We take a look at what next week has in store for the markets. On the monetary front, we note the release of the RBA’s March meeting minutes on Tuesday and the speech by Fed Chair Powell on Wednesday. In terms of financial releases, we make a start on Monday with Japan’s Tankan Big manufacturing and non-manufacturing indexes figures both for Q1, followed by China’s Caixin manufacturing PMI figure and the US ISM Manufacturing PMI figure both for the month of March. On Tuesday, we get the UK’s Nationwide house price rate for March and the US Factory orders rate for February. On Wednesday we get Turkey’s CPI rates the Eurozone’s Preliminary HICP rates and the US ISM-Non Manufacturing PMI figure all for the month of March. On Thursday, we note Switzerland’s CPI rate, the Eurozone’s final composite PMI figure and the UK’s final service PMI figure all for the month of March, followed by the US weekly initial jobless claims figure and Canada’s trade balance figure for February. Lastly, on a busy Friday, we get Germany’s industrial orders rate for February, UK’s Halifax house prices rate, US Employment data and Canada’s Employment data all for the month of March.

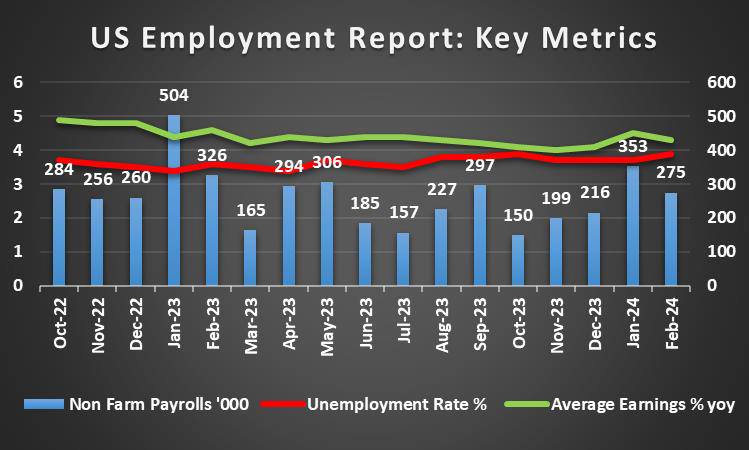

USD – US Employment data due out next week

The greenback is about to end the third week in a row in the greenss against its counterparts. On a monetary level, we note the intensifying rifts between Fed policymakers regarding the bank’s direction. In particular, Fed Governor Cook and Chigaco Fed President Goolsbee implied that current data appears to be on track with the bank’s expectation of easing inflationary pressures. On the flip side, Fed Governor Waller seemed to upend the dovish sentiment that emerged earlier on in the week, having stated on Wednesday evening that “no rush to begin cutting interest rates… or to ease monetary policy”, sending speculators into a frenzy. Overall, we believe that a tug of war may emerge from Fed policymakers, over when it may be appropriate for the Fed to begin easing its monetary policy stance and thus could keep volatility high in the dollar, heading into next week. On a macroeconomic level, we note that the Durable goods orders rate for February exceeded expectations, which may have supported the dollar following its release. However, the highlight so far has been the release of the US GDP rate for Q4 which came in better than expected, at 3.4% qoq (annualised), implying that the US economy is resilient, in spite of the Fed’s restrictive monetary policy. Moreover, the goldilocks scenario with the University of Michigan figures for March where inflation expectations came in lower than expected, yet consumer optimism exceeded expectations, may provide support for the dollar,

as the economy appears to be fairing well from the consumer’s persective. Yet, we must note that the Core PCE rates for February which are the Fed’s favourite tool for measuring inflationary pressures are due to be released this afternoon. Economists are currently expecting the Year-on-Year rate to remain steady at 2.8%, which would imply persistent inflationary pressures in the US economy, and as such could dampen the market’s aforementioned hopes for easing monetary policy this year, thus supporting the USD. On the flip side, the Month-on-month rate is expected to increase at a decreasing rate of 0.3%, which would imply easing inflationary pressures, thus potentially hindering the dollar’s ascent. Next week the highlight for dollar traders may be the US Employment data for March, in which should a resilient labour market picture emerge for a 3rd month in a row, could support the dollar. Whereas a loosening labour market could weigh on the dollar, as the pressure on the Fed to maintain its hawkish stance may ease. Of secondary importance in our opinion is the release of the US ISM Manufacturing and non-Manufacturing PMI figures for March which are expected by economists to improve and thus could support the dollar leading up to “NFP Friday”.

