As the week is nearing its end, we have a look at what next week’s calendar has in store for the markets. On Monday, we note the release of Japan’s preliminary GDP rate for Q4 24 and Canada’s House Starts for January. On Tuesday, we highlight from Australia RBA’s interest rate decision, UK’s December employment data, Sweden’s January CPI rates, France’s final HICP rate for January, Germany’s ZEW indicators for February and Canada’s CPI rates for January. On Wednesday, we get from Japan December’s machinery orders and January’s trade data, from Australia the wage Price index for Q4, from New Zealand we highlight the release of RBNZ’s interest rate decision, UK’s CPI rates for January and from the US the release of the Fed’s January meeting minutes. On Thursday we get Australia’s January employment data, UK’s nationwide House prices, the US weekly initial jobless claims figure, the US Philly Fed Business index for February and Euro Zone’s preliminary consumer confidence for February. On Friday we get the preliminary PMI figures for February of Australia, Japan, France, Germany, Euro Zone and the US as well as Japan’s CPI rates, UK’s retail sales for January, France’s business index for February, Canada’s retail sales for December and the US final UoM consumer Sentiment.

USD – Fed’s January meeting minutes in focus

The Fed seems to maintain rather hawkish intentions. Fed Chairman Powell’s testimony before the US Senate tended to highlight that tendency as Powell stated that the US employment market remains tight and inflation, despite still being above the banks’ 2% target, has slowed down. As for monetary policy, the Fed seems to be in no hurry to cut rates, a comment that implied a continuance of the tight financial conditions in the US economy for the time being. Interestingly Fed Chairman Powell also in answering questions, despite not stating his opinions on the correctness of Trump’s intentions to impose tariffs and in general the US President’s policies, he did acknowledge the possibility of an inflationary effect. Hence, we highlight the release of the Fed’s January meeting minutes next Wednesday and should the bank maintain a hawkish tone in the document we may see the USD getting some support as the market’s expectations for a hawkish approach by the Fed could be enhanced.

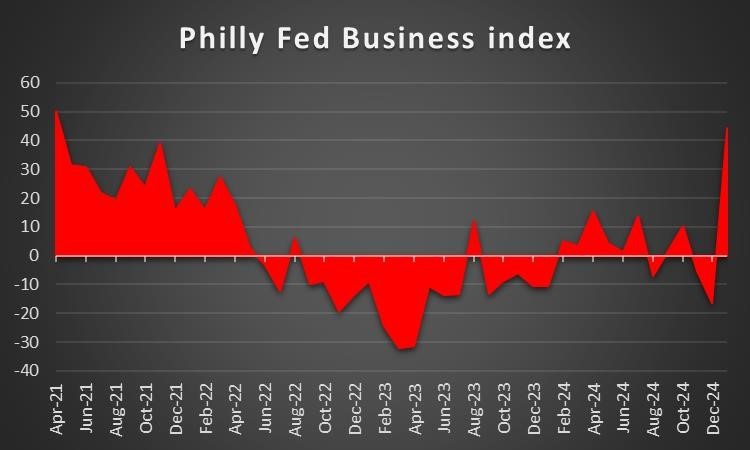

On a macroeconomic level, we note that market reactions from the release of the weaker-than-expected employment report for January were eclipsed by the acceleration of the US CPI rates for the same month. The release highlighted a resilience of inflationary pressures in the US economy, thus providing support for the USD. It should be noted that acceleration of the CPI rates were also supported by an acceleration of the price growth at a producers’ level, showing more depth. Overall the resilience of inflationary pressures in the US economy may harden the Fed’s hawkish intentions and its characteristic that before the CPI release Fed Fund Futures implied an expectation for the bank to cut rates in the July meeting, yet after the release expectations shifted towards the September meeting. In the coming week, we note the release of the Fed Philly business index for February and a possible rise off the indicator’s reading could provide some support for the USD.

On a fundamental level, we note that US President Trump announced on Monday that he intends to apply 25% tariffs on all US steel and aluminum imports, “without exceptions and exemptions”. He also announced reciprocal tariffs on imports from any country that imposes tariffs on US exports. It should be noted that the time of the announcement coincided with the arrival of Indias’ Prime Minister Modi, a country that imposes possibly the highest tariffs on US products. In any case, Trump’s intentions to impose tariffs and his mercantile, protectionist approach, combined by a wide degree of unpredictability and his flamboyant style, tends to enhance market uncertainty about the US and global economic outlook. Given the prementioned fundamental change, the USD may get some increased safe haven inflows, should the uncertainty caused by US President Trump be enhanced. Furthermore we also note the possible inflationary effect of Trump’s policies on imports and immigration, which could also provide some support for the USD as it may harden the Feds’ stance even further.

