As the week draws to a close, we note that the US employment report for November is still to be released as these lines are written. In the coming week, we note that on a monetary level, we highlight the release of Fed’s interest rate decision on Wednesday and also note the release of ECB’s, BoE’s, Norgesbank’s and SNB’s interest rate decisions on Thursday. As for financial releases, we note on Monday the release of Norway’s and the Czech Republic’s CPI rates for November. On Tuesday we get Japan’s corporate goods prices for November, UK’s October employment data, Norway’s GDP rate for October, Germany’s ZEW indicator for December and we highlight the US CPI rates for November. On Wednesday we note the release of Japan’s Tankan indexes for Q4, UK’s October GDP rate, Eurozone’s industrial output for the same month, the US PPI rates for November and New Zealand’s GDP rate for Q3. On Thursday we get Japan’s machinery orders for October, Australia’s employment data for November, Sweden’s CPI rates for the same month, the US weekly initial jobless claims figure, the US retail sales for November and Canada’s manufacturing sales for October. On Friday, we get Australia’s, Japan’s, Germany’s, France’s, Eurozone’s, the UK’s and the US preliminary PMI figures for December, while we also note the release of China’s industrial output for December and the US industrial production growth rate for November.

USD – Fed’s interest rate decision to move the USD

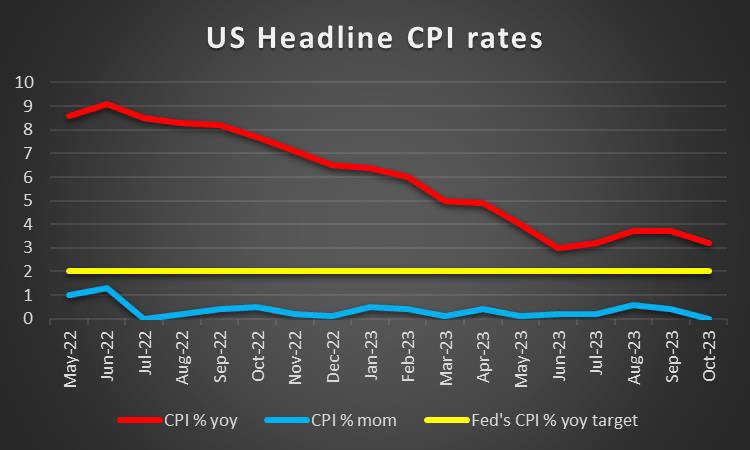

The USD seems about to break the three-week losing streak against its counterparts, yet the US employment report for November is still to be released and could alter the picture. The next week is to be very interesting for the greenback. We make a start with the release of the US CPI Rates for November on Tuesday. The forecasts are for inflationary pressures to have eased in the past month. Should that be the case we may see the market’s expectations for an earlier rate cut by the Fed in 2024, intensifying which could weaken the USD ahead of the Fed’s interest rate decision on Wednesday. The bank is widely expected to remain on hold at the range of 5.25-5.50% and its characteristic that Fed Fund Futures imply that the market has currently almost fully priced in such a scenario, with a 99% probability. It should also be noted that the market seems to also expect the bank to start cutting rates as early as March next year and proceed with another four rate cuts until 2024 is over. So the market’s attention is expected to be on the Fed’s accompanying statement and Fed Chairman Powell’s press conference later on. Should these two elements remain hawkish contradicting the market’s expectations for an early rate cut, we may see the USD relenting some ground and vice versa. The release may have ripple effects beyond the FX market, say for example on gold and US stock markets. Yet the suspense for USD traders is to be continued as on Thursday we note the release of the US retail sales consumer confidence for November and on Friday we get the preliminary S&P PMI figures for the same month.

