The week is nearing its end and we open a the calendar to see what next week has in store for the markets. On Monday we get New Zealand’s electronic card retail sales for June, Japan’s May machinery orders, China’s trade data for June and Sweden’s CPI rates for the same month. On Tuesday, we get China’s urban investment, indusrial output and retail sales growth rates for June, GDP rate for Q2, Germany’s ZEW indicators for July as well as the US and Canadian CPI rates for June, while on a monetary level, we note that BoE Governor Bailey is scheduled to speak. On Wednesday, we get Japan’s chain store sales, UK’s CPI rates, as well as the US PPI rates and industrial output, all being for June. On Thursday we get Japan’s trade data for June, Australia’s employment data for June, UK’s employment data for May, Euro Zone’s final HICP rates for June, the US Philly Fed Business index for July and the US retail sales for June. Finally on Friday we note the release of Japan’s CPI rates for June and from the US the preliminary Univeristy of Michigan consumer sentiment for July.

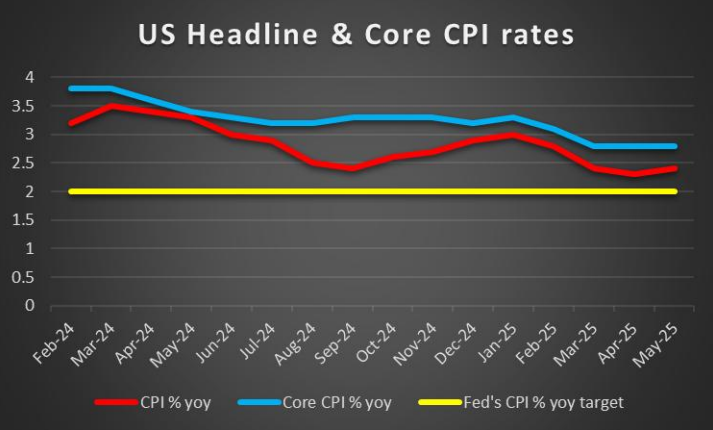

USD – US CPI rates next week

On a monetary level, we note that the Fed’s last meeting minutes which were released this week. The minutes showcase a willingness by Fed policymakers to cut rates this year and even possibly in their next meeting. In particular, it was stated that “A couple of participants noted that, if the data evolve in line with their expectations, they would be open to considering a reduction in the target range for the policy rate as soon as at the next meeting” which in itself is dovish in nature as it show’s that policymakers are considering the resumption of the Fed’s rate cutting cycle. Yet it should be said that other participants saw the case for no rate cuts this year.

On a macroeconomic level, we note that the economic calendar for the US was light this week. Yet next week, interest in the dollar may pick up with the release of the US CPI rates for June on Tuesday. Should the CPI rates showcase easing inflationary pressures in the US economy, it may aggravate the dovish sentiment which we discussed in our above paragraph and could thus weigh on the dollar. However, should they showcase a resiliency or even an acceleration of inflationary pressures, the pendulum may swing in favour of the hawk’s and could thus aid the dollar.

On a fundamental level, we highlight and stress that the tariff deadline has been pushed to the 1st of August per President Trump. Yet during the week we saw a new barrage of tariffs being thrown around against various nations, showcasing how dynamic the situation still is. Overall, depending on how the tariff rhetoric develops for the rest of the month it may influence the US Equities markets as well as the US dollar.

Analyst’s opinion (USD)

The Fed’s minutes in our view were predominantly dovish in nature, a view which we expressed in last week’s ‘Week Ahead’ report. Moreover, we note that a source of concern for policymakers are still the ongoing trade deals and the possible inflationary impact on the US economy. Yet with the deadline being pushed to the 1st of August, we see the case being made that some normality has returned to the markets. Yet with President Trump, nothing is certain and thus the narrative could change in the coming week. In particular, the US’s 10% possible tariff on BRIC’s nations may risk the fragile trade truce agreement the US struck with China should China perceived the US’s actions as hostile towards their economic interests.

GBP – Employment and Inflation data ahead

We make a start by noting on a monetary level that the BoE per Sky stated in it’s biannual health check of the UK’s financial system that “The outlook for UK growth over the coming year is a little weaker and more uncertain” as a result of President Trump’s tariffs amongst other reasons. In turn concerns about the health of the UK financial system could lead the bank of a more ‘dovish’ path, which in turn may weigh on the sterling.