Analyst’s opinion (USD)

“We expect the USD to continue to be supported in the coming week and base this assumption mainly on the market expectations for a relatively hawkish Fed and the uncertainty caused by Trump. Should these two factors eclipse, we may see the USD retreating. ”

GBP – Employment and inflation data in focus

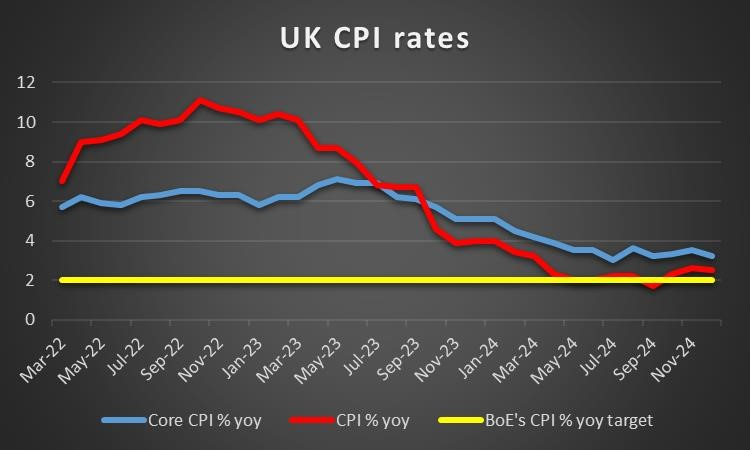

On a monetary level for pound traders, BoE’s dovish approach tends to weigh on the GBP. Bank of England Monetary Policy Committee member Catherine Mann’s worries for the demand side of the UK economy were characteristic of a maybe increasingly dovish approach by BoE. Furthermore we note that the market expects the bank to deliver another two rate cuts until the end of the year, as per GBP OIS, hence the market remains dovishly inclined. Yet the actual course of the bank is dependent on the path of inflation primarily, hence we note the release of the UK CPI rates for January next Wednesday. We also note that BoE Governor Andrew Bailey may comment on the bank’s intentions on Tuesday and should he sound dovish the market’s expectations for a faster rate cutting path, we may see the pound slipping.

On a macroeconomic level, pound traders were pleasantly surprised on Thursday as the UK’s preliminary GDP rate for Q4 24, unexpectedly accelerated. The release despite the actual acceleration on a quarter on quarter level may seem minimal, it tends to remove the possibility of a recession in the UK economy for now. In the coming week, we get a number of financial data which could attract pound traders. We make a start with the release of the UK employment data for December on Tuesday. A possibly tighter UK employment market could provide some support for the pound as it could ease worries for the demand side of the UK employment market. On Wednesday, we get UK’s CPI rates for January and should the headline rate fail to slow down on a year on year level and generally the rates show a resilience of inflationary pressures in the UK economy, we may see the pound getting some support for the GBP, as the release may ease the market’s dovish expectations for BoE. Finally on Friday, we get the preliminary UK PMI figures for January, with special interest being placed on the services sector. Should the figures show a faster expansion of economic activity in the UK services and manufacturing sector, we may see the pound getting some support.

Analyst’s opinion (GBP)

“In the coming week, we expect pound traders to focus primarily on the release of financial data given the heavy calendar and to a second degree also on BoE’s monetary policy intentions. On the one hand, improving financial data could support the pound while on the flip side a dovish BoE could weigh on the sterling”

JPY – GDP and CPI rates to move the Yen

JPY seems about to end the week in the reds against the USD, EUR and GBP in a sign of a wider weakness for the Japanese currency. On a fundamental level, we note that JPY’s safe haven qualities are still a possible market mover. Should we see market worries about a possible trade war easing we may see JPY losing some ground and vice versa. Also we note the rise of Japanese bond yields with the heavy point being longer term bonds, which could reduce the attractiveness of carry trade with the Yen on the short side. In our opinion the rise of US bond yields ends to highlight also expectations of the market for further tightening of BoJ’s monetary policy and should the upward tendency of Japanese bond yields be maintained in the coming week we may see JPY getting some support. On the flip side, should that Japanese bond yields start falling in the coming week, we may see JPY getting under pressure again.

