The war in Ukraine is raging and creates high volatility for the markets to either direction. In the coming week, we expect a heavy calendar, full of high impact financial releases and monetary policy events. For starters we highlight FOMC’s interest rate decision on Wednesday, followed on Thursday by Bank of England and the Central Bank of the Republic of Turkey and finally during Friday’s Asian session we get Bank of Japan’s interest rate decision, while on Tuesday RBA is to release the minutes of its last meeting. As for financial releases after a rather quiet Monday , on Tuesday we get Germany’s ZEW indicators for March as well as UK’s employment data for January. On Wednesday we get the US retail sales and Canada’s CPI rates both for February and on Thursday we get Australia’s employment data for February and the US Philly Fed Business index for March. Last but not least on Friday we note the release of Japan’s CPI rates for February and Canada’s retail sales for the same month.

USD – Fed’s meeting to rock the markets

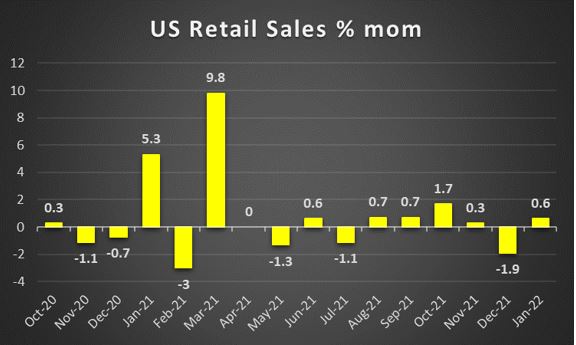

The USD seems to be rather stable after reaching a new high on Monday and correcting lower afterwards. The main event for greenback’s direction next week could be the release of the Fed’s interest rate decision on Wednesday. The bank is widely expected to hike rates and currently Fed Fund Futures imply a probability of 93% for a 25 basis points rate hike. Inflationary pressures in the US economy are at very high levels given also the recent release of the CPI rates for February while the US employment market is tightening to prepandemic levels given also February’s employment report. The question for the Fed is not whether to hike or not, but to what degree it should hike rates. The possibility of a 50 basis points rate hike should not be excluded and if performed could take markets by surprise and provide substantial support for the USD. But its not only about the rate hike. The market will be watching also the new dot plot to understand also how hawkish the views of the Fed’s policymakers are for the future, while the bank’s projections, especially about inflation are expected to be scrutinised by investors and analysts. Last but not least, keep an eye out for the forward guidance provided in the accompanying letter and Fed Chairman Powell’s press conference which is to follow the release. The event is expected to create substantial volatility not only for the FX market but also for US equities markets and gold’s price. As for financial releases from the US we note on Tuesday the PPI rates and on Wednesday the retail sales growth rates both being for February. On Thursday we get the weekly initial jobless claims figure, the Philly Fed Business index for March and the US industrial output growth rate for February, while on Friday we note the release of the existing home sales figure for February.

GBP – Is BoE to deliver another rate hike?

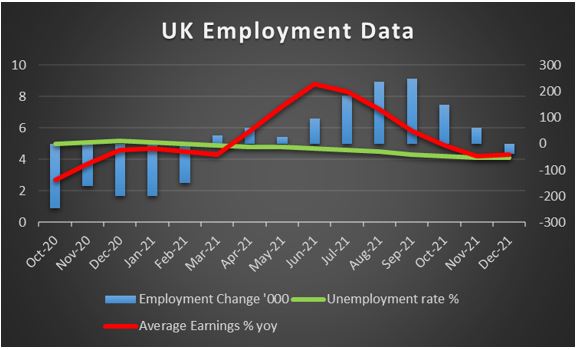

The pound seems about to end the week lower against the USD and the EUR but not the JPY. Pound traders are expected to keep a close eye over BoE’s interest rate decision on Thursday. The bank is widely expected to proceed with a 25 basis points rate hike and its characteristic that the market has currently fully priced in such a scenario materializing, at least according to GBP OIS. The market though seems to price in fully another three rate hikes and partially another one rate hike, until the end of the year which is characteristic of how hawkish its expectations are. So should the bank actually proceed with the rate hike as expected on Thursday a lot about the pound’s reaction may also depend on the forward guidance the bank may provide. Should the bank actually sound hawkish and determined to hike further the interest rate in order to curb the inflationary pressures in the UK economy, we may see the pound gaining further while should the bank seem cautious we may see the pound weakening. To that end we intend to keep also a close watch over the count of the votes for the rate hike to see if anything has shifted in the balance of power within the bank albeit no changes are expected and on second note we would like to see if the bank has any intentions to taper its QE program. As for financial releases next week we would highlight UK’s employment data for January on Tuesday and should the data show that the UK employment market is tightening we may see the pound getting some support.

