Leaving behind us a turbulent week, we take a sneak peek into what next week has in store for the markets. On the monetary front we note the releases of the interest rate decisions of the CNB from the Czech Republic on Wednesday as well as of Norgesbank from Norway and CBT from Turkey on Thursday. Also please note that RBA is to release the minutes of its June meeting on Tuesday. Furthermore, various policymakers from central banks around the world are scheduled to make statements and could sway the market’s opinion. As for financial releases, after a quiet Monday, we note on Tuesday UK’s CBI trends for industrial orders for June, Canada’s retail sales for April and on Wednesday we get New Zealand’s trade data, UK’s and Canada’s CPI rates, all releases being for May as well as the Preliminary consumer confidence of the Eurozone for June. On Thursday we note the release of Australia’s, Japan’s, France’s, Germany’s, the Eurozone’s, UK’s and the US preliminary PMI figures for June, UK’s CBI distributive trades for June and the US weekly initial jobless claims figure. On Friday we get from Japan the CPI rates and UK’s retail sales both for May, Germany’s Ifo indicators and the US final University of Michigan consumer sentiment both for June.

USD– Fundamentals in the front seat

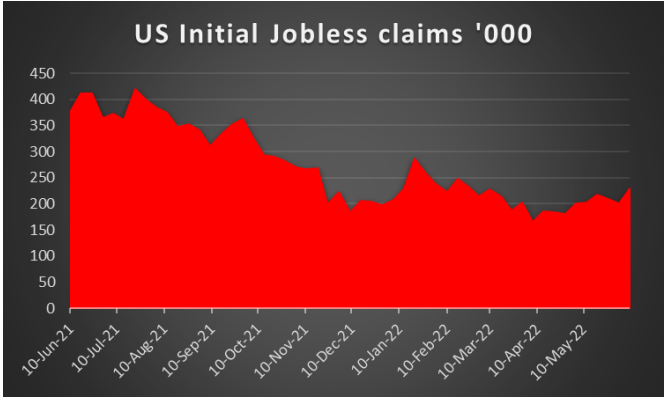

The USD index had a turbulent ride in the past days, mostly due to the Fed’s interest rate decision and remains in red territory so far in the European morning on Friday. It was characteristic that despite the Fed delivering a 75-basis points rate hike and Jerome Powell’s accompanying press conference, the USD moved lower. In its accompanying statement the bank noted that “The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee’s goals”. In his press conference Fed Chairman Jerome Powell was reported stating that “From the perspective of today, either a 50-basis point or a 75-basis point increase seems most likely at our next meeting,”, which did provide some ambiguity for the bank’s intentions. The market may have expected more decisiveness from the bank and may have been partially let down. Yet the monetary policy tightening of the Fed continues at a rather fast pace, thus could provide some support for the USD. Please note though that Fed Chairman Powell is scheduled to make statements during today’s American session and could provide a clearer view in regards to the Fed’s monetary policy outlook. Overall, in the coming week given the low number of high impact US financial releases, we may see the fundamentals taking over in guiding the greenback. Nevertheless, we would like to note on Tuesday the release of the existing home sales for May and on Thursday the release of the weekly initial jobless claims figure along with the release of the preliminary PMI figures for June. On Friday we get the final UoM Consumer Sentiment for June.

