Market worries of a recession have made a comeback this week and with the sentiment taking a turn for the worse, we take a look at what next week has in store for the markets. On the monetary front, we note a relatively quiet period regarding monetary policymakers, as the Fed enters its blackout period before its May meeting. On a more fundamental note, we note the release of the Riksbank’s, Turkey’s CBT and BOJ’s interest rate decisions on Wednesday, Thursday and Friday respectively. As for financial releases, we make a start on a quiet Monday with Germany’s Ifo indicators for April. On Tuesday, during the European session we note the UK’s CBI figures and during the American session the release of the US New Home sales and Consumer Confidence figures for March and April respectively. On Wednesday, during the Asian session, we make a start with New Zealand’s trade data for March, Australia’s CPI rates for Q1 and in the European session, we have Germany’s Gfk Consumer sentiment figure for May and the UK’s CBI Distributive Trades figure for April while during the American session, we have the US durable goods orders for March. On Thursday, we note a quiet Asian session, and we make a start during the European session with Sweden’s Preliminary GDP for Q1 followed by the Eurozone’s Business Climate, Economic Sentiment and Final Consumer confidence as well as Canada’s Business Barometer, all for the month of April. During the American session, we highlight the key release of the preliminary US GDP rate for Q1 and the weekly initial jobless claims. Lastly, on a very busy Friday, we begin during the Asian session with Japan’s Tokyo CPI print for April and Preliminary Industrial production rate for March, during the European session we have France’s, Germany’s and the Eurozone’s GDP Preliminary rates for Q1, UK’s Nationwide house prices rate, France’s and Germany’s Preliminary HICP rates as well as Switzerland’s KOF indicator figure all for the month of April. During the American session, we note the US Consumption Adjusted and Core PCE Price Index rates for March followed by Canada’s GDP for February and the US University of Michigan Sentiment Final figure for April.

USD – Recession worries in full swing

The USD is about to end the week unchanged against the common currency, pound and the Yen. On a fundamental note, we note that the Fed’s Beige Book clearly stated that banks tightened lending standards amid increased uncertainty and concerns about liquidity. The Fed also stated that consumer spending was seen as reduced which was validated by the Retail Sales data last Friday and the contraction of 1% for March, weakened the greenback as the economic outlook continues to deteriorate. On a monetary note, we highlight Fed Governor Waller who stated during a speech last Friday, “This growth would mean that, so far, tighter monetary policy and credit conditions are not doing much to restrain aggregate demand”. Also, according to Reuters New York Fed President Williams stated on Thursday, “Inflation is still too high, and we will use our monetary policy tools to restore price stability,” implying that the Fed may continue on its aggressive rate hiking path. On the flip side Philadelphia Fed President Harker stated that “The Fed is close to where it needs to be on interest rates” implying that the Fed may be near or reaching its terminal rate. On a macroeconomic level, we note the release of the S&P Mfg PMI for the US due out this afternoon, in addition to the US GDP rate for Q1 next Thursday as they may verify the expectations of a slowdown in economic activity as expressed by the Philly Fed Business index data for April. The indicator came in much lower than expected, at -31.3 compared to the expected -19.2 and thus may further weaken the dollar, should adverse releases emerge. On the other hand, should the data provide a contradictory outlook we may see the greenback strengthening and eating away at any negative sentiment generated by the Philly Fed Business index. Overall we highlight the market worries for a potential recession in the US economy and should they intensify we may see the greenback getting some safe-haven inflows.

GBP – Pound trades higher following CPI print

On a fundamental note, we highlight that the British economy seems to be on track to contract in 2023. As such the pound ending the week unchanged against the dollar and the yen may not be a sign of pound strength but dollar and Yen strengthening. On a monetary level, we highlight MPC Tenreyro’s speech last Friday in which she stated that “There are long lags in the transmission of monetary policy. We are still to see most of the tightening pass through.” In combination with stating that “Interest rates should be the last defense against financial stability risks,” this may imply that MPC Tenreyro is highly unwilling to continue hiking rates further during BoE’s May 13th meeting as her term nears an end. As such Tenreyro’s continued dovish comments may further weaken the pound if a similar rhetoric is echoed by other MPC members before the interest rate decision. We suggest though that the bank may proceed with another rate hike at least for the coming meeting, if not beyond. On a macroeconomic level, we note the release of the UK’s CPI print coming in higher than expected at 10.1% yoy, which implies that inflationary pressures are rampant in the UK economy and as such the bank may need to take decisive action by raising interest rates further. Furthermore, the Gfk consumer confidence, retail sales and preliminary manufacturing rates and figures validate the IMF’s hypothesis of a decline in the British economy. On the other hand, we also note the increase in economic activity for the UK’s critical services sector. Hence, we may see the pound fluctuating as the MPC debates on holding, cutting, or hiking rates in order to prevent the economy from entering a recession or to prevent further inflationary pressures. Traders may opt for further information due next week from the UK’s CBI figures and Nationwide house prices albeit the latter’s release may be postponed.

