Leaving a roller coaster week behind us, we open a window into what next week has in store for the markets. On the monetary front, we note from Sweden, Riksnbank’s interest rate decision on Tuesday, while BoJ is to release the summary of opinions of the bank’s March meeting on Thursday. As for financial releases, we note on Monday from the UK the CBI distributive trades for March and the GDP rate for Q4. On Tuesday, we get Germany’s GfK consumer sentiment for April, the US durable goods orders growth rate for February and consumer confidence for March. On Wednesday we get Australia’s CPI rate for February and the Eurozone’s business climate for March. On Thursday, we get Australia’s retail sales for February, Switzerland’s KOF indicator for March, Canada’s Business Barometer for the same month and from the US we highlight the final GDP rate for Q4, the weekly initial jobless claims figure and the final University of Michigan consumer sentiment for March, while from Canada we get the GDP rate for January. On Friday we get Japan’s Tokyo CPI rates for March and the preliminary industrial output for February, while from France we get the preliminary HIPC rate for March and from the US we get the consumption rate for February and the Core PCE price index for the same month.

USD – The Fed’s interest rate decision weakened the USD

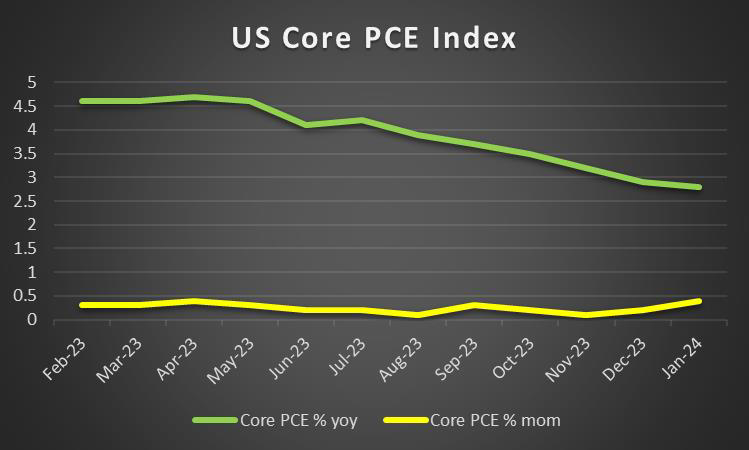

Despite a weakening of the USD on Wednesday, the greenback is about to end the week substantially higher than when it began. On a monetary level, we note the release of the Fed’s interest rate decision. The bank as was widely expected remained on hold and seemed to verify that rate cuts are coming. Yet in its accompanying statement, the bank also mentioned that “The Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2 percent” showcasing some hesitancy on cutting rates. Furthermore, the new dot plot verified the market’s current expectations for a total of three rate cuts in the year which also tended to weigh on the USD. Overall, should fed policymakers highlight that three rate cuts are a very possible scenario for 2024, we may see the USD being set under pressure on a monetary policy level. On a macroeconomic level, we note that the weekly initial jobless claims figure did not rise as expected, implying a relative tightness in the US employment market. Furthermore, we note the improved levels of economic activity in the US, for the manufacturing sector in March, as per implied by the release of the preliminary S&P PMI figures for the current month. Similarly despite the Philly Fed Business index for March dropping, it dropped less than forecasted implying that the situation may not be as bad as initially expected. We highlight as the next big tests for the USD the release of the final GDP rate for Q4 on Thursday and the Core PCE price index for February next Friday and should the rates show a resilience of inflationary pressures in the US economy, they could provide some support for the USD.