GBP – UK CPI rates in focus

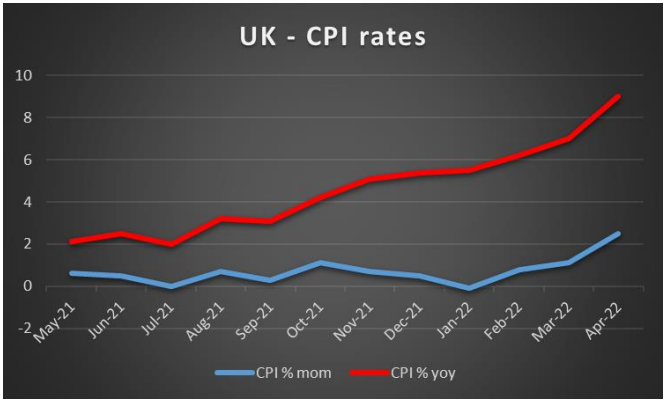

The pound’s weakening against the USD continued for a third week in a row as the currency pair dropped to a new multi-year low in the past days but regained most of the ground in the following sessions. At the moment, the pound is also down against the EUR and the Yen in a sign of a broader weakness. It should be noted that the pound retreated on a weekly basis, despite BoE delivering a rate hike of 25 basis points as expected. In its accompanying statement the bank mentioned that “The MPC will take the actions necessary to return inflation to the 2% target sustainably in the medium term, in line with its remit” which tended to imply that more rate hikes are to come. Yet it should be noted that the bank seems to be sticking to its gradual approach for now, raising its interest rate at the pace of 25 basis points per meeting. It should be noted though that the balance of power within the bank seems to be shifting towards a more hawkish stance, given that three out of nine members of the monetary policy committee (MPC) voted in favour of a 50-basis points rate hike. We see the case for inflationary pressures being the determining factor behind BoE’s future rate hike policy and thus tend to highlight the release of UK’s CPI rates for May on Wednesday. Should the rates accelerate beyond April’s 9.0% yoy we may see the pound getting some support as such rates would be increasing the pressure on BoE to hike rates at a faster pace. We would also note the release of the preliminary PMI figures for June on Thursday and a drop of the related readings could imply further slowdown of economic activity, in an already shrinking UK economy, as indicated by the GDP rates for March and April. We would also like to note the release of the CBI indicators for June on Tuesday and Thursday while on Friday we get UKs’ retail sales for May as well as the GfK Consumer sentiment for June. On a more fundamental level, tensions of the UK with the EU over the Northern Ireland protocol seem to be about to escalate and such a scenario could weaken the pound as the last thing the UK economy currently needs would be another trade war with the EU.

JPY – Japans’ CPI rates eyed

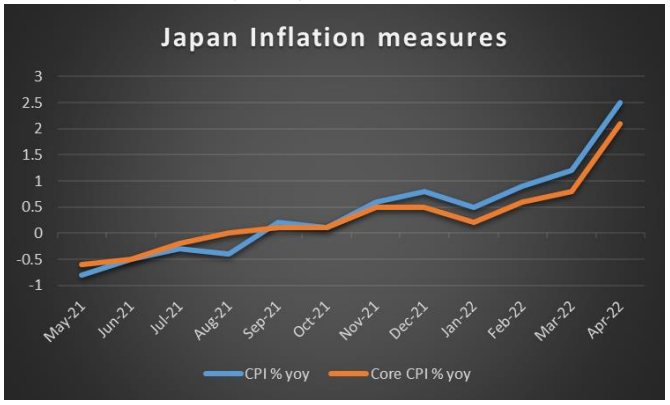

JPY could be ending the week breakeven against the USD, but is still strengthening against the EUR and the GBP. Today BoJ’s interest rate decision confirmed the central bank will remain on hold, keeping its rate at -0.10% as epxected. Yet the JPY went through a turbulant session and finally weakend against the USD in the European morning. On a more fundamental level, we note that Japan’s Prime minister Kishida is to attend the NATO summit near the end of June, which would be Japan’s first time. The move could instigate substantial frictions in the relationships of Japan with China and Russia, not mentioning North Korea, but strengthen its relationships with western alliance. As for financial releases, we would note practically two from the land of the rising sun. The first would be on Thursday when we get the Jibun Bank preliminary manufacturing PMI figure for June. A possible rise of the indicator’s reading would be signalling a faster expasion of economic activity for the crucial Japanese manufacturing sector. The second would be on Friday, and may be the crown of financial releases for Japan next week as we get Japan’s CPI rates for May. Should the rates accelerate we may see JPY getting some support as that would increase the pressure on BoJ to act. It should be noted that we see risks related to the release as tilted to the upside given the weakening of JPY in the past month. Also note that JPY’s status as a safe haven could be on display once again next week.

