A slow week is coming to an end and we open a window to what next week has in store for the markets. On the monetary front, a number of policymakers from various central banks are scheduled to make statements and could sway the markets. As for financial releases, after a quiet Monday, on Tuesday we note the release of Japan’s Corporate Goods Prices for January, UK’s employment data for December, Switzerland’s January CPI rates, Germany’s ZEW indicators for February and highlight the release of the US CPI rates for January. On Wednesday we get UK’s CPI rates for January and Eurozone’s revised GDP rate for Q4. On Thursday we start with Japan’s GDP rates for Q4, Australia’s January employment data, UK’s preliminary GDP rate for Q4, the Czech Republic’s CPI rates for January, Canada’s House Starts for the same month and manufacturing sales for December and from the US we get the weekly initial jobless claims figure, the Philly Fed business index for February as well as January’s retail sales and industrial production growth rates. On Friday we get UK’s retail sales growth rate for January, the US PPI rates for the same month and finally the preliminary US University of Michigan consumer sentiment for February.

USD – US CPI rates ahead

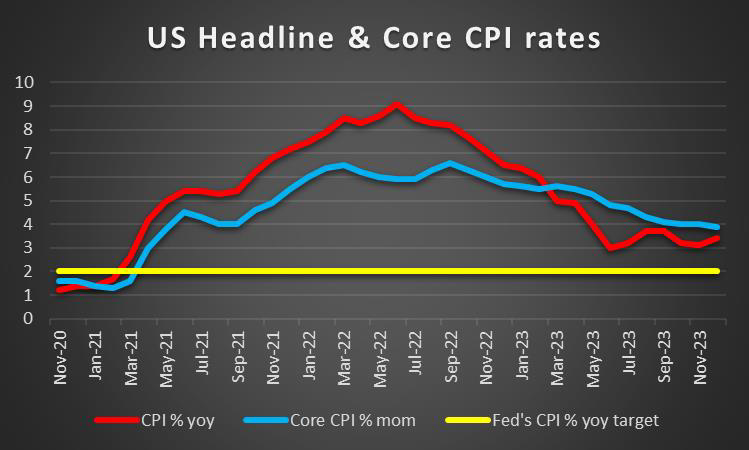

The USD is about to end the week relatively unchanged against its counterparts. On a fundamental level, we tend to maintain our worries for the banking sector, with the incident involving New York Community Bank forcing us to concentrate on medium-sized companies fo the sector. We are also concerned about a possible contagion across the sector, yet also abroad. The issue is highlighted given the wide exposure of US consumers to credit card debts, but also the tight financial environment in the US economy. Nevertheless, the market seems to stay calm for now. On a monetary level, once again we note that comments of Fed policymakers tend to underscore the possibility that the Fed is to maintain high rates for a longer period than what the market is currently pricing in. It’s characteristic that Fed Board governor Kugler stated that rate cuts would be appropriate “at some point…assuming inflation and the labor market continued to cool”. It’s interesting how Ms. Kugler placed similar weight on inflation and the labor market, which is understandable given the Fed’s dual mandate. Yet the statement implied that rates may remain at their current levels for longer. Please note that the market has already partially shifted its expectations from 6 rate cuts for 2024, starting in March to five rate cuts in the year, starting in May. Should market sentiment continue to be contradicted, we may see the market being forced to reposition itself further and that may keep USD supported on a monetary level. On a macroeconomic level, we note the tighter-than-expected employment market as reported by the US employment report for the past month, last Friday with the rise of the NFP figure taking the markets by surprise. The release provides more leeway for the Fed to maintain rates high for longer. Also, the higher-than-expected ISM non-manufacturing PMI reading for January, implying a wider expansion of economic activity in the sector tended to underscore the narrative for a soft landing of the US economy. In the coming week, we highlight the release of the US CPI rates for January and should the rates continue to slow down, we may see the USD losing ground as it may intensify market expectations for an earlier rate cut by the Fed.

