As the week is nearing its end, we have a look at what next week’s calendar has in store for the markets. We make a start on Monday with China’s final Caixin manufacturing PMI figure, Turkey’s CPI rate, Germany’s final manufacturing PMI figure, the UK’s manufacturing PMI figure, the Zone’s preliminary HICP rate, Canada’s manufacturing PMI figure and the US ISM manufacturing PMI figure all for the month of January. On Tuesday we get the US factory orders rate and US JOLTs job openings figure both for December and New Zealand’s unemployment rate for Q4 2024. On Wednesday, we make a start with China’s Caixin services PMI figure, France’s Services PMI figure, the Eurozone’s final composite PMI figure, the US ADP employment figure all for January, followed by Canada’s trade balance figure for December, the US S&P services PMI figure and ISM Non-Manufacturing PMI figures both for January. On Thursday we get Australia’s trade balance figure for December, Switzerland’s unemployment rate for January, Germany’s industrial orders rate for December, Sweden’s and the Czech Republic’s preliminary CPI rates for January and Canada’s Ivey PMI figure for January. Lastly, on Friday we get the UK’s Halifax house prices rate, the US and Canada’s employment data all for January and ending off the week is the US University of Michigan preliminary consumer sentiment figure for February.

USD – Fed to remain on hold?

Starting on a monetary level, we note the Fed’s interest rate decision which occurred this Wednesday. The Fed remained on hold at 4.5%, as was widely expected by the majority of market participants, with FFF having priced in a 99% probability for such a scenario to occur. In turn, we will focus on the Fed’s accompanying statement and Fed Chair Powell’s press conference in order to acquire a better understanding of the possible intentions of the Fed’s current leanings. Starting with the accompanying statement, we note that the Fed appears concerned about the economic outlook, potentially as a result of the new US administration’s economic policies. Moreover, some concern also appears to linger in regards to inflationary pressures in the US economy, with the Fed stating that it remains “somewhat elevated”, and Fed Chair Powell stating during his press conference that “We do not need to be in a hurry to adjust our policy stance”. Overall, it would appear the Fed may slow down their monetary easing cycle, which in turn could be perceived as relatively hawkish in nature and could thus aid the dollar.

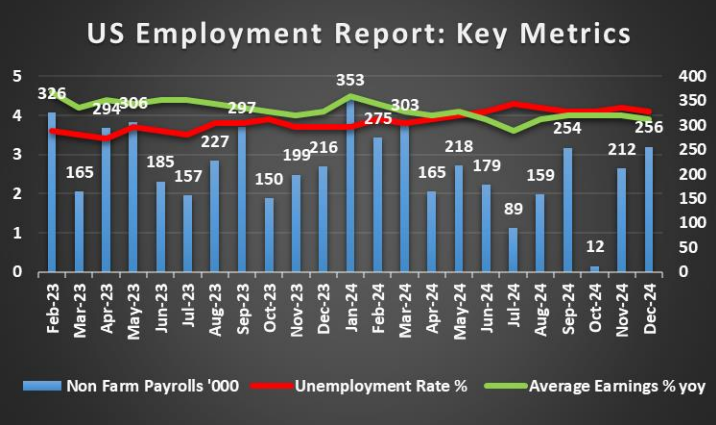

On a macroeconomic level, we that the US Core PCE rates which are the Fed’s favourite tool for measuring inflation, have yet to be released at the time of this report. The Core PCE rate for December on a YoY is expected to come in at 2.8%, which could imply that inflation remains elevated and in turn could imply that the rate cutting approach may be more gradual. In the event that the rate comes in lower than expected, it could intensify calls for the Fed to resume cutting rates, which may weigh on the dollar and vice versa. Lastly, we must mention the US Employment data which is due out next Friday, where a resilient labour market could provide leeway for the Fed to prolong their “hold” period and vice versa.

