An eventful week is slowly drawing to a close as we open a window into what next week has in store for the markets. On the monetary front, we highlight the release of BoJ’s interest rate decision on Tuesday and also note the release of Turkey’s CBT and from the Czech Republic CNB’s interest rate decisions, both on Thursday. Also, we note the release of RBA’s December meeting minutes on Tuesday and on Wednesday, BoC’s December monetary policy deliberations. As for financial releases, we note on Monday the release of Germany’s Ifo indicators for December and later on New Zealand’s trade data. On Tuesday we note the release of UK’s CBI trends for industrial orders for December and Canada’s CPI rates for November. On Wednesday, we get Japan’s trade data for November, Germany’s GfK consumer sentiment for January, UK’s CPI rates for November, Eurozone’s preliminary December consumer confidence and the US consumer confidence, both being for December. On Thursday, we get the UK’s CBI distributive trades for December and we highlight the final US GDP rate for Q3, the weekly initial jobless claims, the Philly Fed business index for December, and Canada’s retail sales for October. Finally on Friday, we note the release of Japan’s November CPI rates, UK’s GDP rate for Q3 and retail sales for November. In the same day we also get the US consumption rate, the Core PCE price index and the durable goods orders all for November, Canada’s GDP rates for December and the final US University of Michigan consumer sentiment for December.

USD – Fed hints that rate cuts are on the menu next year

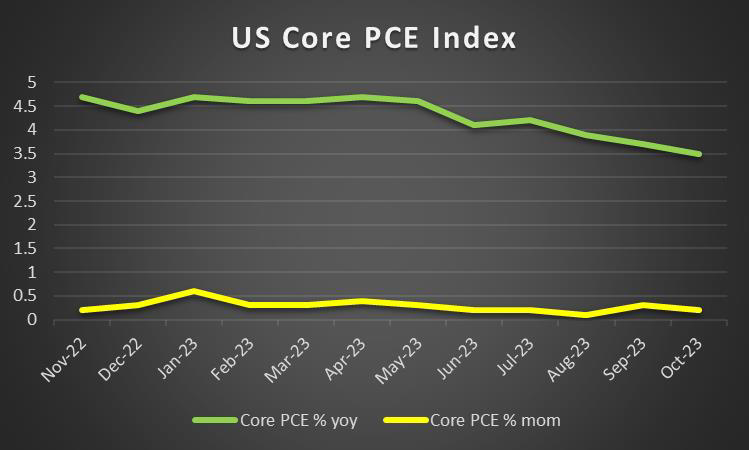

The USD seems about to end the week in the reds against its counterparts, in a sign of general weakness. On a fundamental level, we note that the House of Representatives which has a Republican Majority, voted on Wednesday evening to open impeachment inquiries into President Joe Biden. The potential political instability could weigh on the dollar on a more macro level, as we enter the election period in January 2024. On a monetary level, we note the Fed’s interest rate decision this Wednesday, in which the bank remained on hold as was widely expected. Yet, what was interesting was Fed Chair Powell’s post decision press conference in which he stated that “we believe that our policy rate is likely at or near its peak for this tightening cycle”, implying that the bank may be done with raising interest rates. Moreover, with the Fed’s new dot plot, we note that the majority of policymakers anticipate the Fed’s monetary policy to drop between 4.75 and 4.5%, which is approximately 75 basis points of rate cuts in total for 2024 and appears to support the theory that the Fed may be done raising interest rates. On a macroeconomic level, we note that the CPI rates for November on a mom level, ticked up, yet the 0.1% appears to have been immaterial in the grander scheme of things, and appears to have been widely ignored by the market. Overall we tend to expect the USD to remain under pressure in the coming week, on a monetary level. Looking at what next week has in store for us, we note the Consumer confidence figure for December, the Final GDP rate for Q3, the weekly initial jobless claims figure, the Philly Fed Business index figure for December. Closing off the week is the Core PCE rates for November, which is the Fed’s favourite tool for measuring inflationary pressures, the Consumption rate and the Durable goods orders rate both for November and lastly the University of Michigan consumer sentiment Final figure for December.

