Crude prices were on the retreat this week, failing to break past last week’s $83 peak and are currently found trading near the $78 level. Contributing to the depreciation in prices has been the prospect for a higher interest rate environment which could staunch global economic growth and thus tarnish the demand for energy. On the flip side, what kept a floor under crude’s prices were the stronger than anticipated GDP results from China, which broadcasted to the world that the Red Dragon’s sharp recovery after the abandonment of its strict zero covid policy, could play a pivotal role in the global scene in 2023. In this report we aim to shed light on the catalysts driving WTI’s price, assess its future outlook and conclude with a technical analysis.

Russian oil flows towards the East

Russian crude has been increasingly flowing towards the East since the start of the year and more specifically towards the largest oil consuming nation in the world, China and the now officially most populous nation in the world, India. According to Reuters, in the month of April, Russia sold the majority of its crude to these nations, with India receiving 70% and China 20% respectively, at above the $60 price cap that has been imposed by Western nations in December. The move essentially bypasses the sanctions and sends a disappointing message back to the Western world, whose plan was to stifle Russia’s oil revenue inflows, that are used to prolong the war in Ukraine. Reuters data also showed that Urals sales in Asia have already matched half of last year’s volume, indicative of record shipments in 2023. Russia’s ability to expertly maneuver away from European “punishment” and divert their flows towards the East, sends a bitter message to the group and without a doubt undermines the credibility of the European Commission’s retaliation tactics. This makes the decision by Europe harder to swallow, since the sanctions left the continent depleted from Russian supply, compounding the negative impact on common European folks, who thankfully had luck on their side, as this winter’s conditions were rather mild. Considering all this, a question arises, what about the next winter?

Norway emerges as a key crude supplier for Europe

As European nations aggressively work towards severing ties from Russia’s oil supply, limiting their dependency, Norway steps in and capitalizes on the opportunity to cover the continent’s crude needs. More specifically, Norway is now pumping crude to European market refineries in countries such as Finland, Germany and Poland, replacing in a sense the sanctioned flow from their common foe, Russia. Johan Sverdrup crude, the oil that gets extracted from Norse fields, has similar qualities to the Urals crude of Russia and could play a key role in the bloc’s efforts to restock crude in the months ahead, as European nations brace for this year’s winter impact. The capacity of Norway to cover the needs for the entirety of the European nations comes under question however and remains to be seen whether the country has the ability to do so.

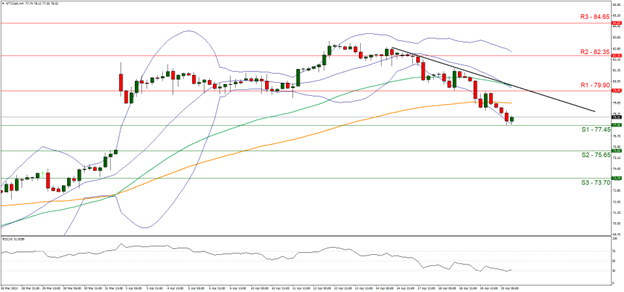

تجزیه و تحلیل فنی

- Support: 77.45 (S1), 75.65 (S2), 73.70 (S3)

- Resistance: 79.90 (R1), 82.35 (R2), 84.65 (R3)

Looking at WTICash 4-hour chart we see crude reversing last week’s gains, having broken below the $80 key psychological level, forming a downwards trendline, and aims for the $77.45 (S1) support line. We hold a bearish outlook bias for the commodity, given its daily downwards path and supporting our case is the RSI indicator below our 4-hour chart which registers a value of 30, showcasing an intense bearish sentiment surrounding WTI. Should the bears extend their dominance, we would like to see a clear break below the $77.45 (S1) support level with a move towards the $75.65 (S2) resistance barrier. Should on the other hand the bulls take over, we may see the break above the descending trendline, the break of the $79.90 (S1) support level and moving towards the $82.35 (S2) support base.

سلب مسئولیت:

This information is not considered investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced or hyperlinked, in this communication.