EUR – Preliminary PMI figures in the epicenter

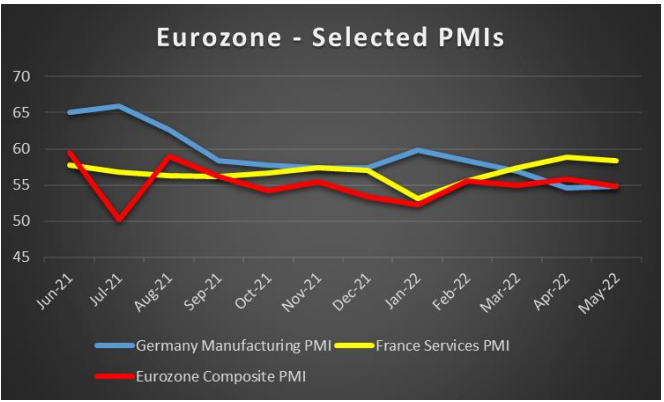

The common currency seems to be losing ground for a third week in a row against the USD. The EUR could end the week lower against the JPY but possibly stronger against the GBP. On a monetary policy level, after ECB’s interest rate decision, which we analysed in last weeks’ report, we note that the bank seems to have reached new decisions, as the possibility of yield fragmentation was visible on the horizon. We note that the spread between the yields of Italian, Greek on the one side and German bonds on the other, widened ringing the alarm bells in the Banks’ headquarters in Frankfurt. In a surprise meeting the bank on Wendesday decided, to flexibly reinvest redemptions coming from the PEPP portfolio “to preserve the functioning of the monetary policy transmission mechanism”. In addition the bank decided to “accelerate the completion of the design of a new anti-fragmentation instrument”. The decision seems to show that the bank is actively moving to stop fragmentation which could be positive for the common currency. Yet, EUR traders may need more evidence for the banks’ decisiveness and ability to produce such an instrument. Also please note that ECB President Lagarde is about to make statements over the weekend and could provide a clearer view on ECB’s intentions. As for financial releases, we note on Wednesday the release of Eurozone’s preliminary consumer confidence, while on Friday we get Germany’s Ifo indicators, both being for June. The crown of financial releases for EUR traders next week though could be the release of the preliminary PMI figures for June expected on Thursday. It should be noted for the record that all the main indicators of France and the Eurozone dropped in May, with the exception of Germany’s manufacturing sector saving the day by rising a bit. Should the readings drop further implying a wider slowdown of the expansion of economic activity we may see the common currency weakening.

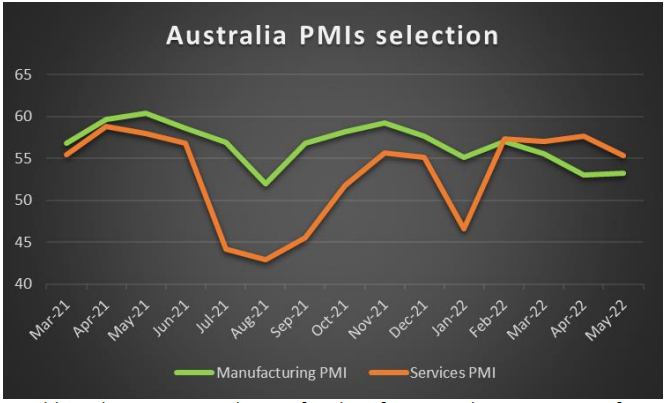

AUD – Low number of high impact financial data

AUD may end the week on the backfoot against the USD. It should be noted that the Aussie briefly gained traction in the past few days after China’s robust industrial data for May was released. It should be noted that China’s industrial output growth rate for May outperformed market expectations escaping negative levels and showing growth once again. The release could imply a greater volume of orders for Australian exporters of raw materials. Moreover, the release of Australia’s employment data for May was in the market’s focus in the past days. Despite the unemployment rate remaining stable at 3.9%, the employment change figure jumped to 60k implying a tightening of the Australian employment market. Such a tightening of the Australian employment market could boost the RBA’s confidence for future interest rate hikes. The central bank had previously linked data regarding employment and inflation to such a scenario. Please also note that in the coming week RBA is to release the minutes of its June meeting during Tuesday’s Asian session and the release could generate substantial interest among AUD traders. Also, on the monetary front we note that RBA Governor Lowe is to make statements on Tuesday’s Asian session and if he sounds hawkish enough may generate some support for the AUD. As for financial releases, we note Australia’s preliminary PMI figures for June on Thursday. Hence, we would expect fundamentals to be in the driver’s seat for Aussie traders next week, and a possible improved market sentiment could provide some support for the commodity currency, which is considered a riskier asset and vice versa.