GBP – UK’s GDP Rates eyed

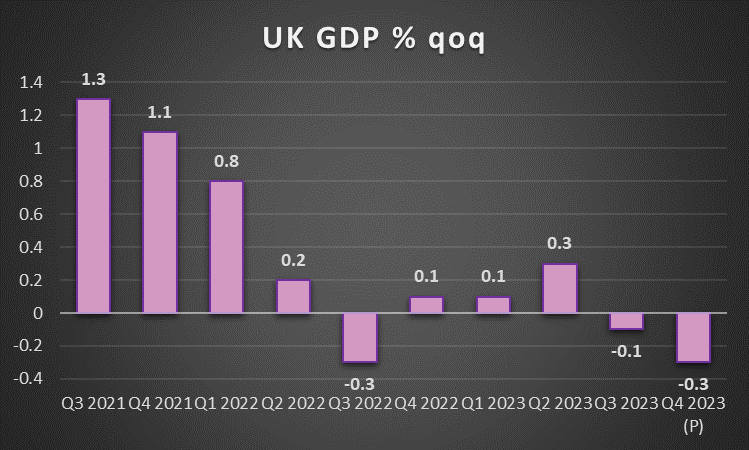

The pound is about to end the week lower against the USD and the EUR, yet still seems to be gaining some ground against the JPY. On a monetary level, we highlight BoE’s interest rate decision. The bank as was widely expected, remained on hold, keeping rates at 5.25%. It’s interesting that despite the wider-than-expected slowdown of the UK CPI rates for February, the majority within the bank to remain on hold strengthened with Policymaker Dinghra being the only which sees the necessity of easing the bank monetary policy at the current stage. On the other hand, no BoE policymaker seems to see the need for the bank to start hiking rates again, which may have not been a win for the doves yet it was a loss for the hawks. Understandably the release had a bearish effect on the pound. Yet in the accompanying statement, the bank does not seem to be in a rush to start cutting rates as it stated that “Monetary policy will need to remain restrictive for sufficiently long to return inflation to the 2% target sustainably”. We note that February’s CPI rates slowed down more than expected, while as for economic activity in the UK, the narrowing of the contraction of economic activity in the UK manufacturing sector was notable, as March’s preliminary PMI figure neared the reading of 50. In the coming week, we note the release of the UK’s GDP rates for Q4 and a possible acceleration could provide some support for the pound.

JPY – JPY hiked, yet that may be it

JPY is about to end the week in the reds across the board in a sign of wider weakness. The main market mover of the week for the Yen was the release of BoJ’s interest rate decision. BoJ hiked rates on Tuesday, to reach 0%-0.1%, and in its decision ended the seven-year-long negative rates policy as it stated that “The Bank considers that the policy framework of Quantitative and Qualitative Monetary Easing (QQE) with Yield Curve Control and the negative interest rate policy to date have fulfilled their roles.”. On the other hand, the bank has also stated that it will continue with its asset purchases indirectly maintaining rather loose financial conditions in the Japanese economy. It’s characteristic that despite the bank’s historic shift, JPY weakened, as the market may have been expecting more certainty regarding additional future steps towards a normalisation of the bank’s monetary policy. Yet any further steps towards further tightening of the bank’s monetary policy may prove to be difficult. The market on the other hand seems to expect the bank to

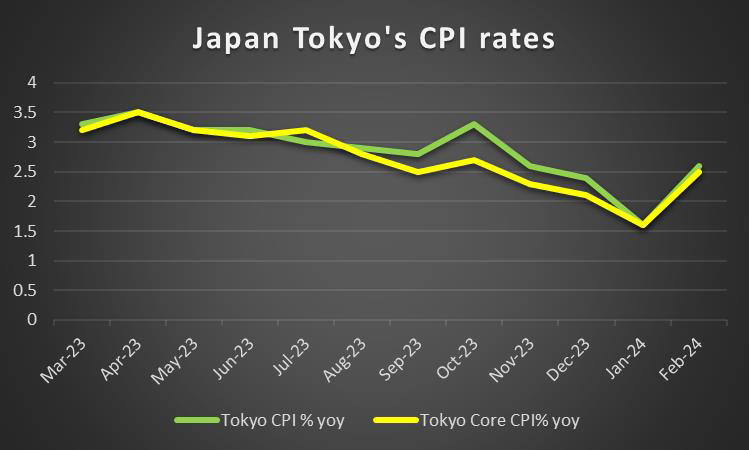

proceed with another two rate hikes within the year. We expect JPY to remain under pressure on a monetary policy level for the time being. On a macroeconomic level, we note the acceleration of the CPI rates for February, which tends to corroborate the bank’s narrative. Hence in the coming week, we will keep an eye out for the release of Tokyo’s CPI rates for March and a possible acceleration could be another indication of the persistence of inflationary pressures in the Japanese economy. As for economic activity, we note the release of Japan’s preliminary industrial output for February.

