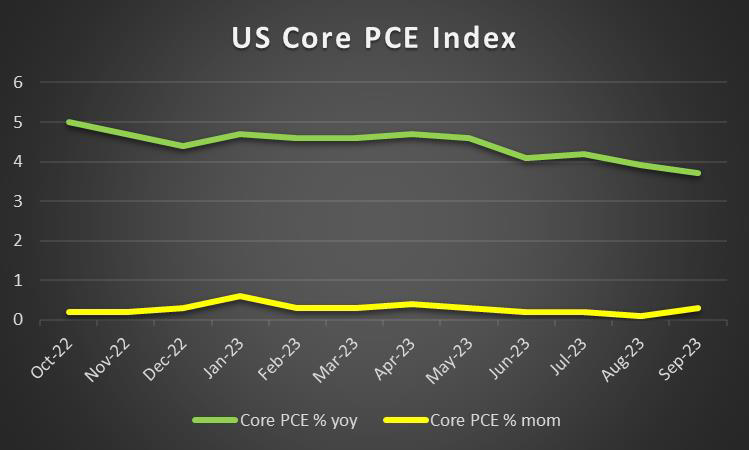

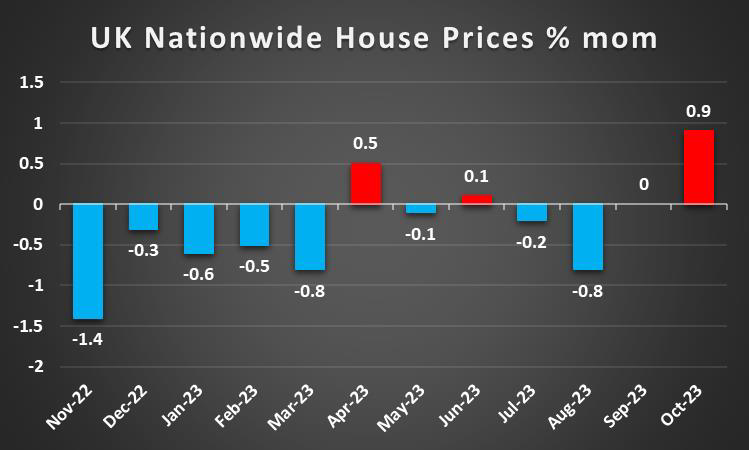

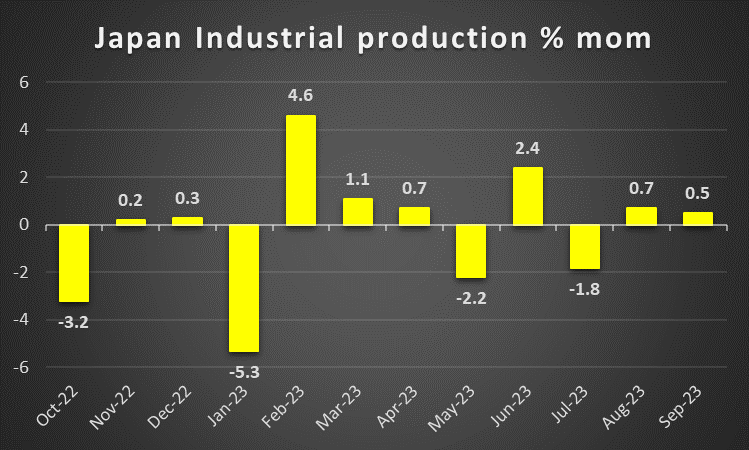

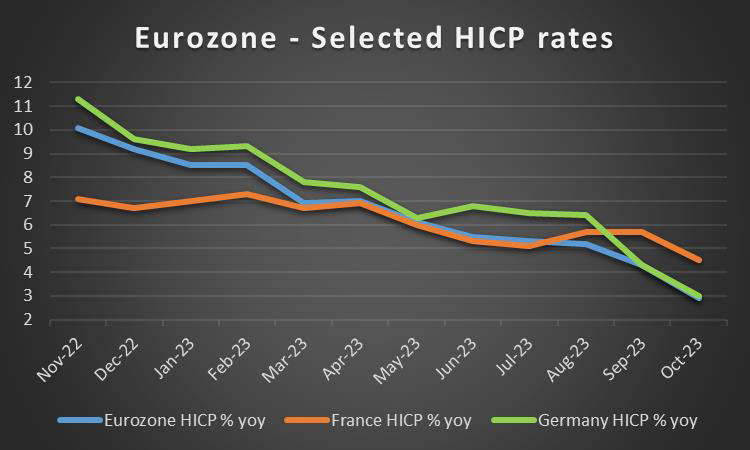

As the week draws to a close, we open a window to what next week has in store for the markets. On the monetary front, we note that New Zealand’s RBNZ on Wednesday, is to release its interest rate decision, while a number of policymakers from various central banks are scheduled to make statements throughout the week and could sway the market’s opinion. As for financial releases, we note on Tuesday the release of Australia’s October retail sales and from the US the consumer confidence for November. On Wednesday we get Germany’s preliminary HICP rate for November and we highlight the release of the revised US GDP rate for Q3. On Thursday we get Japan’s preliminary industrial output for October, Australia’s building approvals and CapEx rates for October and Q3 respectively, China’s NBS PMI figures for November, Turkey’s GDP for Q3, the UK’s Nationwide house prices for November, France’s final GDP rate for Q3 and preliminary HICP rates for November, Switzerland’s KOF indicator for November, Eurozone’s preliminary HICP rates for November, Canada’s Business Barometer for November and we highlight for Loonie traders the GDP rate for Q3, while from the US we get the Consumption rate and the Core PCE price index for October, as well as the weekly initial jobless claims figure. On Friday, we get China’s Caixin manufacturing PMI figure, Canada’s employment data and the US ISM manufacturing PMI figure all being for November.

USD – 2nd estimate of GDP rate in focus

The USD tended to remain relatively unchanged against its counterparts for the week, maybe with some slight bearish tendencies. On a monetary level, we note the release of the Fed’s October-November meeting. The document showed the bank’s intentions to continue leaning on the hawkish side maintaining a restrictive policy, yet a wide majority seems to favor the bank to remain on hold. On the one hand, Fed policymakers seem to want to avoid another rate hike, yet at the same time, the market’s expectations for a quicker rate cut in the coming year seem to be contradicted by the contents of the minutes. The message seems to have come at least partially across, as the