JPY – Yen finds unexpected support from safe-haven inflows

The JPY is about to end the week unchanged against the greenback and the pound, but slightly higher than last week’s close against the common currency. The movement implies that the JPY has held its ground as market tensions of a recession appear to have been elevated. Overall, the JPY is facing safe heaven inflows despite banking earnings week in the U.S appearing to be in relatively good shape which should have alleviated further banking fears. BoJ Governor Ueda last Sunday, re-iterated the need to stick to the ultra-loose monetary policy stating according to Reuters that “In many countries, inflation is very high or not slowing enough. The important thing is that the situation is quite different in Japan, which I explained at the meeting”. Furthermore, during his address to parliament, he stated that “The BOJ’s JGB purchases are managed out of the need of conducting monetary policy with the aim of achieving the 2% price stability target”, implying that the purchasing of Government bonds is monetary policy thus further weakening the JPY as a result of the ultra-loose monetary policy settings. On a macro level, we note the release of Japan’s CPI today and it was indicative of increased inflationary pressures, in the economy as the rate had increased for March on a month-on-month basis. Also please note that industrial production ticked upwards on Wednesday and Japan’s trade data came in better than expected on Thursday, indicative of an improvement in Japan’s international trading activity. With inflationary pressures still present, we may see the JPY strengthening as the pressure on BoJ may intensify before next week’s interest rate decision. Yet the bank is widely expected to remain on hold, and should its dovishness resurface, we may see JPY slipping. Also, note that this is to be the first interest rate decision of BoJ with Mr. Ueda at the helm.

EUR – Market worries heightened

The common currency remained relatively unchanged this week against the dollar, as well as against the pound and the Yen as these lines are written. Fundamentally, we acknowledge the fact that the French protests are continuing as last Friday the French Constitutional Court voted in favor of the deeply unpopular pension reforms, resulting in continued strike actions in France. The developments potentially are weakening one of Europe’s largest economies, affecting adversely the EUR in the long run. On a monetary front, we highlight the release of the ECB’s March meeting minutes in which policymakers Lane and Schnabel whose rhetoric appeared to be hawkish supported that “market-based indicators of longer-term inflation expectations had continued to point to elevated concerns that inflation would remain above the ECB’s target of 2%.” with ECB’s Lane suggesting “raising the three key ECB interest rates by 50 basis points”. Both comments may have provided support for the common currency, as they strengthen the case for further interest rate hikes. However, we note dissent amongst policymakers with some making the case to remain on hold in order to allow for a comprehensive re-evaluation of the ECB’s macroeconomic policy, hence potentially weaking the EUR if more dissenters join the dovish side. On a macro outlook, we note the contraction of economic activity in the manufacturing sector of not only Germany, but the Eurozone as a whole for the month of April. It’s characteristic that the relative preliminary PMI readings reached new post-pandemic lows. The readings are indicative of a potential slowdown in Germany’s economy and thus the Eurozone. EUR traders may extend their disappointment, next week in the event that Eurozone’s, France’s and Germany’s Preliminary GDP figures for Q1 slow further down showcasing the possibility of a recession. Overall, should ECB continue with its rate hikes, it may provide support for the common currency whereas slowing GDP data could weaken the EUR as it may lead to the ECB to rethink its strategy. Also critical to the market’s perception about the ECB’s intentions are expected to be the preliminary HICP rates for April of the Eurozone, next week.

AUD – AUD in trouble

The Aussie appears to have remained unchanged against the USD as this week draws to a close. On a fundamental note, we give emphasis to the rapid deterioration in the US-Sino relationship, potentially