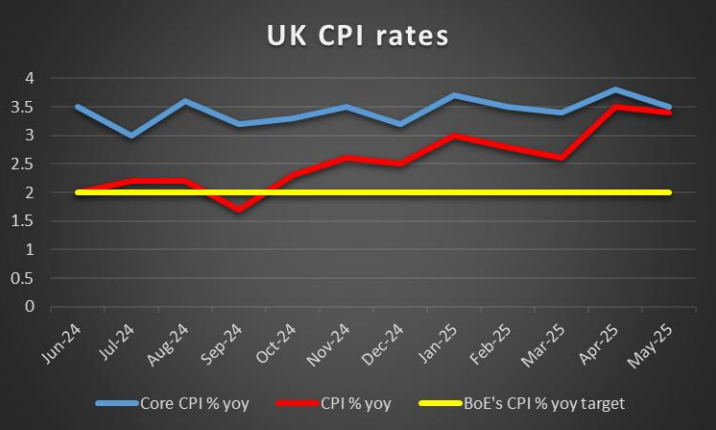

On a macroeconomic level, we note that next week, trader’s may be interested in the release of the UK’s CPI rates for June on Wednesday, where a hotter than expected inflation print could increase pressure on the bank to withhold from cutting rates in their next meeting and could in turn aid the sterling and vice versa. Moreover, the UK’s employment data for June as well is set to be released on Thursday, adding a continued interest for the pound towards the end of the week. A resilient labour market could provide some leeway for the bank to remain on hold, whereas a loosening labour market could increase calls for further rate cuts.

On a fundamental level, we note the recent collaboration between the UK and France for nuclear weapons. According to a report by the FT “The UK and France have pledged for the first time to co-ordinate the use of their nuclear weapons, saying they would jointly respond to protect Europe from any extreme threat.” A more friendlier relation between the UK and it’s European neighbours could possibly aid the UK Equities markets down the line.

Analyst’s opinion (GBP)

Interest may pick up in the Sterling in the coming week, given the release of the nation’s CPI rates and unemployment data. In our view the CPI rates are crucial and could allow the bank to continue on their rate cutting cycle, which may weigh on the pound. Yet, the employment data is also crucial for the UK therefore we would not be surprised to see heightened volatility in the cable in the coming week

JPY – Inflation data ahead

On a monetary level, we note BOJ board member Koeda stated that “inappropriate to say now specific timing of next rate hike due to high uncertainty over the economic outlook”. Although it showcases uncertainty as to when the next rate hike will occur, it does imply that there may be a next rate hike which could be perceived as slightly hawkish in nature. In turn should further BOJ policymakers in the coming week hint that a rate hike may be in the cards for the bank in the near future it could aid the JPY

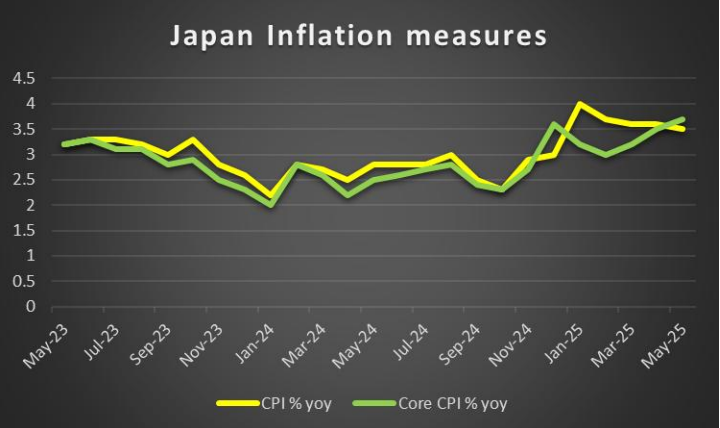

On a macroeconomic level, we note that Japan’s nationwide CPI for June is set to be released next Friday. Should the CPI rates showcase an acceleration of inflationary pressures in the US economy it could aid the JPY, whereas easing inflationary pressures in the Japanese economy may have the opposite effect and weigh on the currency.