markets now price in a possible rate cut in June instead of May, as was the case before. Also a number of Fed policymakers may reiterate the view that more indications may be necessary for them to be convinced that inflationary pressures in the US economy are subsiding and any such comments could provide some support for the USD and vice versa. On a macroeconomic level, we note the drop in the existing home sales figure marketing another possible contraction for the US real estate sector, while the durable goods orders growth rate contracted more than expected implying a lack of confidence on behalf of US businesses to actually invest in the US economy. On a more positive

note the weekly initial jobless claims figure dropped more than expected, implying some sort of tightness in the US employment market that supported the USD somewhat.

GBP – Fundamentals to lead the way

The pound is about to end the week higher against the USD, the EUR and JPY in a sign of broader strength. On a fundamental level, we note the UK finance minister Hunt’s Autumn Statement on Wednesday. The UK finance minister, recognising a possible slowdown of the economy, tended to highlight tax-cuts, which could characterise a potentially expansionary fiscal policy. Yet the finance minister also announced plans to reduce debt which may curtail expenditure somewhat. Overall, we tend to see the tone of the announcement as being supportive for the pound at a fiscal level. Further statements of UK government officials pointing towards an expansionary fiscal policy may add more support for the pound. On a monetary level, we note that BoE Governor Bailey warned the markets not to expect inflation to fall quickly and thus tended to dismiss any idea of an early rate cut by the bank. Hence should BoE policymakers continue leaning on the hawkish side, we may see the pound getting some support on a monetary level. On a macroeconomic level, we note that November’s trend for industrial orders indicator dropped deeper into the negatives, implying an expectation for a deterioration of economic activity in the sector. Yet what really caught the market’s eye in the past few days was the release of UK’s November preliminary PMI figures which tended to rise more than what the market expected, improving the economic outlook of the UK.