Analyst’s opinion (USD)

“We are not surprised to see the Fed adopt a ‘wait and see’ approach as the new administration’s economic policies and in particular their tariff ambitions are relatively ambiguous. Specifically, the 1st of February which is tomorrow, has been touted as the day where tariffs on Canada and Mexico will be imposed. In our view, we would not be surprised to see tariffs being imposed over the weekend and seeing Fed policymakers re-iterating Fed Chair Powell’s comments in the coming week.”

GBP – BoE decision next week

The BoE’s interest rate decision is set to occur next week, with the majority of market of market participants currently anticipating the bank to cut rates by 25 basis points, with GBP OIS currently implying an 85.4% probability for such a scenario to materialize. In turn, we would turn our attention to the bank’s accompanying statement in which should the BoE reference measures to support economic growth, it may be perceived as dovish in nature which could weigh on the pound. On the other hand, should the BoE imply that they may withhold from further cutting rates in the near future, it may aid the GBP.

On a macroeconomic level, we note that it was a relatively quiet week for pound traders with no major financial releases stemming from the UK. For next week, we would like to note the release of the UK’s manufacturing PMI figure for January which is set to be released on Monday. The prior figure came in at 48.2 implying a contraction in the UK manufacturing sector. As such, should the figure showcase an improvement in the manufacturing sector, either in the form of a smaller contraction or entering into expansionary territory, it could provide support for the GBP. On the other hand, should it showcase a widening contraction it could weigh on the pound.

Analyst’s opinion (GBP)

“In the coming week, we look forward to the BoE’s rate decision in which the bank is widely expected to cut rates by 25bp. In our view, we would not be surprised to see the bank cutting rates by 25 basis points, with the accompanying statement potentially being relatively dovish in nature. Moreover, at the same time we would not be surprised to see some concern from policy”

JPY – BoJ on track for more rate hikes?

On a monetary level, we would like to discuss the recent comments made by BOJ Deputy Governor Ryozo Himino. The BOJ Deputy Governor stated per Bloomberg that “Looking ahead, it depends on the economy, prices and financial circumstances, but if our economic and price outlooks are realized, we’ll hike rates accordingly”. Essentially, it appears that the Deputy Governor’s comments are hawkish in nature and thus should further policymakers re-iterate the hawkish remarks, it could aid the JPY.

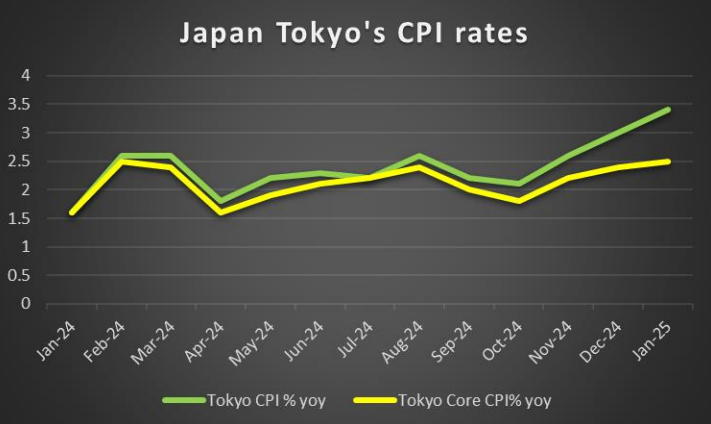

On a macroeconomic level, we highlight the acceleration of the BOJ Core CPI rates for January. The release highlighted the resilience of inflationary pressures in the Japanese economy which could further support the aforementioned comments made by BOJ Deputy Governor Ryozo. Furthermore, the release of the Tokyo CPI rates on a YoY basis for January showcased an acceleration of inflationary pressures in the economy, hence validating the aforementioned BOJ Core CPI rates. Overall, the financial releases could increase pressure on the BOJ to adopt a more hawkish tone, which in turn could aid the JPY.