GBP – BoE remains on hold

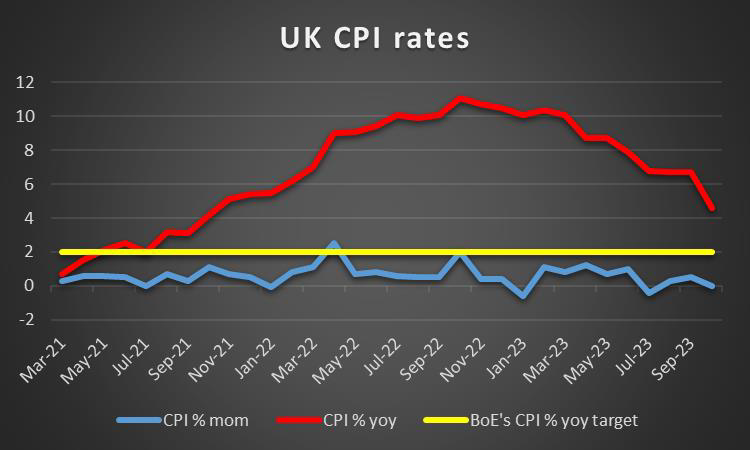

The pound is about to end the week lower against the JPY and EUR, yet stronger against the dollar. On a fundamental level, we note that the political turmoil within the UK continues, with current PM Rishi Sunak, “battling” to keep his Conservative party united, as cracks under his leadership appear to be intensifying. On a monetary level, we note that the BoE remained on hold during Thursday’s monetary policy meeting, as was widely expected. Yet with market expectations of four rate cuts by the BoE next year, BoE Governor Bailey during his press conference, appeared to push back at those expectations by appearing slightly hawkish, having stated “There is still some way to go” when referring to taming the inflation beast. Moreover, the bank stated that “CPI inflation is expected to remain near to its current rate around the turn of the year”, implying that the battle against inflation may not be over, and as such the potential for a tight monetary policy may support the pound. On a macroeconomic level, the UK’s GDP rates for October which were released on Tuesday, came in lower than expected at -0.3% on a mom basis. The lower-than-expected GDP rates, may be concerning for the UK economy and as such could weigh on the pound, should further financial releases imply that the UK economy may be entering a recession in 2024. As such, pound traders may be interested in next week’s CBI trends orders and distributive trade figures for December. Yet we anticipate that traders may be more focused on the UK’s CPI rates for November and should they come in higher than expected in addition to potentially the GDP rate for Q3 coming in lower than expected, we may see heightened fears for a recession weighing on the pound and vice versa.

JPY – BoJ interest rate decision in sight

JPY is gaining ground across the board in a sign of broader strength. The political norm in Japan appears to have been shaken up, with the current Government’s ruling party facing one of the biggest financial scandals in the past decade. Per Reuters, the allegations are in regards of lawmakers receiving roughly $3.5 million in fundraising proceeds which are missing from party accounts. Although the scandal may not have an immediate effect, it could destabilize the Japanese political scene and thus weigh on JPY. Last week, we saw