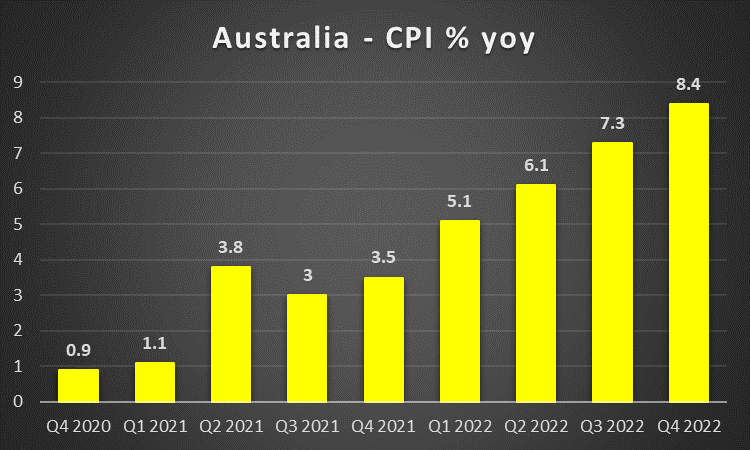

affecting in a negative manner the Aussie in the long run. Considering the recent developments of China’s continued military drills around the island of Taiwan, intensified fears of escalating tensions between the world’s biggest superpowers, which may negatively affect the AUD. Please note that China’s GDP for Q1 and retail sales growth rates for March both outperformed market expectations and tended to reassure markets that growth is back in China, with the internal demand side being particularly strong in the Chinese economy. On the flip side, the industrial production and urban investment growth rates undershot the market expectations tending to create worries for Aussie traders. On a monetary level, we highlight the release of the RBA’s April meeting minutes in which members acknowledged that “the tighter monetary policy stance was gradually flowing through to the real economy” implying that the RBA may remain on hold during its next meeting as well. Yet this is not definitive as the purpose behind the on-hold position in early April, was to gather additional data. Furthermore heading into next week’s financial releases with the CPI print for Q1, traders may be optimistic that the data will indicate the strengthening of the Australian economy, hence providing support for the AUD.

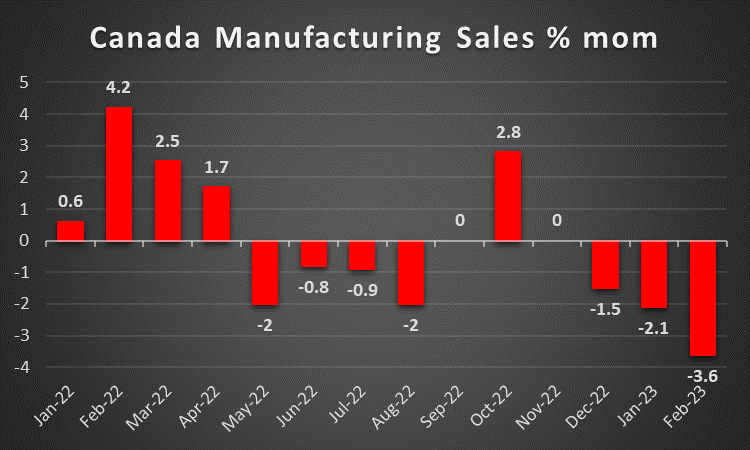

CAD – Loonie may see hikes in the future

The Loonie is about to end the week lower than the dollar. Fundamentally we note that a third of Canada’s federal workers went on strike on Wednesday, setting a record for the largest strike in the country’s history. This weakened confidence in the Canadian economy, and as a result, if the strike continues it may further weaken the CAD. On a monetary tone, BoC Governor Macklem on Tuesday stated in the event of increasing inflationary pressures that “we are prepared to raise the policy rate further to get there” hence we could attribute partial strengthening in the CAD as the comments made, seem to follow last week’s forward guidance that the bank anticipates that getting inflation to 2% would be more difficult. Implying that the BoC may continue hiking interest rates if the BoC feels it is necessary. On a macroeconomic level, we note the higher-than-expected CPI rate on a month-on-month level, on Tuesday, indicative of persistent inflationary pressures in the Canadian economy. This may have provided temporary support for the CAD, as it may place pressure on BoC, as there is now a case being made for further hikes should inflation rates show persistence. Furthermore, we also note Canada’s GDP rate for February due to be released next Friday, a lower-than-expected reading may weaken the CAD as it may limit the bank’s eagerness to hike leading to the Loonie weakening and vice versa. Also on a fundamental basis, we note that CAD’s weakening may have been heavily affect by the rapid deterioration in oil prices, as a Canada is a major exporter, hence the CAD may be weakened by dropping oil prices further.

General Comment

As a closing comment, following the Fed’s beige book, the outlook on the US economy is grim as “banks tightened lending standards amid increased uncertainty and concerns about liquidity”, highlighting the increased risks of a recession looming in the financial markets, which may lead to the USD continue to deteriorate, unless safe haven flows come to its rescue. In the US equities market, the market sentiment seems to have remained stable following the earnings releases by various banks and corporations this week, indicative of a resilient equities market going into next week’s releases. Yet the overall market worries for a possible recession in the US economy have turned the market sentiment towards a risk-off direction. We note some worries for companies not meeting the market’s expectations with their earnings reports which have also contributed to that end, such as Alcoa, Netflix and Tesla. Making a start on Monday we anticipate Coca-Cola’s (#KO) earnings, Tuesday we await the earnings release of Microsoft(#MSFT) followed by Google (#GOOG), VISA (#Visa), PepsiCo (#PepsiCo), McDonald’s (#MCD), General Electric (#GE), UBS(#UBS), 3M (#MMM) , General Motors (#GM), Xerox (#XEROX). On Wednesday we note Meta(#FB), Boeing (#BA), Ebay (#EBAY). Thursday, we anticipate Amazon (#AMZN), and Intel (#INTC). Also, the halt of the USD’s weakening may provide a cautionary tale to gold traders to be on alert for any possible weakening in the precious metal’s price. Gold reversed it direction by dropping this week, negatively being affected by the recovery of the USD and displaying once again their negative correlation.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.