GBP – GDP and CPI rates eyed

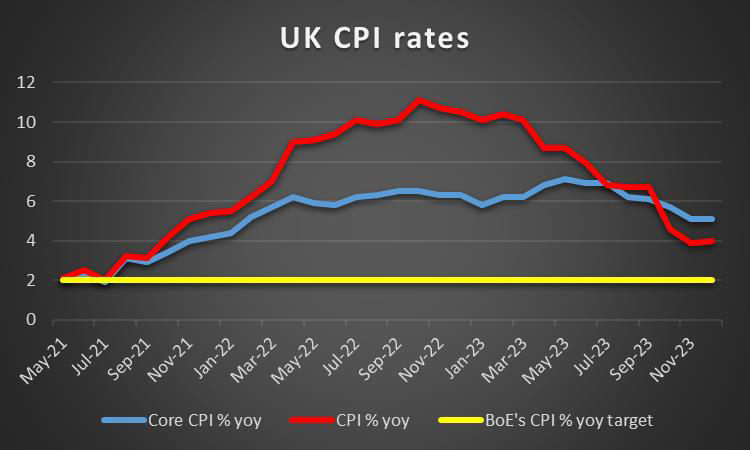

The pound is about to end the week relatively unchanged against the USD and the EUR, yet seems to be gaining against the JPY. On a fundamental level, we still note the cost of living crisis which tends to lower the living standards in the UK as possibly the main issue. Yet the Government seems to be confident that inflation is going to come down yet does not seem to be gaining the public’s trust. It’s characteristic how a British think tank as reported by Reuters, stated that UK living standards will start improving before the year’s end, yet lower-income households will have to wait until 2027 to recover their pre-pandemic spending power. Yet on a monetary level, we do not see any signs of a possible easing of the tight financial conditions in the UK economy yet. The bank’s stance, as expressed in its latest interest rate decision was underscored by BoE’s chief economist Huw Pill on Monday. Mr. Pill highlighted that the question is not whether there will be rate cuts but when. Mr. Pill also pointed toward the need for additional signs that underlying drivers of inflation, like wages and pricing in the services sector start slowing before starting cutting rates. That tends to highlight the release of the UK CPI rates for January next week. We expect the rates to slow down which in turn may weaken the pound as the pressure on BoE to start cutting earlier may rise. Yet it’s not only about inflation, there are worries for the economic outlook of the UK also on growth level. In the coming week, we are also getting the preliminary GDP rates for Q4 and another contraction on a quarter-on-quarter level, which would technically be signaling the entering of the UK economy into a recession and could weaken the pound. Furthermore, we also note the release of the UK employment data and highlight beyond the unemployment rate and employment change figure also the average earnings growth rate, given the statement of BoE’s Pill mentioned earlier. On a more positive note, we underscore the acceleration of the Halifax House Prices for January, implying a wider demand for housing in the UK economy.

JPY – GDP rates in the epicenter of attention

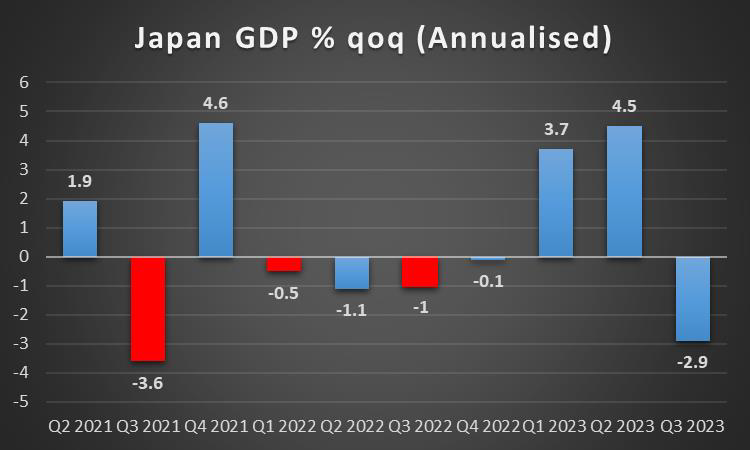

JPY seems about to end the week slightly lower against the USD, EUR and GBP, in a sign of wider weakness. On a fundamental level, we note the governing LDP’s internal funds scandal probe which may weigh further on the popularity of the Japanese Government. Yet we view as the main issue for the JPY on a fundamental level, its dual nature as a safe haven and a national currency. Hence, a possible improvement of the market sentiment in the coming week may weaken JPY, while a more cautious approach of the market may provide safe haven inflows for the JPY. On a monetary level, we note that BoJ seems to be growing more confident that it will be exiting its ultra-loose monetary policy. Bank’s policymakers in the summary of opinions of the January meeting seem to expect an intensification of inflationary pressures in the services sector, “supported by wage increases resulting from this year’s annual spring labor-management wage negotiations” which could stabilise inflation at around 2%, a scenario that would allow the bank to proceed with interest rate hikes. Yet any change is expected to be kind of subtle, as implied by BoJ policymaker Uchida in statements made on Thursday. Overall neither the aforementioned document nor the statements Mr. Uchida made seemed to provide some substantial support for the JPY, yet should the bank continue signaling a return to a normalisation of monetary policy we may see JPY getting some support as it would reinforce market expectations for a rate hike in June. On a macroeconomic level, we note the better-than-expected services and composite PMI figures for January, implying a faster expansion of economic activity for the sectors which improves the outlook for the Japanese economy despite its manufacturing orientation. On the negative side, we note the substantial narrowing of the current account balance in December tended to weigh macroeconomically. In the coming week, we note the release of the revised GDP rate for Q4. The rate is expected to show an improvement if compared to the preliminary release and if actually so could support the JPY, as it would reverse the picture of a contraction of the Japanese economy for the last quarter of the past year.