GBP – BoE to remain on hold

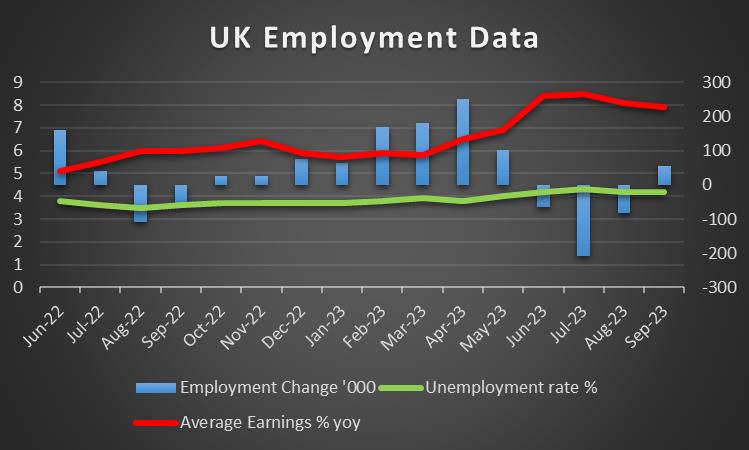

The pound is about to end the week lower against the USD and the JPY and EUR. Pound traders are expected to have an interesting week ahead. We make a start on Tuesday, with the release of UK’s employment data. Should the data show that the UK employment market shows signs of tightening, say for example the unemployment rate drops and the employment change figure rises, we may see the pound getting some support and vice versa. On Wednesday we shift our attention towards economic activity, as October’s GDP and manufacturing output growth rates are to be released. A possible acceleration could provide a boost to pound traders’ morale. The main release though is expected to be BoE’s interest rate decision on Thursday and the bank is widely expected to remain on hold, keeping rates at 5.25% and GBP OIS imply a probability of 98.55% currently, for such a scenario to materialize, practically rendering the interest rate part of the decision as an open and shut case. Hence, market attention is expected to fall on the bank’s future intentions. The market is expecting the bank to start easing its tight monetary policy from June onwards and proceed with a total of four rate cuts in the coming year. We expect a certain degree of hawkishness as the CPI rates, despite a substantial slowdown in October, are still high. Yet a possible recognition that the bank’s rates are in a restrictive territory, could reassure the markets that rate cuts are under way and could weaken the pound. Yet pound traders are also expected to pay attention to the release of the preliminary PMI figures for December, with a special focus being on the services sector indicator.

JPY – BoJ’s intentions, the catalyst for JPY’s direction

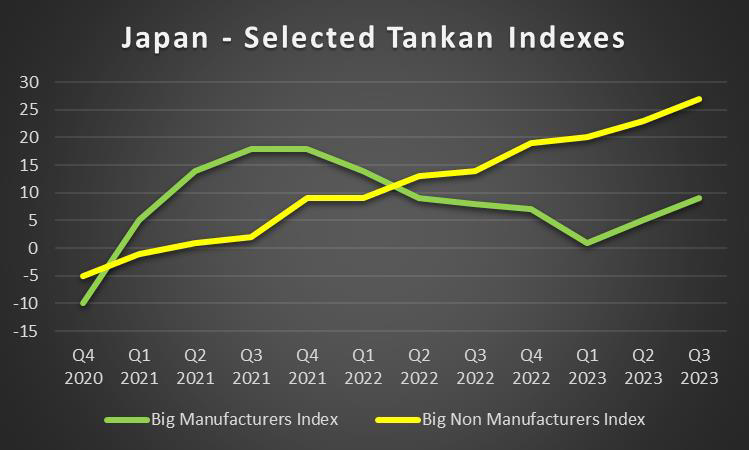

JPY is gaining ground across the board in a sign of broader strength. Despite the restart of hostilities in Gaza, tensions over Venezuela’s intentions to annex part of Guyana, tankers being seized at the Persian Gulf and understandably a market participant expecting some safe-haven inflows for the Japanese currency, we turn our attention elsewhere. We consider the intentions of BoJ as the main catalyst behind JPY strengthening. It’s characteristic that JPY gained substantially on Thursday after BoJ Governor Ueda’s statements in the late Asian session. The BoJ Governor seemed to imply without providing a timeframe, that the era of negative rates is to be ended, as he visited Japan’s Premier Kishida. The BoJ Governor stated that BoJ does not know what level of interest rate is to be targeted once the negative rates policy is ended. Yet he also implied that such a move may still be premature. Overall, should we see more BoJ policymakers implying an end of the negative rate policy, we may see JPY being supported as it would strengthen the market’s expectations for a possible rate hike as early as March. On a macroeconomic level, we note that Tokyo’s CPI rates for November slowed down, which may foreshadow a slowdown on a national level, given the density of Tokyo’s population. Should rates continue slowing down, we may see some obstacles rising on the path towards a normalisation of BoJ’s monetary policy. Yet the issue extends also towards economic activity as our worries for the economic outlook of Japan tend to intensify after the release of the revised GDP rate for Q3, which showed a wider contraction than initially calculated. In the coming week, we intend to concentrate on the Tankan indexes for Q4 in an effort to gauge the outlook and economic activity of the Japanese economy.

