Market worries for a US default on a fundamental level, remain strong as we glance into what next week has in store for the markets. On the monetary front, we expect a relatively quiet week, yet policymakers from various central banks are scheduled to make statements that could sway the market’s mood. As for financial releases after a rather easy-going Monday, we note on Tuesday the release of Australia’s Preliminary building approvals rate, Switzerland’s and the Czech Republic’s GDP rates both for Q1 and we note the US Consumer Confidence figure for May. On Wednesday, we note the release of Japan’s Preliminary industrial production rate for April, China’s NBS Manufacturing PMI figure for May France’s GDP rate and Turkey’s GDP rate both for Q1, followed by Germany’s preliminary HICP rates for May, Canada’s GDP for Q1 followed by the US JOLTS job openings figure for April. On a busy Thursday, we get Australia’s retail sales for April, China’s Caixin Manufacturing PMI figure for May and during the European session we note Germany’s, the Eurozone’s and the UK’s Manufacturing final PMIs all for the month of May, followed by the Eurozone’s HICP rate for May and Unemployment rate for April. During the American session, we note the weekly US Initial jobless claims figure followed by the ISM Manufacturing PMI figure for May. Lastly, the highlight of the week is expected to be the US-dominated Friday with the US employment report for May.

USD – US tip-toes around a debt ceiling deal

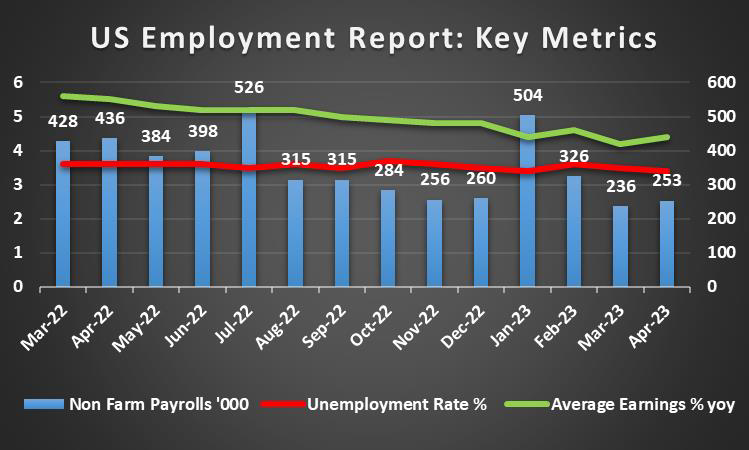

The USD seems to end the third week in a row, higher against its counterparts. On a fundamental note, we highlight the progress being made by key Republican and Democratic leaders during this week, as to raising the US debt ceiling. Following a four-hour meeting between President Biden and House Speaker McCarthy in the White House this Wednesday, with the two leaders hinting that there were positive developments made on both fronts. However, during the past weekend, Speaker McCarthy indicated that the two sides were not close to a deal, highlighting the delicate nature of the negotiations on a day-by-day basis. On the monetary front, we note the release of the Fed’s FOMC May meeting minutes, which were indicative that the Fed might pause rates sooner rather than later. This could be deduced from the meeting minutes in which policymakers agreed that “additional increases in the target range may be appropriate after this meeting had become less certain”. On a macroeconomic level, we note the fact that the US Preliminary S&P Manufacturing PMI for April came in below the figure 50, indicating a contraction in economic activity for the sector as the 50 figure serves as a cut-off point between expansion and contraction. However on the contrary the US 2nd GDP estimate appears to have ticked upwards in comparison to the preliminary releases which may imply that the situation may not be as bad as initially expected. Looking ahead, we note that greenback traders will likely place heavy emphasis on next week’s Non-Farm Payrolls and Unemployment rates for US during the month of May, which are anticipated by analysts to weaken the dollar, given forecasts for the NFP figure to drop and the unemployment rate to rise.