On a monetary level, we note BoJ’s hawkish intentions. It’s characteristic that BoJ Governor Ueda, stated on Wednesday, that the rise of food prices may persist and recognised its possible effect on consumers. The comment was deemed as hawkish as persistence of inflationary pressures in the Japanese economy, could lead to further rate hikes by BoJ. We note that market expectations for the bank currently is to deliver another rate hike, possibly in June. Coming Wednesday we note the planned speech of BoJ board member Takata Hajime and should he sound hawkish we may see the market’s expectations for a rate hike by BoJ intensifying and thus providing some support for JPY

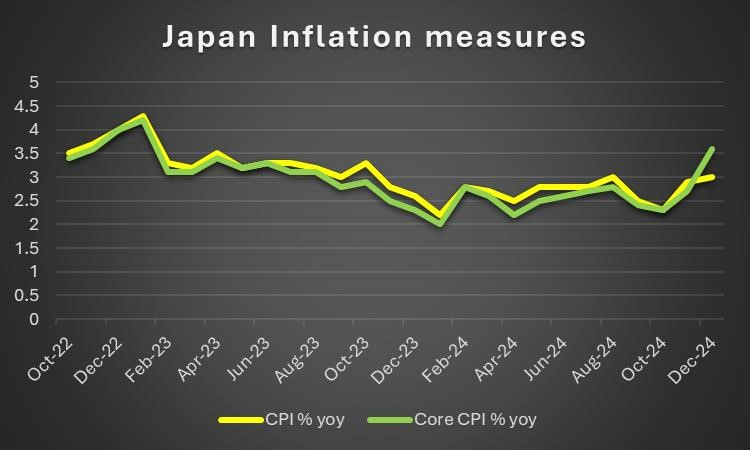

Lastly on a macroeconomic level, despite financial data not being usually major movers for JPY, we note the acceleration of the corporate earnings growth rates for January, while in the coming week, we get some high impact financial releases that could move the JPY. We make a start on Monday with the release of Japan’s preliminary GDP rate for Q4 24 and should the rates show a slowdown in the growth rates of the Japanese economy it could weigh on the Yen. At the end of the week we highlight the release of Japan’s CPI rates for January and a possible acceleration could provide some support for JPY as it would imply a relative persistence of inflationary pressures in the Japanese economy thus enhancing the market’s expectations for a hawkish BoJ.

Analyst’s opinion (JPY)

“Despite recognizing BoJ’s intentions being possibly the main driver for JPY’s direction in the coming week, a possible out of expectations rate in the releases of the GDP rates and the CPI rates could prove to be market movers for JPY. As for monetary policy, should market expectations for BoJ become more hawkish we may see the JPY getting some support.”

EUR – Peace prospects for Ukraine may support EUR

On a fundamental level, we note the possibility of a deal for Ukraine between the US and Russia. Such expectations intensified after US President Trump announced that the US is to pursue negotiations with Russia for peace in Ukraine. It’s being mentioned that most of Putin’s terms are met that meaning that the conquered land by Rusia is to be annexed, Ukraine is to be prevented from entering NATO, while elections in Ukraine could also be held, which in turn could allow for Putin’s claim for change of government in Kyiv. It also remains unclear what role Ukraine and the EU would have in these negotiations. For the time being it seems that the prospect of peace in Ukraine and thus a stabilization in EU’s east flank could provide some support for the EUR, yet we view the situation as still quite fluid. Also the political scene within the EU seems also to remains rather fluid, given that on the one hand, the French government survived a no confidence vote, yet on the other hand, negotiations for a government in Austria fell through, while the German Federal elections are nearing. Also on a fundamental level, Trump’s intentions to impose reciprocal tariffs could affect Eurozone’s products entering the US, an issue which also tends to weigh on the EUR.

On a monetary level, we note ECB’s dovish intentions as having a bearish effect on the EUR. Currently market expectations are for the bank to proceed with another three rate cuts until the end of the first half of the year. The market’s dovish expectations over the past week were maintained and ECB policymakers tended to feed such expectations. In the past week ECB President Lagarde and Vice President De Guindos highlighted the risks related to trade on an international level, given Trump’s tariffs and its possible negative consequences on growth. The overall situation with growth stagnating in the Eurozone tend to intensify the need for the ECB to remain substantially dovish. While, as reported by Reuters, ECB policymaker Vujčić noted that the market is pricing in three more rate cuts this year and added that those expectations are not unreasonable. We see the case for the dovish stance of the ECB not to change in the coming week and thus continue to weigh on the common currency on a monetary level as the interest rate differential outlook of the ECB continues to diverge with the Fed.