JPY – BoJ to remain dovishly on hold once again

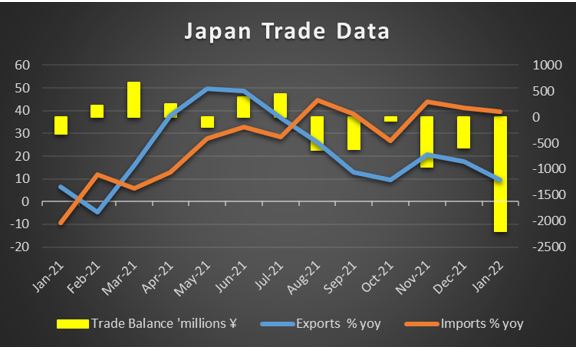

JPY seems to be losing ground against the USD, the EUR and the pound in a sign of safe haven outflows. It should be noted that the risk on sentiment improved somewhat in the past few days which may have had some adverse effects against the Yen. Overall the uncertainty in the global economy caused by the war in Ukraine and the political tensions that have arisen were the primary reason for any gains safe haven JPY may have had in the past weeks. Should the tensions start to ease we may see the Yen experiencing further safe haven outflows and vice versa. On the monetary front, in the coming week we note the release of BoJ’s interest rate decision. The bank is widely expected to remain on hold, keeping rates at -0.10% and JPY OIS imply a probability of 96% for such a scenario to materialise. It’s characteristic that the market widely seems to be pricing in the bank to maintain the current level of rates until the end of the year and beyond. BoJ polcymakers had mentioned in the recent past that the bank would not hike its rates as long as its 2% yoy inflation target is not met. Given that the current inflaiton rate was at 0.5% yoy for January the market’s stance seems to be verified. As for financial releases we would like to note that on Wednesday we get from Japan the trade data for February, on Thursday we get machinery orders growth rate for January and on Friday we note the release of Japan’s CPI rates for February.

EUR – Recovering but uncertainty remains

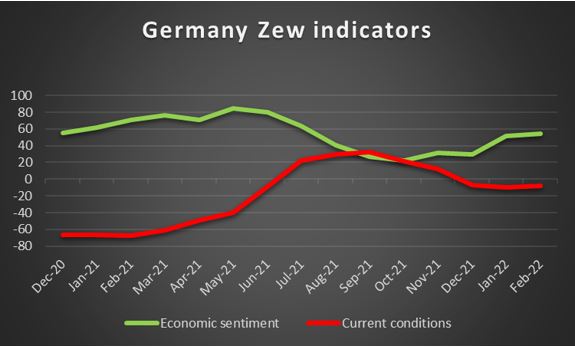

The common currency seems to be recovering some ground against the USD yet is still at rather low levels. In a wider sign of recovery the EUR seems also to be gaining against hte GBP and the JPY. The situation in Ukraine is the main issue worrying EUR traders given that it could have a wide adverse effect on the area’s economy. Some signs of a possible improvement were present in the past few days yet despite some hopes flaring up, negotiators in Antalya Turkey left the table with no deal and no signs of further progress. Overall any signs that a peacefull solution is on the horizon, could provide some support for the common currency and vice versa. On the monetary front we cannot pass unnoticed ECB’s interest rate decision yesterday. As expected the bank kept rates unchanged, but what should be noticed is that the bank also scaled back its stimulus program. On the other hand, the crisis in Ukraine tended to dominate the decision as it creates substantial uncertainty and its characteristic that it is mentioned in the opening paragraph of ECB’s press release. Overall we see the forward guidance as being flexible maybe with a slight degree of creative ambiquity, to allow the bank to follow what action will be necessary depending on future developments. As for financial releases we note for EUR traders the release of Germany’s ZEW indicators for March on Tuesday as well as Eurozone’s industrial production growth rate for January the same day.