GBP – BoE admits failures regarding inflation predictions

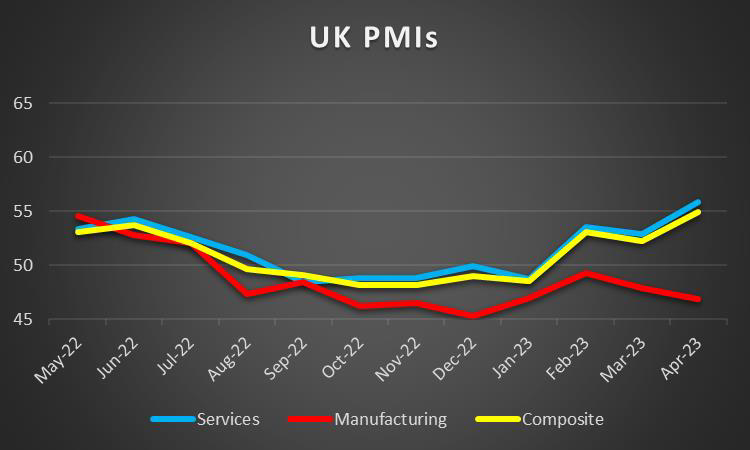

The pound is about to end the week higher against the Yen, yet lower than the dollar and the euro. On a fundamental note, we note the continued reduction in confidence by investors in the London stock exchange as UK regulators forced Meta (#FB) to sell the image platform Giphy to Shutterstock, citing competition concerns. On a monetary level, we highlight BoE Governor Bailey’s statements on Wednesday, who acknowledged that there are “very big lessons to learn”, referring to the bank’s failure to properly forecast inflationary pressures. Furthermore, MPC member Hugh Pill re-iterated comments made by Governor Bailey, stating that “We are trying to understand why we have made errors in inflation forecasts”, startling investors who could now question whether or not the bank’s revision of the UK’s GDP growth rate is accurate. On a macroeconomic level, we note the CPI rate for April which actually ticked up, on a month-of-month level whilst the year-on-year slowed down yet not as much as the market expected. Market expectations are for BoE to proceed with more rate hikes which could provide some support to the pound on a monetary level. On a macroeconomic level, UK’s Preliminary PMI figures decreased with the Manufacturing industry experiencing a worsening contraction of economic activity. Furthermore, we highlight the release of UK’s Retail sales growth rate for April which accelerated on a MoM basis beyond market expectations implying that the demand side of the UK economy may continue to fuel inflationary pressures.

JPY – JPY continues facing safe haven outflows once again

The JPY is about to end the week in the reds against the common currency the pound and the greenback in a sign of a wider weakening. Fundamentally, the JPY has been experiencing safe haven outflows since progress has been made on raising the US debt ceiling, yet we highlight the fact that until a deal is reached, the yen could receive safe haven inflows should a no-deal scenario be materialized until the 1st of June. On a monetary level, we note BoJ Governor Ueda who stated last Friday that “The cost of prematurely shifting policy, and nipping the bud towards achieving 2% inflation, is extremely large”, reducing expectations of an upheaval of his predecessor’s YCC policy. However, the Governor stated yesterday that should Japan’s CPI fail to slow down in line with projections, the bank will act swiftly, a rather unusual statement from a BoJ Governor, which could, in turn, spark some support for JPY. On a macro level, we note the release of Japan’s Tokyo CPI rates that were released during today’s Asian session, which were indicative of reduced inflationary pressures, as they slowed down beyond market expectations.

EUR – Will France’s GDP rates next week, simulate those of Germany?