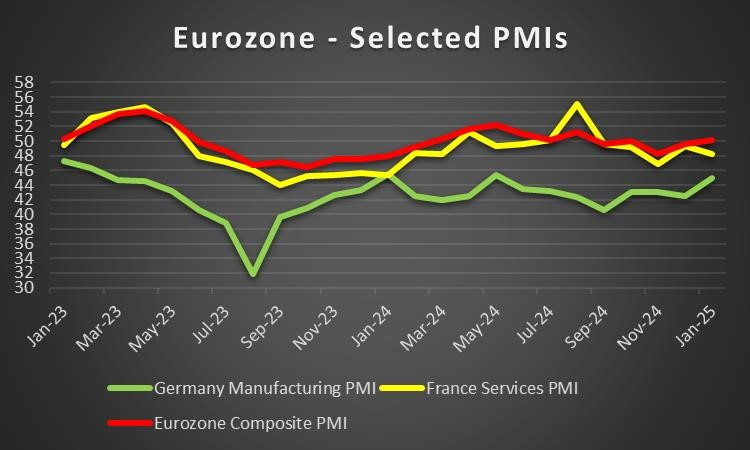

On a macroeconomic level, we note the revised GDP rate for Q4 and in the coming week we get a number of interesting financial data and we intend to focus, near the end of the coming week on the release of the preliminary PMI figures for February, given that the main issue tantalizing currently the Eurozone is growth and economic activity. Main area of interest could be Germanys’ manufacturing sector, yet also the indicators of the France’s services sector and the Eurozone’s composite PMI figure could move the common currency. Currently the indicators’ reading are expected to rise slightly, which on the theoretical side should provide some support for the EUR, as they improve, yet we still have some way to go before solid paces of expansion returns, especially for Germany’s manufacturing sector.

Analyst’s opinion (EUR)

“In the coming week, we expect interest of EUR traders to revolve around the release of the preliminary PMI figures for January on Friday, while further indications for peace in Ukraine could provide some support for the EUR. On the flip side, the dovish intentions of the ECB could weigh on the EUR.”

AUD – RBA to cut rates?

Aussie traders are expected to keep a close eye on the release of RBA’s interest rate decision next Tuesday. We note that the market seems to expect the bank to proceed with a 25 basis points rate cut and AUD OIS imply a probability currently of 79.3% for such a rate cut, while the other 20% seems to imply that the bank may remain on hold. We see the case for the bank to proceed with a rate cut on Tuesday’s meeting as the CPI rates for Q4 slowed down considerably despite some resilience in November and December. At the same time the Australian employment market seems to be remain rather tight with the unemployment rate dropping over the second half of 24, despite a tick up in December. Also the rate cut as such could have a bearish effect on the Aussie as it may disappoint market participants expecting the bank to remain on hold. Should a rate cut be delivered, we may see the markets’ attention turning towards the bank’s forward guidance. Should the bank hold a dovish tone implying that more rate cuts are to come, we may see AUD weakening, while should the bank show increased uncertainty for more rate cuts to come, we may see the Aussie getting some support.

On a fundamental level, we highlight US President Trump’s trade war to be negatively affecting the Aussie as its considered to be a riskier asset and given the close Sino-Australian ties, as Trump semes to be increasingly targeting China. One silver lining worth mentioning though would be that Australia may be able to avoid the US tariffs on Australian products, as Australia claims to have a trade deficit with the US. Should market worries for US tariffs intensify over the coming week we may see the Aussie retreating.AS for the situation in China, we note the slight acceleration of the CPI rates for January as a signal of a possible slight improvement of the Chinese demand side, yet even that may not be sufficient to convince traders for the improvement of China’s economic outlook as it may be related to the Chinese New Lunar year festivities.

On a macroeconomic level Aussie traders may focus on the release of Australia’s January employment data on Thursday’s Asian session. We also note the release of the wage price index for Q4 on Wednesday as an indicator to keep an eye out. Should the Australian employment data show a tight employment market, we may see the Aussie getting some support and vice versa. Also some interest could be placed on the release of Februarys’ preliminary PMI figures on Friday.