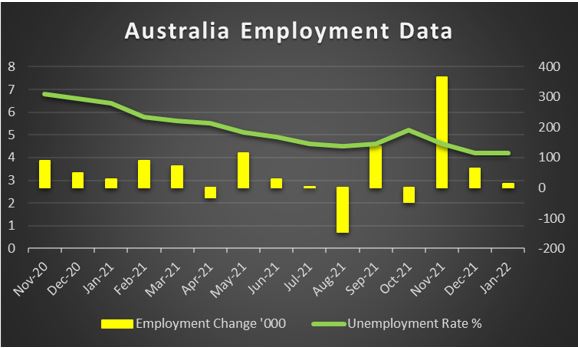

AUD – Employment data in focus

AUD seems to have stabilised this week against the USD, after five weeks of consecutive gains. The correction in the prices of a number of raw materials tended to provide some headwinds for the AUD. Also the seesaw of the market’s mood was not exactly helpful for the Aussie which is considered as a riskier asset. A lower degree of uncertainty and more optimism could provide some support for the AUD in the coming days should it be present in the markets. On the monetary front, there seems to have been some chatter for RBA to hike rates rather sooner than later. It’s characteristic that Goldman Sachs is reported to have brought forward its expectations for a rate hike, probably as early as August and September, while the market seems to be pricing in even more hawkish scenarios by the end of the year. It should be noted that RBA Governor Lowe in statements that he recently made allowed for the possibility for a rate hike by the end of the year yet also mentioned that the bank may have the luxury to wait a little longer than central banks of other developed economies. As for financial releases we note that on Thursday we get from Australia, the employment data for February, especially given the weight that RBA places in the Australian employment market. Aussie traders though may also be interested in the release of China’s industrial output growth rate for February on Tuesday. Please note that on the monetary front RBA is to release the minutes of its last meeting on Tuesday.

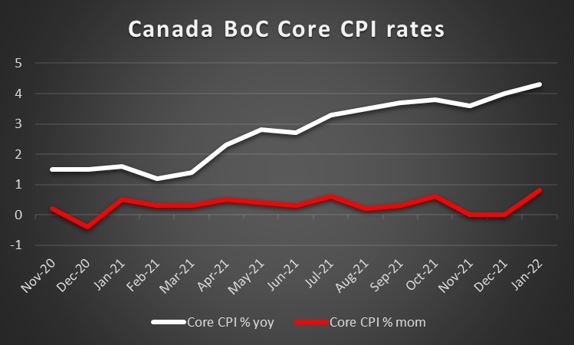

CAD – CPI rates in the epicenter

The CAD seems to remain rather stable against the USD this week, maybe with some slight losses. Please note though that Canada’s employment data for February are still to be released, during today’s American session and could alter the direction of the CAD. On a fundamental level, we note that the Looney did not follow the path of oil prices in their wide downward correction. The possibility of a cease fire in Ukraine, efforts for alternative sources of oil and discussions for the possivility of an increase of oil production tended to contribute to a correction of oil prices albeit we must note that they have not yet reached pre crisis levels. On the monetary front BoC’s hawkish intentions seem to be still present and its characteristic that the market currently prices in another four rate hikes fully, plus one partially until the year’s end. So overall, the interest rate differentials tend to support the CAD currently. As for financial releases we make a start with Tuesday as the housse starts figure for February are due out and on Wednesday we get Canada’s CPI rates for February as well. Finally on Friday we get the retail sales growth rate for January.

General Comment

Overall, as a closure we see the case for war in Ukraine to remain high on the agenda of traders in the coming week as well. Any signs for a possible ceasefire, could provide a more risk on attitude for market participants. However also the contrary is possible should tensions rise, say for example if the Russians decide to enter Kyiv, in which case we may see safe havens gaining and riskier assets retreating. Yet we may also see a substantial part of the market’s interest shifting towards monetary policy issues given the high number of central banks which are due to release their interest rate decisions. Overall, we see the case for the USD to have the initiative over other currencies in the FX market given the frequency and gravity of US financial releases. Once again though, there are releases and events stemming outside of the US borders which could steal the spotlight from the greenback thus allowing for a wider range of trading opportunities.

Si tiene preguntas generales o comentarios relacionados con este artículo, envíe un correo electrónico directamente a nuestro equipo de investigación a research_team@ironfx.com

Descargo de responsabilidad:

Esta información no debe considerarse asesoramiento o recomendación sobre inversiones, sino una comunicación de marketing. IronFX no se hace responsable de datos o información de terceros en esta comunicación, ya sea por referencia o enlace.