GBP – UK’s GDP Rates confirm recession territory

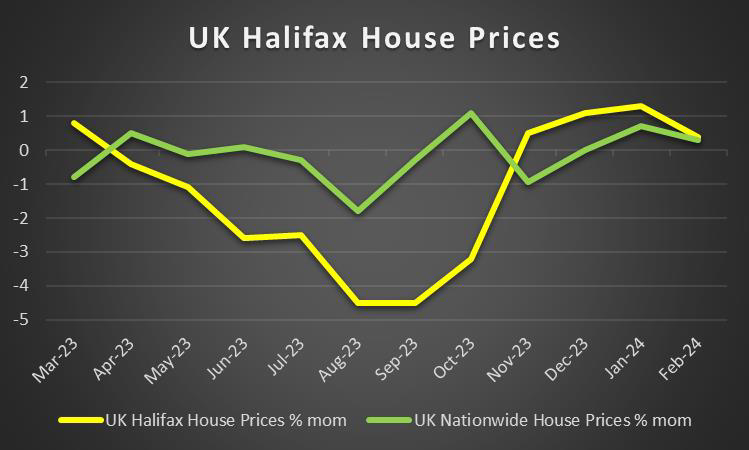

The pound is about to end the week stronger against the EUR and to a smaller degree stronger against the USD and the JPY. On a monetary level, we highlight BoE Mann’s comments this week in which she said that “markets are pricing in too many rate cuts”. The comments were made in addition to BoE Haskel’s comments that interest rate cuts should be a “long way off”, and may have alleviated some of the bearish tendencies on the pound since last week’s interest rate decision. Should more BoE policymakers adopt a more hawkish stance, we may see the pound slightly recovering some ground, yet in our opinion for the pound to recover some ground against its counterparts, it may need a helping hand from external forces besides BoE. As the GDP rate for Q4 came in as expected at -0.3% qoq, validating worries that the UK economy continues to remain within negative teritory, entering a shallow recession tending to darken the macroeconomic outlook of the UK. In the coming week, we note the release of the UK’s Nationwide house prices for March and the final services PMI figure for March as well, although we do not anticipate these financial releases to materially impact the pound.

JPY – JPY intervention inbound?

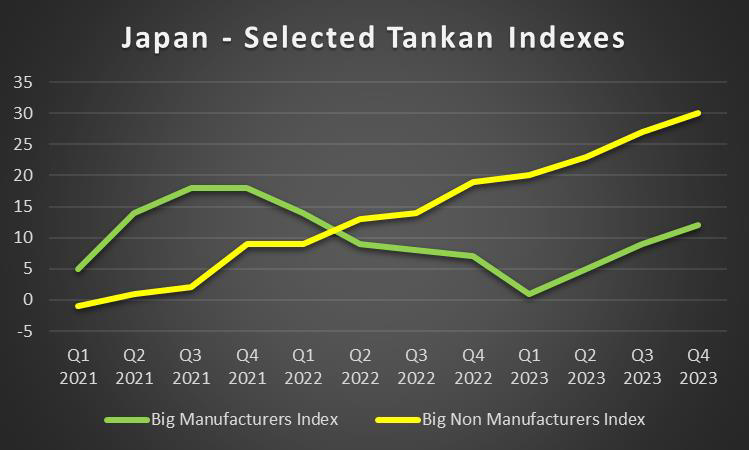

JPY is about to end the week relatively unchanged against the dollar, the pound and the EUR. The main event of the week for the Yen was the JPY nearing its historic 34-year low against the dollar. Thus the Yen may have been predominantly guided by fundamentals this week rather than macroeconomic data. In particular, the weakening of JPY prompted Japan’s Finance Minister Suzuki to warn the markets that Japanese authorities would take “decisive steps”. It should be noted that the Japanese government used the same wording before a market intervention in the past, hence speculation of a possible imminent operation by the Japanese government to save the Yen is on the rise. On the flip side BoJ board member Tamura highlighted the need for a steady yet slow monetary policy normalization while BoJ Governor Ueda was reported stating that BoJ must continue to support the Japanese economy with easy policy. The comments of the two BoJ policymakers were a painful reminder that the bank may keep a rather loose monetary policy for a longer period and in turn that seems to weigh on JPY. Moreover, the release of BoJ’s summary of opinions for the March meeting tended to verify comments expressed by BoJ policymakers for a slow and long road toward monetary policy normalization. The release had little effect on the JPY and on a fundamental basis the warning issued by Japan’s finance minister, as mentioned above, seems to keep the JPY in check, preventing it from further devaluation, at least against the USD. In our opinion, a potential intervention could occur on Monday, in which the JPY could meet the lowest amount of resistance by FX traders, given the upcoming long weekend due to the easter holidays and thus could be the most optimal time for the Government to intervene. In the coming week, we will keep an eye out for the release of Japan’s Tankan big manufacturing and non-manufacturing figures for Q1 .