On a fundamental level we noted last week that a US trade deal with Japan before the 9th of July deadline may not occur which we correctly noted in last weeks report. Yet with the deadline pushed to the 1st of August there is still some hope for Japan to reach an agreement. The reason as to why we say “hope” is because Japan now faces a 25% tariff as stated by President Trump earlier on this week. Thus should the following round of negotiations fail to bear fruit it may negative influence the Japanese equities markets.

Analyst’s opinion (JPY)

In our view next week’s inflation print may be of interest by the BOJ, yet the bank may be more interested in seeing as to how the trade negotiations with the US play out as it may be a source of great uncertainty for the bank. Therefore we wouldn’t be surprised to see hints for possible rate hikes in the future but not before a trade agreement has been reached with the US

EUR – Germany’s ZEW figures due out next week

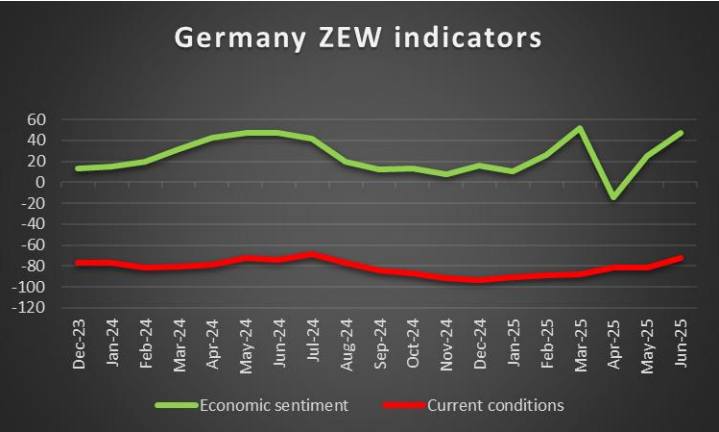

On a macro level we note that Germany’s ZEW figures for July are set to be released next Tuesday. Given Germany’s significance as one of the largest economies in the Zone, the financial releases composed of the economic sentiment and current conditions in Germany may influence the EUR. Thus should the figures showcase an improvement from last month it may be perceived as a positive and could in turn aid the EUR. Whereas should the figures showcase a deterioration if may weigh on the common currency

On a monetary level, we note the comments made by ECB member Nagel who per Bloomberg stated that “Yet it would be unwise to commit to a certain interest-rate path, to envisage a further step or indeed, to rule it out” implying that the current situation is still uncertain, yet the overall tone could be perceived as a hesitation for the bank to commit to any particular path. Nonetheless, in our opinion the comments made by ECB Nagel could be interpreted as slightly hawkish in nature. Overall, should further ECB policymakers showcase a hesitancy to cut rates in the near future, it may aid the EUR.

On a fundamental level we note that the EU is amongst the other US trading partners who are still attempting to reach a trade agreement. President Trump this week stated that he would “probably” tell the EU what rate to expect for its exports to the US. However with President Trump stating that the bloc was much more cooperative and thus the EU may be able to a strike a relatively decent deal with the US which could aid the European Equities markets

Analyst’s opinion (EUR)

In our view, although the ZEW figures are important, the ongoing trade negotiations with the US may take the market’s attention in the coming week, especially considering that the recent tariff announcements by President Trump have led to a resurgence of market speculation as to what may come next.