JPY – BoJ’s outlook a key factor for JPY

JPY is about to end the week relatively unchanged against the USD and the EUR but is losing ground against the pound. On a monetary level, we note that discussions among analysts for BoJ to end its negative rates monetary policy in 2024 have been enhanced in the past week. It should be noted that BoJ Governor Ueda, tended to note that a weak Yen does not have only a negative aspect, which may have sounded a bit dovish. Yet, overall we tend to see the market’s expectations being enhanced for the bank to proceed with its first rate hike being expected in Spring next year, although some analysts mention the January meeting as a possible pivot point for the bank. Overall any comments by BoJ policymakers supporting the idea of a policy normalisation may provide substantial support for JPY in the coming week. On a fundamental level, we note JPY’s dual nature as a safe haven and a national currency, with any possible tensions providing some support for the yen and a more risk on approach by the market may weaken it. On a macroeconomic level, the acceleration of Japan’s CPI rates for October as released during today’s Asian session tends to support the idea that BoJ should start normalising its monetary policy, as it implies a resilience of inflationary pressures in the Japanese economy and thus tends to support JPY. On the other hand, economic activity seems to weaken in the crucial manufacturing sector for November, according to the month’s preliminary PMI figures, which tends to intensify the worries for the outlook for the Japanese economy.

EUR – Preliminary November HICP rates to move EUR

The common currency is about to end the week at about the same levels as the week began against the USD and JPY, yet is losing ground against the GBP. On a political level, yesterday’s riots in Dublin and the recent Dutch elections highlighted the deep rift among Europeans about immigration once again an issue that is tantalizing the Eurozone on a political level. For the time being we expect no major market reaction on the issue. On a monetary level, we note that the minutes of ECB’s October meeting showed a hawkish predisposition of the bank’s policymakers, with some not being quite convinced that another rate hike is not necessary. Yet at the same time, it seems that worries of ECB policymakers about the economic outlook of the Eurozone were extensive. It’s characteristic that ECB Nagel hinted that the ECB is close to its terminal rate, implying that the bank may need to hike at least one more time, and as such his comments may be perceived as slightly hawkish. On the other hand, we note also France’s central Bank Governor Villeroy de Galhau who stated yesterday that the ECB is not to hike rates again should there be no surprises highlighting the power struggle within the bank. Furthermore, the minutes of the meeting tended to shed light also on the worries of the bank for the economic outlook of the Eurozone. Yet on a macroeconomic level, there seems to be a ray of hope, as the Eurozone’s November preliminary PMI figures, despite implying another contraction of economic activity the situation is slightly improving and the relevant indicators seem to be bottoming out. In the coming week, we note the release of France’s final GDP rate for Q3 and we highlight the release of November’s preliminary HICP rates for November and a possible failure of the rates slowing down could provide substantial support for the common currency.

AUD – CapEX, Building Approvals and Chinese PMI figures in sight

AUD is about to end the week higher against the USD for a second week in a row. On a monetarry level, we note RBA’s worries for inflationary pressures in the Australian economy. It’s characteristic that RBA Governor Michelle Bullock stated that “the remaining inflation challenge we are dealing with is increasingly homegrown and demand driven”. It’s as if the bank’s Governor is preparing the markets for another rate hike, or at least underscoring the bank’s hawkish tilt. For the time being the market seems to maintain the expectation for the bank to hike rates in early Spring next year. Overall should there be further signs of a hawkish stance on behalf of the bank, we may see AUD getting some support in the coming week. On a more fundamental level, given the perception of the market for AUD as a riskier asset given it being a commodity currency, a positive, more optimistic market view could provide some support for the Aussie and vice versa. At the same time, we highlight any developments in China’s economy, given the close Sino-Australian economic ties. According to various media outlets, China is preparing packages to aid its property developers, as fears continue to mount about the resilience of the Chinese economy. Such a move could potentially aid in economic development in China, which in turn may provide some support for the Aussie.