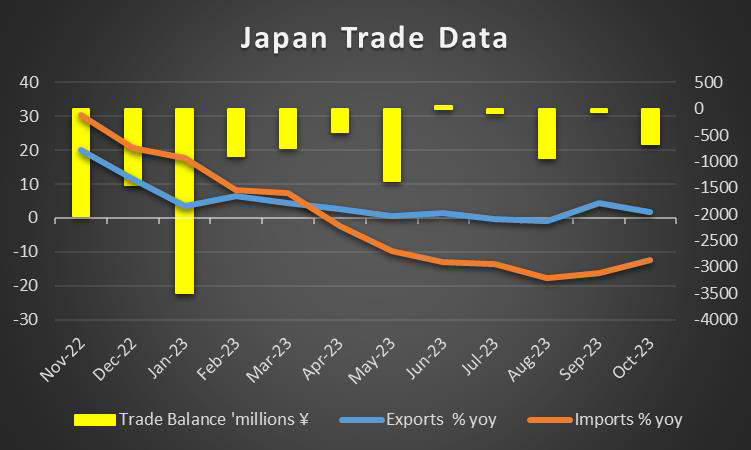

heightened excitement amongst traders that the BOJ was ready to end its decades-long ultra-loose monetary policy. Yet, following a report by Bloomberg, which claimed that BOJ officials see little need to drastically abandon their negative interest rate in next week’s BOJ meeting. The report seemed to tame the market’s expectations of an imminent rate hike. Nonetheless, with the BOJ’s interest rate decision due next week and JPY OIS currently implying a 90.64% probability for the bank to remain on hold, market participants may be more eager to hear BOJ Governor Ueda’s press conference. Overall, should we see the BOJ Governor, providing a timeframe for policy normalization, we may see the JPY gaining, whereas should the Governor push back on expectations of a potential rate hike next year in April, the JPY could weaken. Moreover, should we see more BoJ policymakers gradually hinting at the end of the negative rate policy, it may provide support for the JPY, as it could re-affirm existing expectations of a potential rate hike next year. On a macroeconomic level, the Tankan Manufacturing Index for Q4 came in higher than expected, yet some of our concerns about the outlook and economic activity of the Japanese economy tend to remain. In the coming week, we turn our sights on Japan’s trade balance in an attempt to gauge Japan’s manufacturing competitiveness and economic resilience, whilst the Nationwide CPI rates, may provide insight into the effectiveness of the bank’s current monetary policy in reaching their 2% inflation target.

EUR – The ECB remained on hold

The common currency is about to end the week in the greens against the USD and GBP, yet lower against the JPY for the third week in a row. On a fundamental level, we note that Germany’s government has agreed to a budget deal in order to address a budget gap, following a landmark court ruling. The agreement could ease concerns about Europe’s largest economy, in terms of worsening their current debt-to-GDP ratio. On a monetary level, we note that the ECB kept rates unchanged as was widely expected, yet also note that market expectations are for the bank to start cutting rates in early March and end the year with a total of 6 rate cuts. It should be noted that in the bank’s accompanying statement, it was stated that “ ECB interest rates are at levels that, maintained for a sufficiently long duration, will make a substantial contribution” to reducing inflation, implying that the ECB has reached its terminal rate and as such it could keep the EUR supported. Furthermore, during ECB President Lagarde’s presser, she mentioned a measurement that has not declined which is a concern to the ECB and the measurement is domestic inflation, which may provide additional support for the EUR. Yet we also tend to remain worried about the Eurozone’s manufacturing activity following the release of the Eurozone industrial production rate for October which came in at -0.7%, furthermore despite Germany’s ZEW Economic sentiment improving, the current conditions came in lower than expected, implying that the outlook for Germany’s economy may be improving yet the conditions on the ground still need some work. Hence, we tend to focus also on the release of the Germany’s Ifo business climate figure for December and Consumer sentiment figure for January next week, with some emphasis on the Eurozone’s preliminary consumer confidence figure for December which are due to be released. Yet, based on the ECB’s comments this week, we do not anticipate the releases to have a significant impact on the common currency. Eurozone’s preliminary PMI figures for December proved to be a market mover. Characteristically the contraction of economic activity in Germany’s manufacturing sector is dragging economic activity in the services sector lower Overall the data show a grim picture for Eurozone’s economic outlook and understandably weakened the EUR.

AUD – RBA December meeting minutes due out next week

AUD is about to end the week in the greens against the USD. On a monetary front, we note that RBA’s December meeting minutes are due to be released next week. As such following last week’s monetary policy meeting, in which the bank implied that inflationary pressures in the economy, continue to moderate, traders may be looking for signs that RBA is preparing to cut interest rates. In such an event we may see the Aussie weakening, whereas should the meeting minutes imply that such a scenario may not be on the table yet, we may see the Aussie gaining some support. Yet based on recent indications by RBA officials, we do not expect the latter to be the case. On a fundamental level, we note that the market sentiment may have a wider effect on AUD’s direction, given the Aussie’s riskier asset nature, as it is a commodity currency in nature. On a macroeconomic level, Australia’s employment data came in better than expected, implying that the Australian economy still remains relatively tight, which could further aid the Aussie’s ascent. However, given the close Sino-Australian economic ties, traders may be interested in China’s industrial production rate for November,

which came in better than expected, implying a rebound in China’s economic activity. As such, given their close economic ties, the Aussie may benefit from an improving economic climate in China. We note that we do not anticipate any major financial releases from Australia next week and as such the currency’s direction, may cede control to fundamentals.