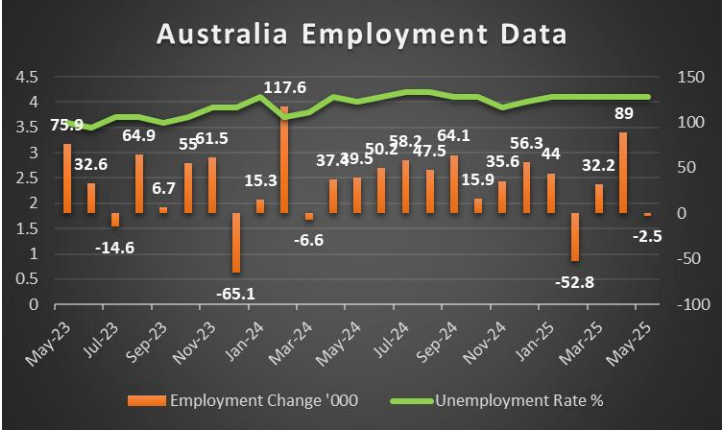

AUD – RBA surprisingly remains on hold

On a macro level, we note for next week Australia’s employment data for June which is set to be released next Thursday. Should the nation’s employment data showcase a loosening labour market, it could weigh on the Aussie. Whereas should the employment data showcase a resilient labour market it could potentially aid the Aussie. Moreover, of interest may be the unemployment rate which currently stands at 4.1% and thus it’s release may have a greater impact on the Aussie over the employment change figure.

On a monetary level, we note that the RBA’s interest rate decision occurred this week and last week AUD OIS had implied an 84.6% probability for the bank to cut rates by 25 basis points. However, that was not the case as the bank took the markets by surprise by remaining on hold. Moreover in the bank’s accompanying statement it was stated that “Nevertheless it remains cautious about the outlook, particularly given the heightened level of uncertainty about both aggregate demand and supply”, potentially as a result of the uncertainty about the world economy which has emerged due to the US tariffs and policy responses from other countries. Thus, should the tariff bonanza lead to heightened uncertainty once again it may lead to a more restrictive stance by RBA policymakers whereas should trade deals be signed, it could ease the worries presented by RBA policymakers which in turn could pave the way forward for the bank to continue cutting rates

On a fundamental level, we highlight China’s GDP rate for Q2 on Tuesday which is expected by economists to come in at 5.2% which would be lower than the rate of 5.4% of Q1. In turn such a scenario could weigh on the AUD as well give their close economic ties.

Analyst’s opinion (AUD)

The RBA’s decision to remain on hold took the markets by surprise, yet considering how we are still discussing new tariffs which are being imposed and a new deadline of the 1st of August, can we really be that surprised that the bank decided to remain on hold?. Nonetheless, attention may be on the release of Australia’s employment data next week

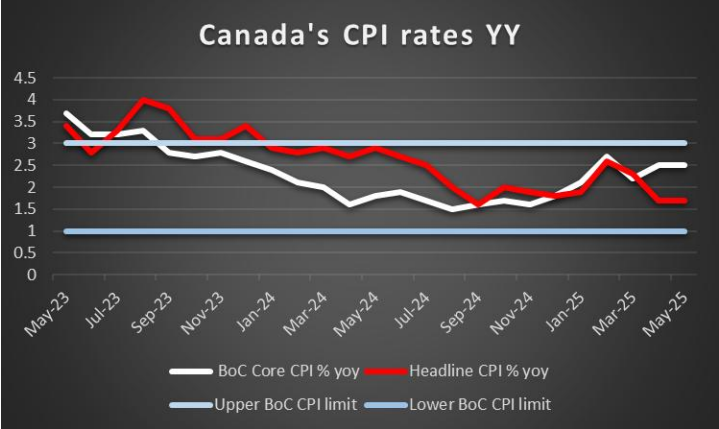

CAD – Inflation data ahead for Loonie traders

On a macroeconomic level, we note that Canada’s CPI rates for June are set to be release next Tuesday. Market participants may be interested in the afformentioned financial release for obvious reasons as it may showcase the state of inflation in the Canadian economy. Therefore, should the inflation print showcase easing inflationary pressures in the Canadian economy it could potentially weigh on the Loonie and vice versa.

On a fundamental level, some reports have emerged that OPEC may be considering, pausing their output hikes after their next increase. In turn a restriction of the supply of oil into the market could aid oil prices and thus could also aid the CAD given Canada’s status as an oil exporting nation.

Analyst’s opinion (CAD)

Canada’s CPI rates will surely be interesting, yet any announcements by OPEC+ in regards to the supply of oil into the market could lead to a secondary impact on the Loonie next week. Nonetheless, our sights are turned to the release of the CPI rates and whether they will showcase an acceleration or easing inflationary pressures in the economy

General Comment

As a closing comment we note that the risk which may arise from Trump’s tariff extension to the 1st of August may continue to tantalize the markets for the rest of the month. Moreover, the situation still remains volatility and may warrant closer attention.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.