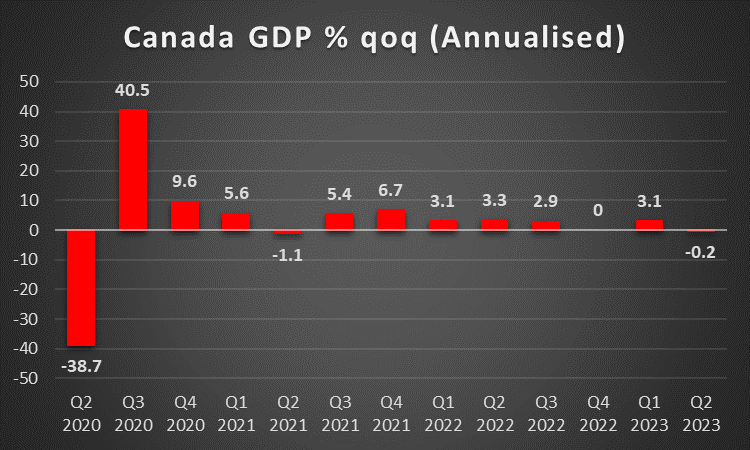

CAD – GDP and employment data to gain attention

The Loonie is about to end the week relatively stronger against the USD. On a monetary level, it seems that BoC’s hawkishness has eased somewhat and may have clipped any gains for the Loonie. It’s characteristic that BoC Governor Tiff Macklem implied that the bank may have reached its terminal rate and further rate hikes may not be needed by stating that “interest rates may now be restrictive enough to get us back to price stability”. The market seems to be in line with such a scenario and currently seems to expect that the bank may proceed with a rate cut in April. On a more fundamental level, we note that oil prices tended to edge a bit higher for the week, yet nothing material. Oil market fundamentals tend to be drawn between OPEC+’s intentions for lower production levels or not, a slack in the US oil market and doubts about worries for the demand outlook of the oil market particularly from China. Should oil prices strengthen in the coming week, could provide some support for the CAD given that Canada is a major oil-producing economy. Furthermore, a positive market sentiment in the coming week could support the CAD as a commodity currency. On a macroeconomic level, we note that after the slowdown of inflationary pressures in October, attention now turns to growth thus we note the release of the GDP rate for Q3 on Thursday and another contraction could weaken the Loonie. On Friday we get November’s employment data and should they show that the employment market remains tight we may see the CAD getting some support.

General Comment

In the coming week, we expect the FX market to remain rather balanced given the low number of high-impact financial releases stemming from the US. Yet we would like to make a comment about RBNZ’s interest rate decision on Wednesday. The bank is widely expected to remain on hold at 5.5% and the market is expected to have reached its terminal rate. Yet market analysts tend to highlight the possibility of extensive rate cuts in the coming year. Should the bank in its accompanying statement more or less maintain a cautious tone, foreshadowing an early cut in the official cash rate, we may see the Kiwi retreating. As for US equities markets, we note that the earnings release season is drawing it a close as most high-profile companies have released their earnings reports. Overall we expect the US equities markets to be driven by fundamentals and may focus also on the Fed’s intentions. As for gold, we note that the negative correlation between the precious metal and the greenback seems to be functioning as the USD’s slippage against its counterparts seems to be benefiting gold’s price. The slight drop of US yields may also have provided some support for gold’s price. Should in the coming week, the USD’s weakening be enhanced, we may see gold’s price rising.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.