EUR – Fundamentals to lead the EUR

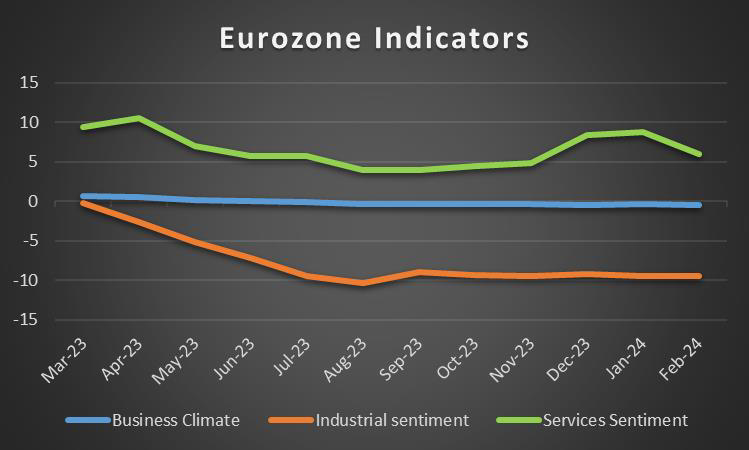

The common currency seems about to end the week lower against the USD, yet stronger against the JPY and GBP. On a monetary level, we note the comments of ECB President Christine Lagarde that the bank will not commit to any rate-cutting path. Nevertheless, we still see the case for the bank to proceed with rate cuts, yet the comments of Lagarde add more uncertainty to the timing and the size of rate cutting until the end of the year. Overall Lagarde’s statement tended to lean more towards the hawkish side yet the common currency did not seem to get any support on Thursday. The main reason why, may be based on macroeconomics as the preliminary PMI figures for March were released and overall the situation does not look so good for the trading bloc. We highlight the deeper contraction of economic activity for Germany’s manufacturing sector, which is considered the spearhead of the Eurozone’s economy, yet we have to note that the manufacturing sectors of other member states did not fare much better. On a brighter note, the services sector across the Zone was able to expand its economic activity at a faster pace, despite Germany’s and France’s services sectors suffering another contraction. Nevertheless, the release tended to intensify our worries about the macroeconomic outlook of the Eurozone and it seems that the release, understandably, tended to weigh on the common currency. On a fundamental level, we still note the war in Ukraine, which tends to maintain uncertainty in the Eurozone’s eastern flank, while centrifuge forces within the block are ever-present.