EUR – ECB could go first

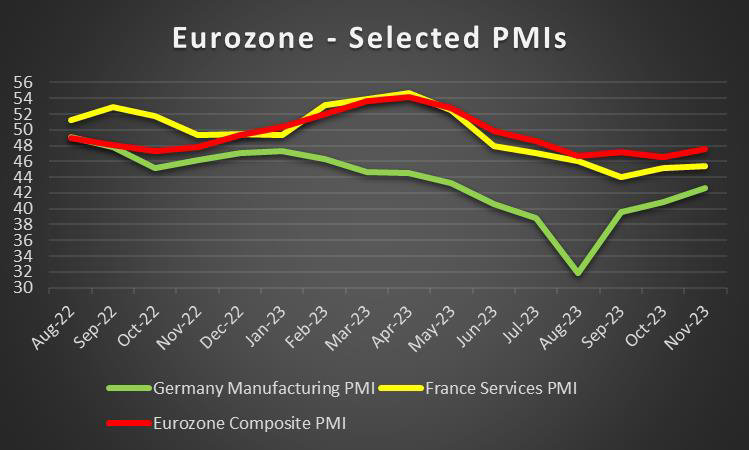

The common currency is about to end the week in the reds against the USD and JPY, yet remains relatively unchanged against the GBP. The monetary policy outlook of the ECB seems to be weighing on the common currency. For the time being the market is expecting the bank to remain on hold on Thursday keeping the refinancing rate at 4.5%. Currently, EUR OIS imply a probability of 94.56% for such a scenario to materialise, yet also that the bank is to start cutting rates in early March and end the year with a total of 6 rate cuts. It should be noted that the HICP rate has slowed down considerably in November’s preliminary release, nearing the bank’s 2% target, strengthening the case for earlier rate cuts. Should the bank on Thursday in its accompanying statement and/or ECB President Lagarde’s press conference later on, show signs that the bank intends to start cutting rates early next year, we may see the common currency losing some ground. Yet we also tend to remain worried about economic activity and growth, given the contraction marked by the revised GDP rate for Q3, despite being a shallow one. Hence we tend to focus also on the release of the preliminary PMI figures for December, with a special focus being on Germany’s manufacturing PMI figure. Should we see an improvement in economic activity, we may see EUR traders getting a boost, yet should the figures remain below the cut-off point of 50, implying another contraction of economic activity, yet narrower, we may see that boost being moderated.