Analyst’s opinion (JPY)

“The BOJ continues to be poised to continue hiking rates during the year, during a period where other central banks are expected to cut rates. In our view, with the BOJ seemingly poised for future rate hikes, we would not be surprised to see the JPY strengthening and thus should other policymakers re-iterate hawkish remarks it could further aid the Yen”

EUR – ECB cuts rates as expected

On a monetary level, we highlight ECB’s interest rate decision which occurred yesterday. The bank cut interest rates by 25 basis points, as was widely expected by market participants. In the bank’s accompanying statement, it was stated that “Most measures of underlying inflation suggest that inflation will settle at around the target on a sustained basis”, implying that the bank has some leeway should they wish to continue cutting rates in the future. Moreover, during the post-decision press conference, ECB President Lagarde stated that the euro-area economy “is set to remain weak in the near term”. In turn, this may be perceived as dovish in nature, with the ECB President potentially implying that the bank may continue on their rate-cutting path, which may weigh on the common currency.

On a macroeconomic level, the euro-economy is not looking good either.w are not looking that good either. Specifically, France’s, Germany’s and the Zone’s preliminary GDP rates for Q4 all came in lower than expected, with Germany’s economy remaining in contraction territory. The economic resilience of the Zone and the major economies in it, continue to be troubling and should the financial releases continue to paint a dire picture, it could weigh on the EUR. For next week, we would like to point our sights on the Eurozone’s preliminary HICP rate for January. Should the HICP rate showcase an acceleration of inflationary measures, it could potentially aid the EUR, as the bank may need pump the breaks on their rate-cutting approach. Yet, with the economic situation in the Zone, it may spark concerns about a euro-area recession which in itself could weigh on the common currency instead. Lastly, should the HICP rates showcase easing inflationary pressures, then it could validate the ECB’s rate cutting approach which in turn could weigh on the EUR.

Analyst’s opinion (EUR)

“The Eurozone’s economic situation continues to be in trouble, as showcased by the preliminary GDP rates for Q4 which were released this week. In our view, the ECB may have no other option but to continue cutting rates should the economic situation worsen. However, should inflationary pressures resurface or even accelerate and thus cast doubt on the bank’s 2% inflation target being sustainably achieved, the EUR could enter a new realm of uncertainty and volatility”

AUD – CPI rates showcase easing inflationary pressures

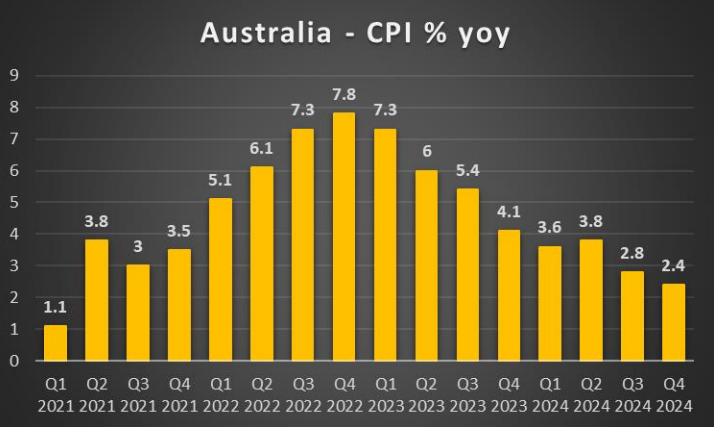

On a macroeconomic level, we note the release of Australia’s CPI rates for Q4 2024, which came in lower than expected. The lower-than-expected inflation print, implies that inflationary pressures in the Australian economy may be easing. In turn, easing inflationary pressures may increase pressure on the RBA to begin cutting rates in their next meeting and could thus weigh on the Aussie. For next week, of interest to Aussie traders may be the release of Australia’s trade balance figure for December which is due out on Thursday. An improvement of the trade balance figure could aid the AUD and vice versa.

On a fundamental level given the close economic ties with China, of interest to Aussie traders may also be the release of China’s Caixin manufacturing PMI figure for January which is expected to remain steady at 50.5. Such a scenario could aid the Aussie, as a continued expansion of China’s manufacturing sector, could imply an increase in demand for raw materials stemming from Australia. On the other hand, should the figure come in lower than expected and imply a lower-than-expected expansion or perhaps even a contraction of the manufacturing sector, it could weigh on the AUD.

