US stock markets seem to be taking a breather Just before the Fed releases its interest rate decision and while the earnings season is ongoing. In this report, we are to discuss the earnings scheduled in the coming few days how the Fed’s interest rate decision could affect the markets, what’s coming next and for a rounder view conclude with a technical analysis of the S&P 500.

The Fed’s interest rate decision

The US Equities market this week seems to be focusing on the Fed’s interest rate decision, due out later today. The bank is widely expected to remain on hold and we tend to concur, given also that Fed Fund Futures imply a probability of 98% for such a scenario to materialize. Yet the market also tends to expect extensive rate cuts within the year, hence there is a large question mark looming over the Feds’ intentions and thus the tone of the accompanying statement and Fed Chairman Powell’s press conference later on. On the one hand the easing of inflationary pressures in the US economy as shown also by the latest release of the Core PCE price index for December and the hit on economic activity of the US manufacturing sector tend to suggest that an easing of the Fed’s tight monetary policy is possible. On the flip side, the relative tightness of the US employment market could allow the Fed to maintain rates higher for a longer period than what the market currently expects. Overall should the bank maintain a more dovish tone indirectly reaffirming the market expectations for extensive rate cuts starting from May onwards, we may see equities getting some support as the looser economic conditions in the US may allow for more optimism for the outlook of the US economy.

Earnings reports of GOOGL, MSFT and what’s coming up

The current week is characterised by the earnings releases of mega-cap high-profile tech companies. Alphabet (#GOOGL) outperformed market expectations both on an Earnings Per Share (EPS) level as well as on a revenue level, allowing for a more optimistic outlook for the company to emerge. Yet worries are still present as the revenues from advertising tended to disappoint investors with initial reports indicating that the shares’ price was pushed lower at the after-trading hours, yet we note that the cloud business segment seems once again to be a growth engine for the company. We also note the company’s efforts in the AI sector which is to be embedded in Google’s products. Yet Alphabet’s CEO Pichai, stated that the company has to make cuts elsewhere to promote AI further, a statement that may mean more job cuts within the company. Similarly, Microsoft (#MSFT) also outperformed market expectations for its EPS and revenue figures. The company seems to have a solid footing to advance higher given that its has reported record high revenue for a 5. straight quarter and a jump in earnings, implying also a positive qualitative factor behind the rise of sales. As in Google, AI seems to be a driver for Microsoft as well with the Cloud division being an important segment. It’s characteristic that CFO Amy Hood was reported stating “Growth will be driven by our Azure consumption business with continued strong contribution from AI,”. The statement underscores the importance placed by Microsoft on AI and its Cloud business. In the coming days, we will continue to get earnings reports from mega-cap tech companies, such as Facebook (#META), APPLE (#AAPL) and Amazon (#AMZN). Yet for anyone not interested in the tech sector we also note the release of the earnings reports of Ferrari (#RACE), Deutsche Bank (#DB), Merck (#MRK) and Pinterest (#PINS) on Thursday and Chevron (#CVX) and Exxon Mobil (#XOM) on Friday.

January’s employment report

We note as another big test for equities the release of the US employment report for January on Friday. The unemployment rate is expected to tick up to 3.8%, the average earnings growth rate to remain unchanged at 4.1% yoy and the NFP figure to drop to 180k if compared to December’s 216k. Yet forecasts of the US employment data have been disproven a number of times in the past, thus an element of uncertainty is present for the release which may raise volatility for the markets. Should the actual rates and figures meet their respective forecasts, or be even worse, we may see the US Stock markets gaining as the data may imply a crack in the tightness of the US employment market and exercise more pressure on the Fed for a looser monetary policy.

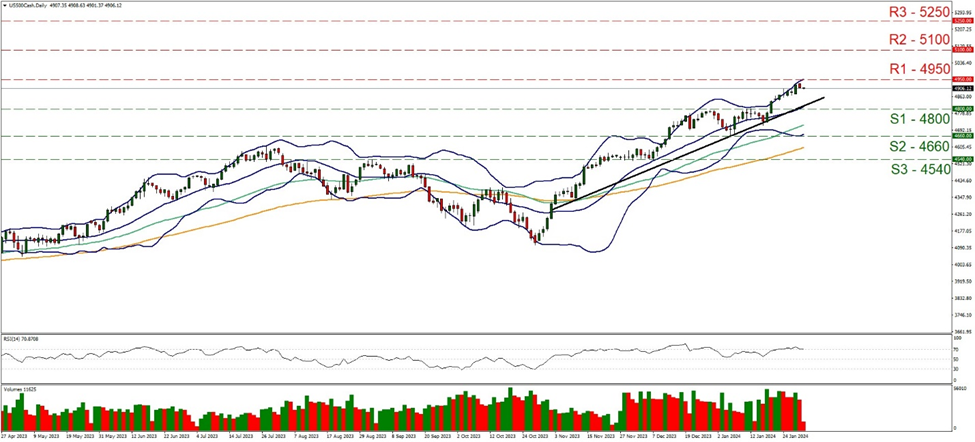

Análisis técnico

US 500 Daily Chart

Support: 4800 (S1), 4660 (S2), 4540 (S3)

Resistance: 4950 (R1), 5100 (R2), 5250 (R3)

S&P 500 edged slightly lower yesterday and during today’s Asian and European session, yet the direction of the index’s price action seems to continue to point towards the 4950 (R1) resistance line. We tend to maintain our bullish outlook for the pair as long as the upward trendline guiding it remains intact. Furthermore, we note that the RSI indicator continues to run along the reading of 70 implying a strong bullish sentiment on behalf of the market, yet the RSI indicator may also imply that the index is still at overbought levels risking a possible correction lower. Should the index find additional buying orders along its path, we may see the index, breaking the 4950 (R1) resistance line and thus open the gates for the 5100 (R2) level while in an extreme bullish scenario we set as the next possible target for the bulls the 5250 (R3) resistance barrier. Should an intense selling interest be expressed by the market we may see the index, breaking the prementioned upward trendline, in a first signal that the upward movement was interrupted and aim for the 4800 (S1) support line. Lower than that we also note the 4660 (S2) support base.