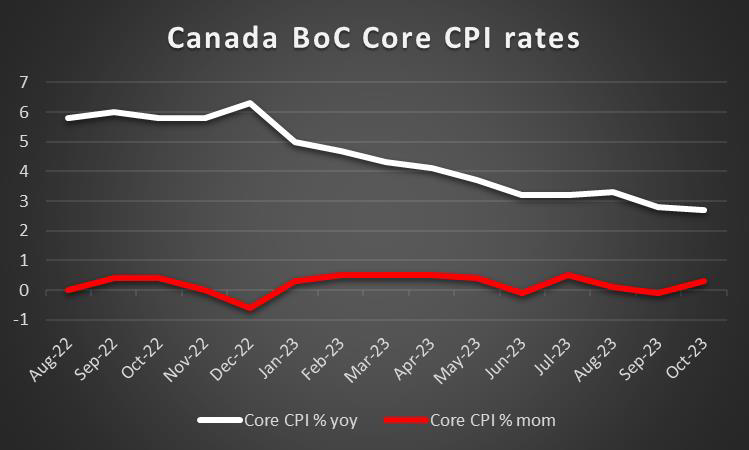

CAD – BoC December monetary policy deliberations due out next week

The Loonie is about to resume its winning streak against the USD and end the week in the greens. On a monetary level, BoC Governor Macklem is due to speak later on today, with traders potentially looking for an indication into the bank’s inclination. Should he sound hawkish, the Loonie may gain and vice versa. Moreover, traders also be interested in the BoC’s December deliberation minutes which are due to be released on Wednesday, given that during the bank’s October deliberations, they had stated that higher global oil prices were standing in the way of the disinflationary process. As such, given the decline in oil prices, it may be interesting for traders to see how the bank may have factored this change into their deliberations and economic outlook for the future. On a fundamental level, we note that oil prices over the week are on track to end relatively higher, which may end oil’s 7-week decline. Should oil prices manage to regain traction, with the bears ceding control to the bulls, we may see the higher prices providing support for the Looney, given Canada’s status as a major oil producer. On a macroeconomic level, we note that Canada’s housing start figure for November is due to be released later on today. However, traders may be more interested in next week’s CPI rates, which should indicate an acceleration in inflationary pressures, we may see the Loonie gaining and vice versa. Furthermore the release of Canada’s GDP rate for October may provide insight into the economic resilience of the Canadian economy and based on our fundamental argument above, we may see a decline in economic growth, which could weigh on the Loonie. On the other hand, should the Canadian economy show signs of growth, we may see the Loonie gaining. Lastly, a testament to the resilience of the Canadian economy on the consumers side, may be the Retail sales rate in October.

General Comment

Overall we expect in the coming week the USD to continue leading the charge over other currencies, given the frequency and gravity of US financial releases. Moreover, we expect volatility to pick up, as we near the end of the year, despite the majority of interest rate decisions having occurred already. In regards to US stock markets, we saw the bulls take over completely, with all three major indexes moving higher and in particular the Dow Jones 30 index, reaching new all-time highs on Thursday, mostly due to the possibility of

more favourable financial conditions, given the Fed’s pivot. Yet we do highlight a small divergence from this week’s market rally, with Microsoft (#MSFT) closing in the reds during Thursday’s trading session, despite the optimistic outlook for the US stock markets. Special focus could be placed on the US Core PCE rates which are the Fed’s favourite tool for measuring inflationary pressures. In addition, gold’s price tended to reverse trajectory, and it’s currently moving higher, once again highlighting its negative correlation with the USD. We also note that the US bonds in particular the 5-Year and 10-Year moved lower for the week, as the Fed implied that the door for rate cuts next year, is wide open. Lastly, we note our continued concern over the escalating tensions between Venezuela and Guyana, as any military conflict could destabilize the region and lead to higher oil prices, given the two nations’ status as oil-producing countries.

Si tiene preguntas generales o comentarios relacionados con este artículo, envíe un correo electrónico directamente a nuestro equipo de investigación a research_team@ironfx.com

Descargo de responsabilidad:

Esta información no debe considerarse asesoramiento o recomendación sobre inversiones, sino una comunicación de marketing. IronFX no se hace responsable de datos o información de terceros en esta comunicación, ya sea por referencia o enlace.