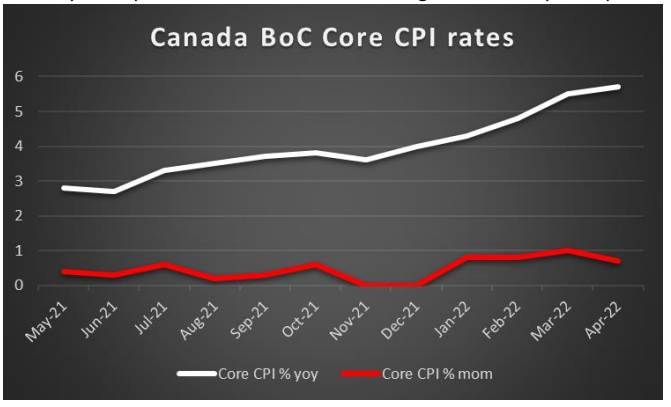

CAD- CPI rates to move the Loonie

The Loonie is weakening against the USD for the second consecutive week. The weakening of the CAD could be partially attributed to the drop of oil prices as well as the wide drop of natural gas prices for the US. Regarding oil, it seems that the surprise rise of US oil inventories as reported by API and the EIA in the past few days tended to weigh, as they would imply a slack in the US oil demand. Oil prices on the other hand could recover on a tight supply side and a firmer global demand outlook. Overall, such fundamentals could imply that the lowering of oil prices could be short-lived and/or shallow. In addition, on Wednesday, US Natural Gas prices managed to regain some of the ground lost on Tuesday but where nowhere near to rebounding. U.S. natural gas futures plunged about 17% to a five-week low on Tuesday on expectations of an extended outage at the Freeport liquefied natural gas (LNG) export plant in Texas, which may allow more gas to refill low U.S. stockpiles and thus could weigh on the CAD as well. On the other hand, on a more fundamental level we note that the commodity currency may prove sensitive to the direction of the market sentiment given that its considered a riskier asset. Should the market sentiment be cautious in the coming week we may see the CAD losing some ground. As for financial releases in the coming week, we note the release of Canada’s retail sales growth rate for April on Tuesday, yet the highlight is expected to be the release of Canadas’ CPI rates for May on Wednesday. Should the rates accelerate further we may see the determination of BoC to curb inflationary pressures through faster and wider rate hikes being hardened, thus providing some support for the CAD. It’s characteristic that economists have issued warnings that BoC may start mirroring the Fed’s 75 basis points rate hikes in an effort to lower inflationary pressures.

General Comment

As a closure, we would like to make a small comment for the interest rate decisions expected in the coming week. We make a start with the Czech Republic’s CNB. The bank has been hiking rates and characteristically in the May meeting proceeded with a 75 basis points rate hike. Yet the CPI rate accelerated further in May reaching 16% yoy, a level not seen for over twenty five years handling probably a shock to CNB policymakers. We would expect the bank to hike rates once again probably with another 75 basis points rate hike, if not even wider and at the same time remain substantially hawkish foreshadowing more rate hikes to come. From Norway on Thursday, we note Norgesbanks’ interest rate decision and we would expect the bank to stick to the script and hike rates in the coming meeting as it remained on hold in the last one and CPI rates accelerated further. It’s interesting to see whether the bank’s forward guidance will be tweaked more to the hawkish side, a scenario which could provide some support for the NOK. Finally, on a more exotic note, we would also like to see how the Central Bank of Turkey acts on Thursday. The bank has maintained its one week repo rate at 14%, with inflation for May accelerating further and reaching 73.50% yoy, while Turkey’s President Erdogan warned that his government will try to lower interest rates even further. Should the bank actually keep rates unchanged once again we may see the Lira starting to weaken. Should the bank show intentions of cutting rates further, we may see the Lira weakening substantially practically sending the Turkish economy in a negative spiral.

Si tiene preguntas generales o comentarios relacionados con este artículo, envíe un correo electrónico directamente a nuestro equipo de investigación a research_team@ironfx.com

Descargo de responsabilidad:

Esta información no debe considerarse asesoramiento o recomendación sobre inversiones, sino una comunicación de marketing. IronFX no se hace responsable de datos o información de terceros en esta comunicación, ya sea por referencia o enlace.