EUR – Major European cities under siege

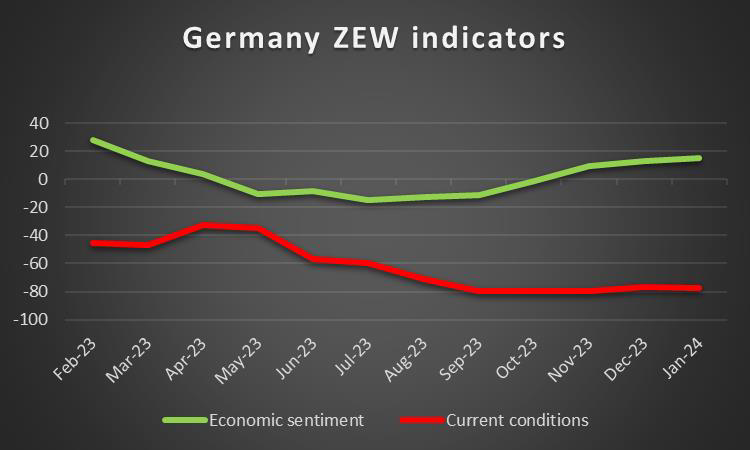

The common currency seems about to end the week unchanged against the USD and the pound and is edging higher against the JPY. On a fundamental level, we note the ongoing protests of European farmers with major European cities being “under siege” by tractors. Increased costs and cheap imports from Ukraine seem to be the main issues. We also note that the protests may influence the public’s opinion before the European Parliament elections in three months. We still expect the issue to escalate further before actually being resolved and could start weighing on the common currency in the coming week on a fundamental level. On a monetary level, we note that ECB seems to be expecting inflation to come down earlier than initially expected, at least according to their AI model. On the other hand, ECB’s chief strategist Lane seems to be placing substantial weight on how wages will be behaving over the next few months and their effect on inflation, which may delay any interest rate cuts a bit. Furthermore, ECB’s Wunsch was even more conservative stating that there is value in waiting for more comforting data regarding inflation. Please note that the market currently prices in a double rate cut in the June meeting and proceed with another three rate cuts within the year. Hence, should the bank continue sending out signals that it will delay any rate cuts, we may see the EUR getting some support, yet we tend to see the ECB as the primary candidate to start cutting rates first among central banks of developed economies, given that inflation seems to be nearing the bank’s target. On a macroeconomic level, Eurozone’s outlook seems to be improving according to February’s Sentix index which is kind of encouraging. On the other hand, the demand side of Eurozone’s economy seems to be weakening given the wider contraction of the retail sales rate for December which tends to weigh on the outlook of Eurozone’s economy. We would also note the conflicting messages for Germany’s manufacturing sector which are a bit worrying. In the coming week, we highlight the release of Germany’s ZEW indicators for February and Eurozone’s revised GDP rates for Q4.

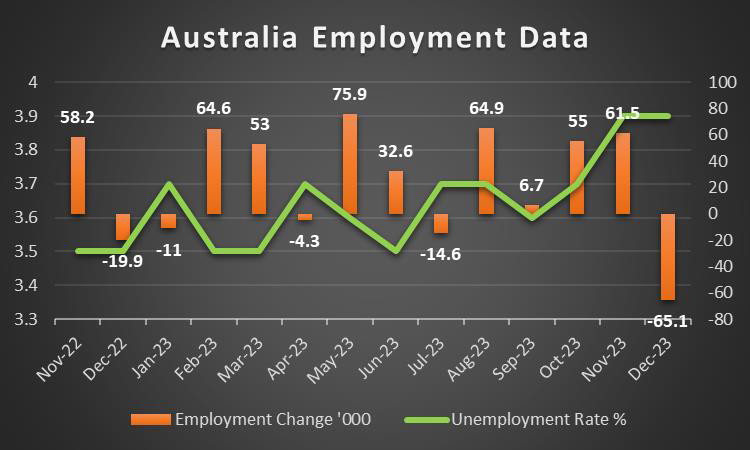

AUD – Employment data in focus

AUD is about to end the week lower against the USD for a sixth week in a row. On a monetary level, we note that RBA remained on hold as was widely expected, yet the bank has reiterated its concerns that inflationary pressures still remain high in the economy. In particular, the bank stated in its accompanying statement that “a further increase in interest rates cannot be ruled out”, implying that the bank may increase its interest rates in the future, which could maintain the Aussie supported on a monetary level. On a more