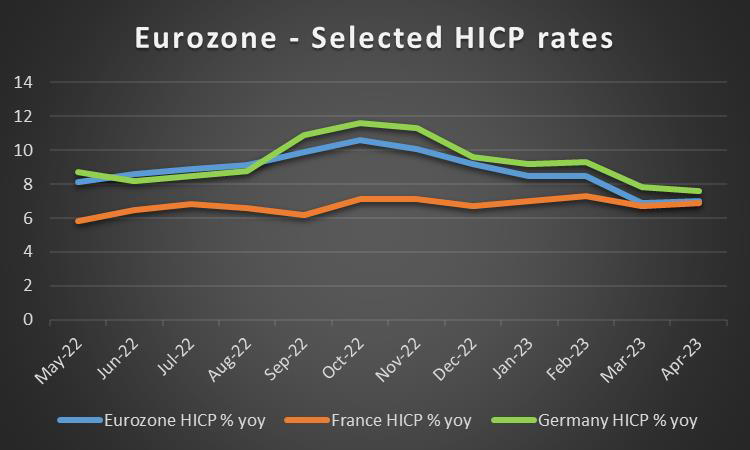

The common currency weakened against the dollar but not the pound and the Yen. Fundamentally, we note a number of strikes in the transportation industry, with airline unions announcing a 24-hour ground handling strike at airports on the 4th of June and a 24-hour Nationwide bus, train and tram strike today. The major disruptions despite being temporary, could have long-lasting economic implications should they be prolonged during the peak tourism season in Europe. On a monetary front, we highlight the numerous ECB policymakers such as ECB President Lagarde, Vice President De Guindos, ECB’s Nagel and ECB Villeroy De Galhau who all re-iterated the need for further rate hikes in order to combat inflation. Despite the continued hawkish rhetoric from policymakers, the euro appears to have failed to make significant gains as market analysts had already taken future rate hikes into account. On a macroeconomic level, Germany’s GDP rate for Q1, ticked downwards and effectively placed the German economy in a recession. With Europe’s largest economy in a technical recession, pressure on ECB policymakers may be mounting to ease on the aggressive rate hiking path. Should France’s GDP rates for Q1 which are due next week also decline more than what is anticipated then we may see heightened market volatility, given that the two largest economies in Europe are slowing down and could have a negative impact on the euro. Interestingly Europe’s preliminary HICP rate for May is due out next Thursday, where should it tick upwards we may see the political forces battle within the ECB, whose core mandate is to reduce inflation.

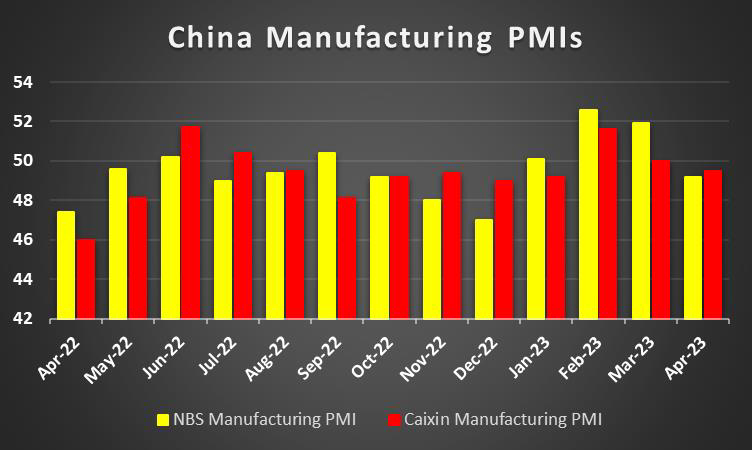

AUD – Australia gradually seeks to reduce its dependence on China

The Aussie appears to have significantly weakened against the USD as the week draws to a close. On a fundamental note, we highlight the meeting between Indian President Modi and Australian Prime Minister Albanese, where the two leaders agreed on a new hydrogen task force, meant to promote cooperation on gas production without the need for fossil fuels. Furthermore, the two leaders noted that the free-trade deal negotiations are expected to be finalized before the end of the year, reducing Australia’s dependence on China. On a monetary note, we note no major announcements by RBA yet the bank’s Governor, Phillip Lowe is scheduled to speak on Tuesday, as we near the next RBA interest rate decision on the 6th of June. On a macroeconomic level, we note that Australia’s Preliminary Manufacturing figure was better than expected, yet failed to provide long-term support for the Aussie as the greenback’s dominance was evident throughout the week. On the contrary, Australia’s Preliminary Retail sales for April, slowed down more than expected, reaching stagnation levels and hinting towards the adverse effects of RBAs’ monetary policy tightening on the demand side of the Australian economy. Lastly, traders may set their sights on China’s NBS and Caixin Manufacturing PMI figures next week which are anticipated to increase, thus as China being the largest importer of Australian goods, we may see the Aussie strengthening should the actual figures meet their respective forecasts, as the data could indicate the potential for increased demand of Australian goods.

