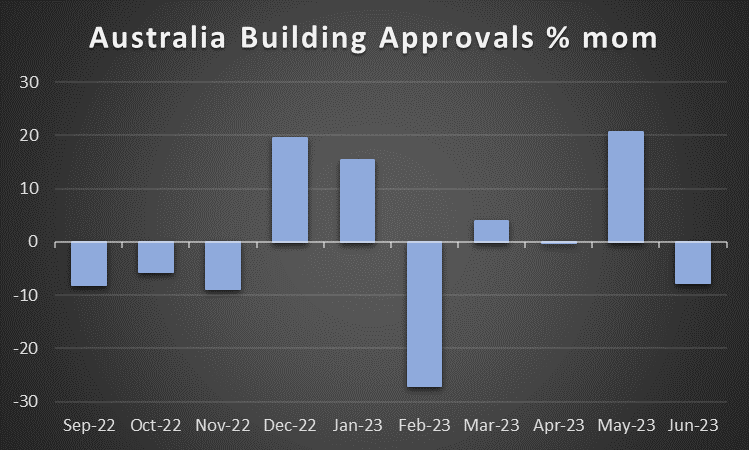

AUD is about to end the week slightly higher than the dollar, potentially stopping a 5 week decline. On a fundamental level, we note that last week’s fears regarding Australian LNG producers appear to have slightly eased following reports that some companies have reached an agreement with their workers, yet some others have yet to do so, therefore tensions may still remain high. As stated last week, the possibility of LNG workers deciding to go on strike, could possibly disrupt 10% of the world’s liquified natural gas supply. On a monetary level, we note the report by Bloomberg which states that Australia Treasurer Jim Charles is considering appointing an outsider for the role of Central Bank Deputy Governor, which will become vacant once Michele Bullock takes over as Governor in September. On a macroeconomic level, we note the Australia’s Judo Bank Manufacturing PMI figure which came in lower than expected, hinting at a continued contraction in Australia’s Manufacturing industry which could spell some trouble for the already troubled Australian economy. Lastly, market participants may be looking at next week’s building Approvals rate for July on Monday and the Judo Bank Manufacturing PMI final figure for August which is due to be released on Friday, for more clues in regards to the resilience of the Australian economy.

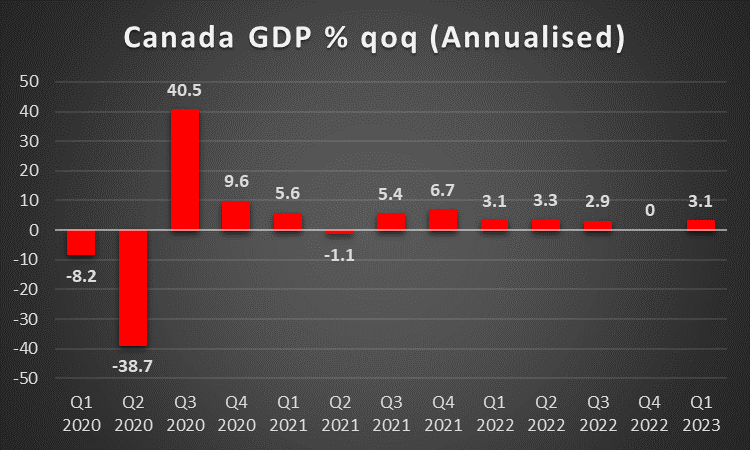

CAD – Loonie extends its losses for a 6th week in a row

The Loonie appears to be ending for a 6th week in a row in the reds against the dollar. On a fundamental level, we note that one of Canada’s biggest banks the RBC, according to news outlets are considering to reduce the number of their employees, citing economic worries. On a monetary level, we note no major press releases by bank officials, despite recent financial releases and as such the pair might have ceded control to the direction of its counterparts. On a macroeconomic level, we note that we note Canada’s Core Retail sales rate coming in lower than expected, potentially indicating a deterioration in consumer activity in Canada , as consumers may be feeling the brunt of high interest rates. Therefore, should the fincnail releases which are due next Friday such as the GDP for Q2 and the Manufacturing PMI Figure for August, support this theory, we may see the Loonie continue in its downwards trajectory. However, given Canada’s status as a major oil exporting country, the currency may find support should the price of oil move higher, as it could potentially increase revenue for the country which in turn could provide support for the Loonie.

General Comment

In the coming week we expect volatility in the FX market to continue to increase given the high volume of financial releases which are due next. We also note that the earnings season in the US appears to be slowing down, as most high-profile companies have already released their earnings reports. Nonetheless, we would note HP INC (#HPQ) and NIO (#NIO) on Tuesday and UBS (#UBS) on Thursday are expected to release their earnings. As for gold’s price, we note that it appears to be ending the week higher, putting a stop to 4 week of being in the reds. On a more fundamental level, we highlight China the current situation in China is deeply troubling, as the Chinese Government appears to be trying to support its property industry, which despite the positive releases that the Government may be implementing measures to help the sector, our underlying concerns still persist.

اگر در مورد این مقاله سوال یا نظر ی کلی دارید، لطفاً ایمیل خود را مستقیماً به تیم تحقیقاتی ما بفرستیدresearch_team@ironfx.com

سلب مسئولیت:

این اطلاعات به عنوان مشاوره سرمایه گذاری یا توصیه سرمایه گذاری در نظر گرفته نمی شود ، بلکه در عوض یک ارتباط بازاریابی است. IronFX هیچ گونه مسئولیتی در قبال داده ها یا اطلاعاتی که توسط اشخاص ثالث در این ارتباطات ارجاع و یا پیوند داده شده اند ندارد.