Analyst’s opinion (AUD)

“The lower-than-expected CPI rates may be the justification the RBA needs to cut interest rates in their next meeting. As such, we would not be surprised to see RBA policymakers potentially hinting to a rate cut in their next meeting in February, which in turn could weigh on the AUD. Moreover, we are concerned about the potential tit-for-tat tariffs that may be imposed by the US and China, which could inadvertently hinder the Australian economy.”

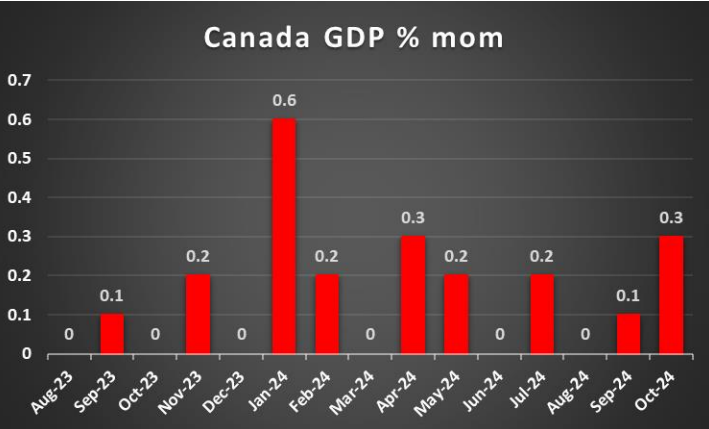

CAD – BoC cuts by 25bp as expected

On a monetary level, we note the decision by the Bank of Canada earlier on this week, in which the bank cut interest rates by 25 basis points, as was widely expected. In the bank’s accompanying statement, it was stated that “A broad range of indicators, including surveys of inflation expectations and the distribution of price changes among components of the CPI, suggests that underlying inflation is close to 2%.” Essentially implying that the bank is on track for its 2% inflation target and could thus continue cutting interest rates, which may weigh on the Loonie. However, of interest was also another comment in the accompanying statement, which tended to showcase that BoC policymakers have taken note of the possibility of tariffs being imposed by the US. Specifically, it was stated that “a protracted trade conflict would most likely lead to weaker GDP and higher prices in Canada.” This may be of concern, as a weaker economy could lead to a looser labour market, whereas higher prices could imply an increase in inflationary pressures as well.

On a macroeconomic level, we note that President Trump has threatened tariffs on Canadian exports to the US of approximately 25%, which may come into effect on the 1st of February which is tomorrow. In such a scenario, it could weaken the Canadian economy as mentioned by the BoC and could thus weigh on the Loonie. For next week traders may be interested in the release of Canada’s employment data which is due out next Friday. A loosening labour market could weigh on the CAD and vice versa.

On a fundamental level, given Canada’s status as an oil exporting nation, the continued decline in oil prices over the past week may have also weigh on the CAD.

Analyst’s opinion (CAD)

“In the coming week, CAD traders may be interested in the Canadian employment data. Yet, should tariffs be imposed from the US, that narrative may be overshadowed. In our view, we would not be surprised to see tariffs being imposed by the US on Canada over the weekend which in turn could weigh on the CAD.”

General Comment

Overall, we expect the USD to maintain the initiative over other currencies in the FX market given that he gravity and frequency of the US fundamentals are key to the market’s direction. Other currencies may come under the spotlight at certain points over the week such as the pound. As for US stock markets we note that the markets were spooked earlier on this week following the announcement of DeepSeek’s AI assistant, who called into question the AI dominance of the US tech sector. Also, US President Trump is expected to announce tariffs on Canada and Mexico over the weekend, As for gold’s price we note its bullish outlook with its upward motion has been maintained over the course of the week.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.