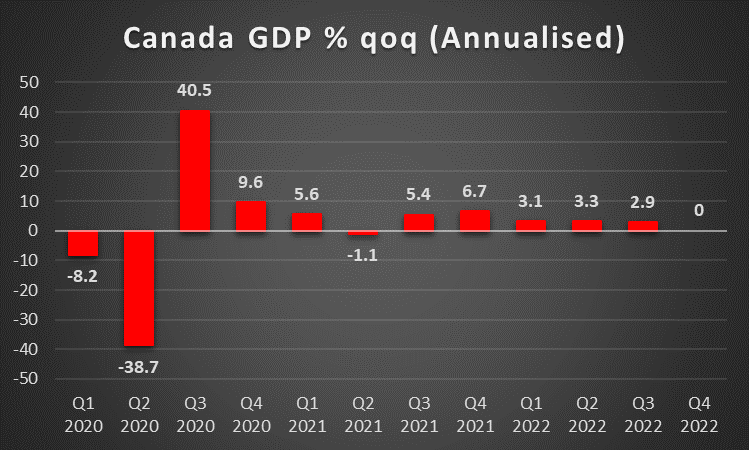

CAD – Alberta wildfires appear to be under control

The Loonie appears to have lost ground against the dollar for the week. Fundamentally we note that the wildfires in the Alberta region, appear to have subsided and eased concerns for the region’s oil and gas outputs. Furthermore, we note that Toronto Dominion, one of Canada’s largest banks, announced a plan to buy back its shares following the failed acquisition of First Horizon, thus increasing consumer confidence in the country’s banking sector. On a monetary tone, we note the lack of press releases by the BoC, which may have contributed to the CAD’s losses. On a macroeconomic level, we note that despite the reduction in the Preliminary Manufacturing sales, it appears that traders were unphased and continued to support the Loonie, as traders eagerly await the release of Canada’s Preliminary Wholesale Sales rate which is due out during today’s American session. Lastly, we note that market attention is expected to shift to next week’s GDP rate for Q1, where should the GDP rate come in higher than expected, it could facilitate Loonie’s rise, whereas a lower-than-expected figure could weaken the CAD. We should note that oil’s price seems about to end the week relatively unchanged and may on a fundamental level provide some support for the CAD should its price start rising in the coming week as well, as Canada is a major oil-producing economy.

General Comment

As a general comment we expect, that the high impact of the financial releases on combination with the continued US debt ceiling drama, to keep traders on high alert as we near the ‘X-Date’ which has been indicated to be as soon as June 1st by some analysts. Also given that the majority of companies have already released their financial earnings for Q1 we have a relatively quiet earnings week with no major releases expected. On a fundamental level, US stock market participants have lost ground this week due to the debt ceiling fears, yet the outlier appears to be the NASDAQ which has been propelled upwards as a result of NVIDIA’s earnings report which beat market expectations, with the firm nearing a $1 trillion market cap. We tend to maintain some worries for the market’s AI enthusiasm, as it may turn out to be the next dot com bubble. We do not reject AI as such but still view the market’s excitement as too high at the current stage which may allow for a number of companies to enter US stock markets without substantial background and prospects. Furthermore, gold’s price seems about to end lower for a 3rd week in a row. The shiny metal may have seen safe haven outflows as debt ceiling talks have slightly progressed, in addition to a strengthening dollar, have alleviated downward pressures on the gold bullion thus straying further away from the $2000 key psychological barrier.

Si tiene preguntas generales o comentarios relacionados con este artículo, envíe un correo electrónico directamente a nuestro equipo de investigación a research_team@ironfx.com

Descargo de responsabilidad:

Esta información no debe considerarse asesoramiento o recomendación sobre inversiones, sino una comunicación de marketing. IronFX no se hace responsable de datos o información de terceros en esta comunicación, ya sea por referencia o enlace.