EUR – Preliminary HICP rate next week

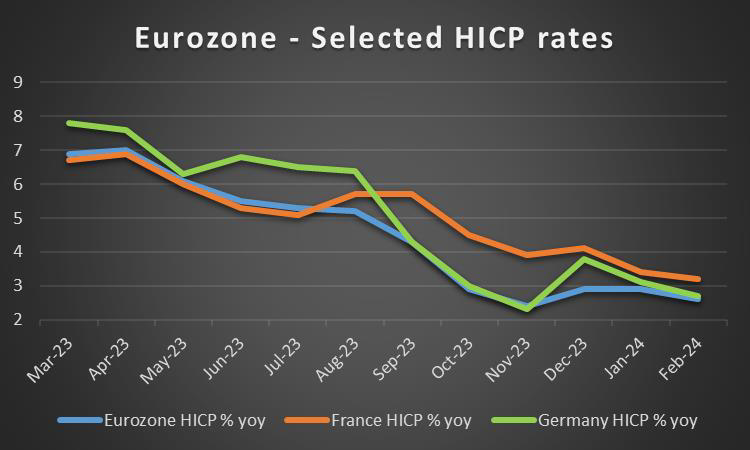

The common currency seems about to end the week unchanged against the USD, and JPY yet weaker against the pound. On a monetary level, we note the comments of ECB Chief Economist Lane on Monday that the bank “is increasingly confident that wage growth is slowly back toward more normal levels, potentially opening the door to rate cuts”. Furthermore, ECB’s Lane also stated that he was confident that inflation was on track when referring to the bank’s 2% inflation target, which may have weighed on the EUR. On a macroeconomic level, Germany’s consumer sentiment figure for April came in better than expected, which may have alleviated some downward pressures on the EUR, yet that appears to have only been a temporary relief as Germany’s retail sales rate for February came in much lower than expected, once again highlighting the status of Germany’s economy as the sick man of Europe. Looking at next week’s financial releases, EUR traders may be interested in the release Eurozone’s preliminary HICP rate for March which is expected to come in at 2.5%. Should the rate come in as expected or even lower, it would indicate easing inflationary pressures in the euro area, thus potentially opening the door for rate cuts by the ECB as was highlighted by ECB Lane, which in turn could weigh on the common currency. On the other hand, should the preliminary HICP rate come in higher than expected, thus implying persistent inflationary pressures it could provide support for the EUR. Lastly, EUR traders may also be interested in the release of the Eurozone’s final composite PMI figure for March and Germany’s industrial orders rate for February, yet we believe these to be secondary releases and would place a greater emphasis on the release of the Eurozone’s preliminary HICP rates for March.