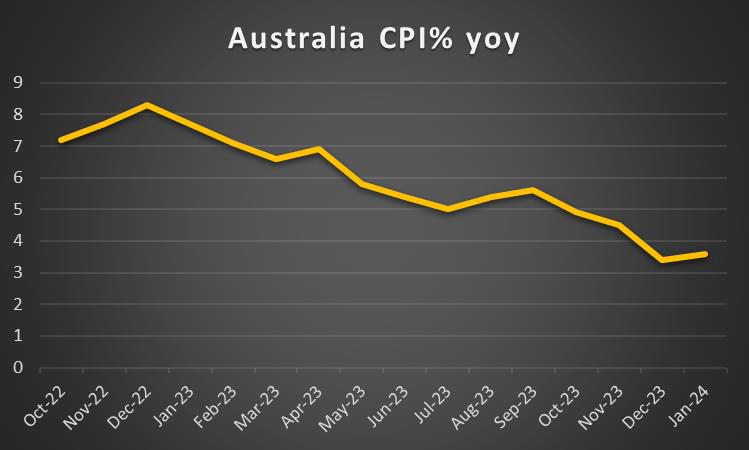

AUD – February’s CPI rates in focus

AUD is about to end the week slightly in the reds against he USD. On a monetary level we note RBA’s interest rate decision last Tuesday. RBA remained on hold as was widely expected keeping the cash rate target unchanged at 4.35 percent. Yet in the accompanying statement, the bank also seemed to ease on its hawkishness as it stated that “The path of interest rates that will best ensure that inflation returns to target in a reasonable timeframe remains uncertain and the Board is not ruling anything in or out.” AUD tended to weaken from the release, and we see the case for the Aussie to be under pressure on a monetary level, given that the monetary outlook direction seems to have shifted. On a macroeconomic level, though the picture changes at least for the Australian employment market as February’s data were impressive. The employment change figure rose far beyond expectations reaching 116.5k, while the unemployment rate dropped to 3.7% from January’s 4.1%. The release highlighted the tightness of the Australian employment market, yet the release may indirectly also harden the stance of RBA towards the hawkish side once again. Thus we highlight next week the release of February’s CPI rates, which are to provide another piece of the puzzle on a macroeconomic level. On a more fundamental level, we note the sensitivity of the Aussie as a commodity currency to the market sentiment but also towards China given the close Sino-Australian economic ties.

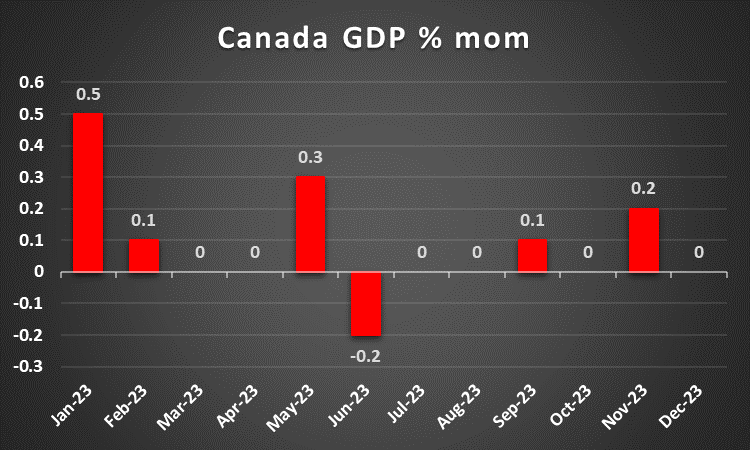

CAD – GDP rates to move the Loonie

The CAD is about to end the week lower against the USD. On a monetary level, we note the release of the deliberations of BoC’s March meeting. The document seemed to show that the balance of power among BoC policymakers is leaning towards rate cuts within the year. Yet there seems to be a split among BoC policymakers about the timing of any potential rate cuts. For the time being, we note that the market expects the bank to start cutting rates in the June meeting and deliver three rate cuts in total until the end of the year. Any rate cuts though would be dependent on whether macroeconomic data would fall in line with the bank’s projections. Thus we note the wider-than-expected deceleration of the CPI rates for February. Practically the rates have now well-entered BoC’s inflation target zone of 1%-3%. Hence the slow-down tended to enhance the market’s expectations. In the coming week, we get another clue about Canada’s economic outlook, namely the GDP rate for January. Any deceleration below December’s stagnation levels could weigh on the CAD. On a deeper fundamental level, we note the positive correlation of the CAD with oil prices. Oil prices for the current week seem to have moved very little, yet the US oil market seems to remain tight and there are some uncertainties regarding the supply side of the international oil market. Should oil prices start rising in the coming week we may see the CAD also getting some support.

General Comment

Overall we expect volatility in the FX market to ease given that the number of high-impact financial releases and monetary policy events is to be reduced. We may see the USD relenting some of the initiative in the FX market to other currencies, yet at the same time, we still see the greenback leading the market. As for US stock markets, we note that equities bulls were allowed to take the driver’s seat. One of the main drivers of the rise of equities may have been the Fed’s interest rate decision. Also, the AI frenzy of the market seems to be taking the lead once again. Overall we once again see the tech sector leading the markets, with AI-related companies generating substantial interest among market participants. At the same time we note the problems faced by Boeing, an issue also mentioned in last week’s report, while Apple got sued by the US Justice department for violations of antitrust laws and the issue could weigh on the share’s price. Moving now to the gold market, gold’s price rallied regaining all of last week’s losses, even at some point gold’s price was able to reach a new record high of $2222 per ounce. The negative corelation of the USD with gold was not in reflected in this week’s movement, given that both trading instruments, gold and the USD, were on the rise. But despite USD rising, the drop of US yields may have allowed gold’s price to rise. We expect in the coming week the negative correlation between gold and the USD to be on display once again, hence should the USD gain further traction we may see some bearish tendencies developing for gold’s price.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.