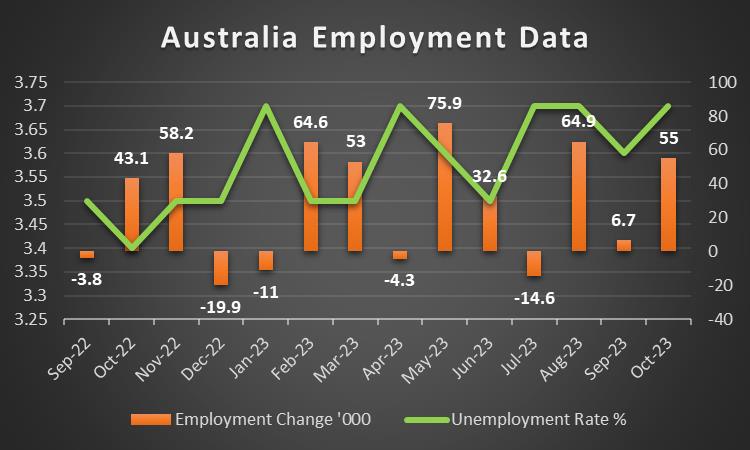

AUD – Employment data to move the Aussie

AUD is about to end the week in the reds against the USD. On a monetary front, we note that RBA remained on hold at 4.35%, as was widely expected. The RBA Governor Bullock’s accompanying statement hinted that inflationary pressures in the Australian economy continued to “moderate” and as such, may imply that the bank may have reached its terminal rate. Furthermore, the bank implied that inflationary pressures in the economy, continue to moderate, which may further imply that the bank may have reached its terminal rate. Therefore, the statements made by the bank appear to be predominantly dovish, which appears to have weighed on the Aussie. On a fundamental level, we note that the market sentiment may have a wider effect on AUD’s direction, given that the Aussie is considered as a riskier asset, given its commodity currency nature. Also Aussie traders may keep an eye out for the situation in China, given the close Sino-Australian economic relationships. We have to note that the lukewarm Chinese trade data for November, especially the contraction of the import rate, did not seem to excite Aussie traders. Yet on a macroeconomic level, the beyond-market expectations acceleration of the real GDP rate for Q3, seemed to provide some support for the Aussie. On the other hand, the narrower-than-expected widening of Australia’s trade surplus left Aussie traders rather unimpressed. Other than we note the release of Australia’s November business conditions and outlook indicators, as well as December’s consumer confidence. Yet the highlight of next week for Aussie traders, is expected to be employment data for November on Thursday and should the data show that the Australian employment market remains tight we may see the the Aussie getting some support. From China we note the release of industrial output and urban investment growth rates for November on Friday.

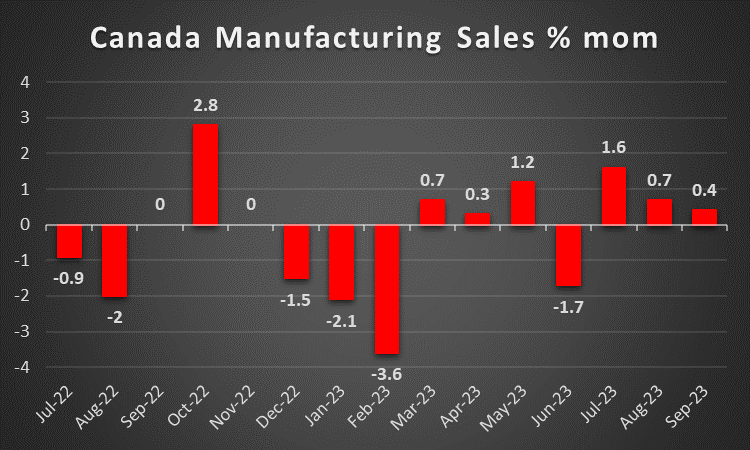

CAD – Fundamentals to lead the way

The Loonie is about to halt its winning streak against the USD and end the week in the reds. On a monetary level, Bank of Canada remained on hold as was widely expected on Wednesday. In the bank’s accompanying statement, they stated that “The slowdown in the economy is reducing inflationary pressures in a broadening range of goods and services prices”, which could further imply that the bank is done with interest rates. As such, the perceived dovish statement by the bank, may have weakened the Loonie. On a fundamental level, we note that the weakening of oil prices over the week, may have intensified some bearish tendencies for the Loonie. It should be noted that the oil market tends to remain worried about

possible weak demand levels from China and the US. Should oil prices continue weakening, we may see them weighing on the Looney, given Canada’s status as a major oil producer. On a macro-economic level, we note that the release of November’s employment data showed an easing of Canada’s employment market’s tightness as the unemployment rate ticked up despite an unexpected rise of the employment change figure which tended to provide some support for the Looney. Also, the widening of Canada’s trade surplus unexpectedly widened providing some support for the CAD. Except for the release of October’s manufacturing sales and November’s house starts on Thursday and Friday respectively, we have no major financial releases in the calendar for CAD traders, thus we expect fundamentals to lead the CAD in the coming week.

General Comment

Overall we expect in the coming week the USD to maintain the initiative over other currencies, given the frequency and gravity of US financial releases. Yet there are a number of high-impact financial releases and monetary policy events that do not stem from the US and could allow other currencies to select their direction. Overall we expect that volatility is to pick up given the high number of high-impact releases from various countries. In regards to US stock markets, we got some mixed signals in the past week and expect fundamentals to lead the way. Special focus could be placed on the Fed’s intentions, yet US financial releases may also provide some increased volatility for equities. On the other hand, gold’s price tended to maintain its negative correlation with the USD and ended the winning streak of the past three weeks ending the current week in the reds. At this point, we have to note that gold’s price dropped despite US bond yields dropping which may have smoothened the losses for the precious metal. Overall, we tend to maintain our expectation that gold’s negative correlation with the USD could be maintained in the coming week despite some asymmetry being present and hence expect that high-impact releases from the US could have also ripple effects on gold.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.