fundamental level for the Aussie, we note worries for the Chinese economy, given the close economic ties of Australia with China. The deflationary pressures on a consumer level in China, tend to highlight the difficulties in the recovery of the Chinese economy. Also worrying for Australian exporters of raw material to China, are the even wider deflationary pressures on a producer level, making the bargaining of Australia’s raw materials selling price even harder. Also on a deeper fundamental level, we note the effect of the market sentiment on the Aussie. AUD is considered as a riskier investment asset as it is viewed as a commodity currency, hence a possible improvement in the market sentiment could provide some support for the Aussie and vice versa. On a macroeconomic level, we note the release of Australia’s employment data for January as the highlight of next week for Aussie traders. The release gets additional interest as the RBA in Tuesday’s interest rate decision, mentioned the importance of the labour market as a factor in its future interest rate decisions. Should the data show the tightness of the Australian employment market easing further, we may see the Aussie slipping as it may also add more pressure on RBA to start cutting rates earlier.

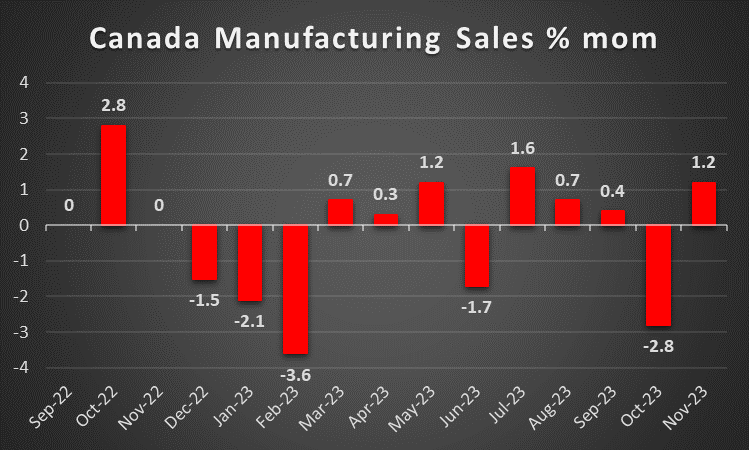

CAD – Fundamentals to lead the Looney

The CAD is about to end the week relatively unchanged against the USD, yet Canada’s employment data are still to be released and could change the picture. On a monetary level, we note that the Bank’s January meeting deliberations the bank seems to have hesitations about easing its monetary policy, given the uncertainty for the outlook of inflation. It was recognised that the bank’s tight monetary policy seems to be bringing some results in easing inflationary pressures in the Canadian economy, yet inflation seems to be coming down slowly. It’s characteristic of the bank’s stance, that BoC Governor Macklem stated that more time is required for an easing of inflationary pressures and tended to highlight the role of high shelter prices in that aspect. Overall any further signs that the bank intends to delay any rate cuts may keep the Looney supported in the coming week. On a fundamental level, we note the path of oil prices, given the positive correlation of oil with the Looney. Oil prices seem to have been on the rise, since the start of the week. It seems that oil prices are getting some support, despite the slack in the US oil market and the doubts about Chinese oil demand, as the tensions in the Middle East tend to intensify market worries for the supply side of the commodity. Should oil prices continue rising in the coming week, we may see some support building up for the Looney as well. Also given the commodity currency nature of the Looney a possible improvement of the market sentiment, especially on the Southern side of the Canadian border, we may see the CAD getting some support. On a macroeconomic level, we note the reversal of Canada’s November trade surplus into a deficit in December, yet in the coming week given the lack of high-impact financial releases, we expect fundamentals to lead the way for the Looney.

General Comment

As general comment for the coming week, we expect volatility to rise, possibly with the USD increasing its influence in the FX market, given the gravity and frequency of high impact US financial releases. As for US stockmarkets we highlight that the earnings season may have kept equity bulls afloat in the past few days, yet on the other hand comments of Fed policymakers contradicting market expectations for extensive rate cuts tend to weigh on US stock markets. In the coming week, we note the earnings releases of Airbnb (#ABNB), American International Group (#AIG), Coca-Cola (#KO), Lyft (#LYFT) on Tuesday, on Wednesday Cisco Systems (#CSCO), on Thursday Coinbase (#COIN), Dropbox (#Dropbox) and on Friday Baidu Inc (#BIDU).

As for gold, we note the relative stabilization of its price, taking advantage of the USD’s inactivity, which tends to be in line with the negative correlation of the two trading instruments. Furthermore, we note that the drop in US yields at the beginning of the week, they recovered, and are about to end the week near the same levels they began. Should US yields continue to rise in the coming week we may see gold’s price slipping as market attention may shift increasingly towards the US Bond market. On the other hand, should we see the USD slipping in the coming week, we may see gold’s price getting some support.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.