AUD – RBA March meeting minutes due next week

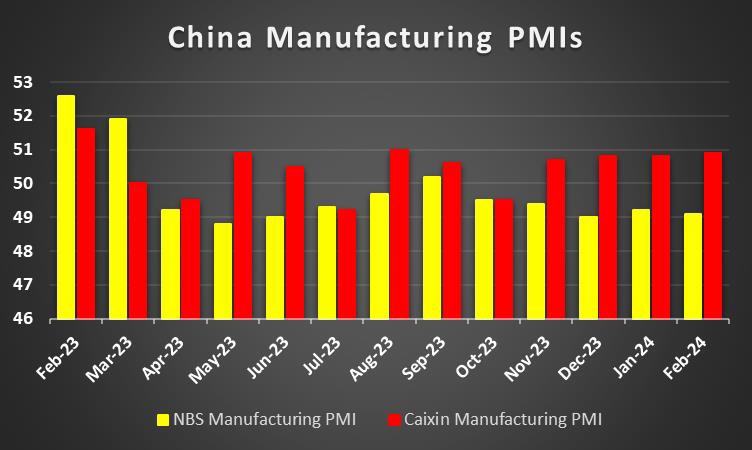

AUD is about to end the week relatively unchanged against the USD. On a fundamental level, we revert to our reference of Australia’s reliance on China as a major trading partner, and as such we delve slightly into recent developments in China. In particular, it appears that China is increasingly attempting to thaw relations with the US in order to boost China’s domestic economy as Chinese President Xi as per CNBC, told US CEOs that “bilateral relations can have a brighter future”. Thus, the economic link to Australia, is that should China’s economic conditions improve via the thawing of relations with the US, it could lead to increased demand for raw materials stemming from Australia and thus could be seen as a positive for the Aussie. However, such an event may not be immediately reflected in the FX markets. On a macroeconomic level though, the picture changes at least for the Australian inflation situation, as February’s CPI rate came in lower than expected at 3.40% yoy, implying that the RBA’s restrictive monetary policy appears to be bearing some fruit. However, when we look at the bigger picture, the past three CPI rates have remained the same, implying that inflationary pressures appear to be entrenched in the Australian economy. Therefore, the CPI rates could act as a double-edged sword for the RBA, where on the one hand it may harden the stance of RBA of maintaining its restrictive monetary policy, while on the other hand, it could allow them to ease their restrictive stance, as keeping rates too high for too long may strangle the economy. A scenario potentially being seen in the retail sector, where the preliminary retail sales rate for February came in lower than expected, implying a reduction in activity from the consumer’s side. Nonetheless, Aussie traders may be interested in the release of the RBA’s March meeting minutes which is due to be released next Tuesday, as an attempt to gain insight into the bank’s inner deliberations, which could determine the bank’s next direction and by affiliation the Aussie’s direction as well. On another note, China’s NBS Manufacturing PMI figure for March is due to be released over the weekend and is expected to improve to 49.9 from 49.1 prior, moreover painting a positive picture for the Chinese economy could be China’s Caixin Manufacturing PMI figure which is expected to come in once again at 50.9 implying an expansion in manufacturing activity in China. Therefore, given the close economic ties between China and Australia, an improvement in China could also benefit Australia and hence may aid the Aussie. Any negative divergence however, could have bearish implications for the Aussie.

CAD – Canada’s Employment data the next big test

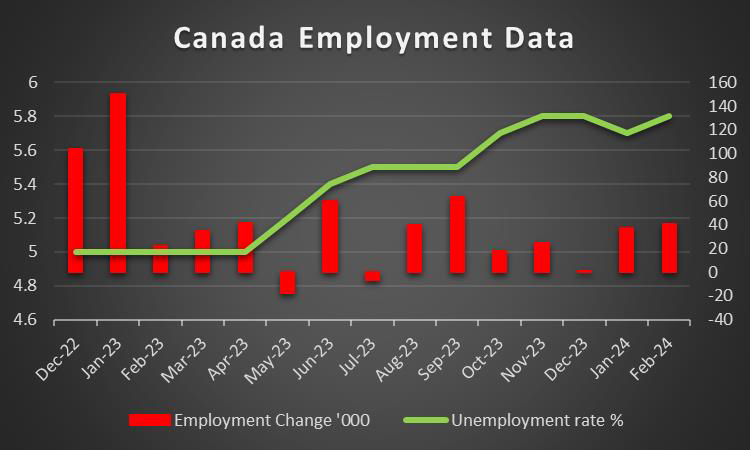

The CAD is about to end the week stronger against the USD. On a monetary level, we note the speech by BoC Deputy Governor Rogers who on Tuesday, implied that the current interest rate environment could be hindering investments into the Canadian economy. As such the hindering of potential economic activity due to restrictive monetary policy, could influence the bank’s stance to potentially adopt a more dovish tone which in turn could weigh on the Loonie. On a macroeconomic level, the clue about Canada’s economic outlook, seems to have been optimistic, with Canada’s GDP rate for January coming in better than expected, which could support the Loonie. On a deeper fundamental level, we note the positive correlation of the CAD with oil prices. Oil prices for the current week seem to have moved higher, which in turn may have also aided the Loonie given its status as an oil-producing nation. For next week we note Canada’s trade balance figure for February, yet the highlight for Loonie traders could be Canada’s employment data for March, where should a loosening labour market picture emerge, it could weigh on the Loonie and vice versa.

General Comment

Overall we expect volatility in the FX market to intensify given the increase of high-impact financial releases next week. We may see the USD regaining some of the initiative in the FX market to other currencies. As for US stock markets, we note that equities bulls appear to be in the driver’s seat for the Dow Jones 30 and S&P500 whilst appear to be facing difficulties in the NASDAQ. At the same time, we note the problems faced by Apple, Microsoft and Google in Europe over alleged violations of the Digital Markets Act, an issue which could weigh on each company’s respective stock price. Moving now to the gold market, gold’s price rallied once again breaking its prior all-time high figure of $2222. Gold’s price may have benefited from the relative inactivity of the USD. In addition to that also the continued decline of some US yields may have allowed gold’s price to rise. We expect in the coming week the negative correlation between gold and the USD to be on display, hence should the USD gain traction we may see some bearish tendencies developing for gold’s price. Ending it all we note that today and on Monday it’s to be a public holiday and the markets are to be closed in the US, Canada, UK, Germany, Switzerland, Norway, France, Sweden, Australia, Czech Republic, New Zealand, so some thin trading conditions may apply. Traders who opt to operate in these days should keep their guard up for any unexpected market reactions.