Analyst’s opinion (AUD)

“We expect RBA’s interest rate decision to be key in regards to the Aussies’ direction next week, yet a possible beyond expectations employment report for January could have also major consequences for AUD.”

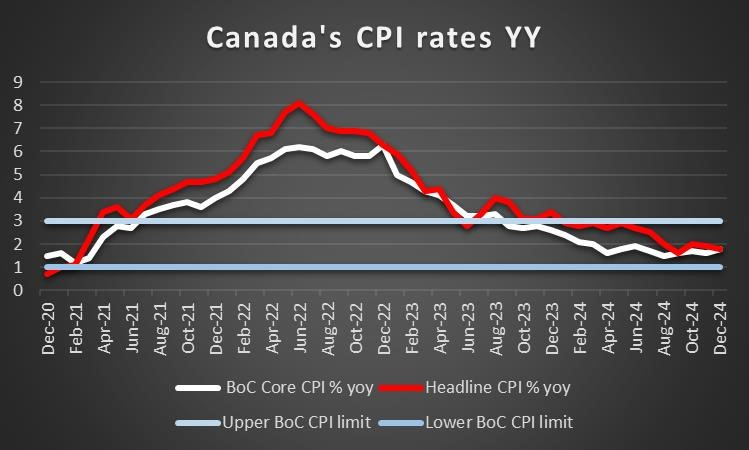

CAD – January’s CPI rates to shake the Loonie

On a fundamental level, the US threat to impose tariffs on Canadian products tends to weigh on the Loonie. Yet the CAD seems about to end the week stronger than the USD reaching levels not seen in two months. Yet the strengthening of the CAD against the USD may have been fueled also by the drop of US Treasury yields on Thursday. On the other hand the rise of oil prices which could provide some support for the Loonie as well, was abruptly interrupted on Wednesday. We see the case for the tariff war to be maybe the main determinant on a fundamental political level, that could affect the Loonie’s direction and should market worries intensify for the possible adverse effects of Trump’s tariffs on the outlook for the Canadian economy, we may see the Loonie slipping.

On a monetary level we note that the market has pushed back against the idea of a March rate cut by the BoC and currently market expectations are for the bank to deliver its next rate cut in the April meeting and deliver another rate cut in the July meeting, as per CAD OIS. On eveent thtm ay have forced the pmarket to reposition itself may have been therelase of Januarys’ employment report, showing a tight Canadian employment market which could allow BoC to delay any rate cuts. Yet the factor behind BoC’s intentions is expected to be inflation. Hence we highlight BoC Governor Macklem’s fireside chat participation and should he make any less dovish commetns than what the market expects, we may see the Loonie getting some support. Please ntoe that Mr. Macklems appearance is to take place after the release of Canada’s CPI Rates for January.

On a monetary level we note that the market has pushed back against the idea of a March rate cut by the BoC and currently market expectations are for the bank to deliver its next rate cut in the April meeting and deliver another rate cut in the July meeting, as per CAD OIS. On event that may have forced the market to reposition itself may have been the release of Januarys’ employment report, showing a tight Canadian employment market which could allow BoC to delay any rate cuts. Yet the factor behind BoC’s intentions is expected to be inflation. Hence we highlight BoC Governor Macklem’s fireside chat participation and should he make any less dovish comments than what the market expects, we may see the Loonie getting some support. Please note that Mr. Macklems appearance is to take place after the release of Canada’s CPI Rates for January.

On macroeconomic level, we highlight the release of January’s CPI rate, next Tuesday. Should the rates fail to slow down implying a relative persistence of inflationary pressures in the Canadian economy, we may see the Loonie getting some support as the release could enhance the market expectations for the BoC to remain on hold for longer, while a slowdown of the rates signaling an easing of inflationary pressures cause the Loonie to slip. On Friday we note the release of Canada’s retail sales for December and a possible slowdown could weigh on the Loonie as it would imply that the average Canadian consumer is less willing and/or able to actually spend more in the Canadian economy.

Analyst’s opinion (CAD)

“We currently see the case for the Loonie to continue to strengthen in the coming week, yet that may ultimately depend also on the release of January’s CPI rates. On the fundamental level, we highlight nay intensification of the US trade war that may have a bearish effect on the Loonie as well. ”

General Comment

As a closing comment, we expect the influence of the USD in the FX market to ease in the coming week as US financial releases are to be reduced in frequency and gravity. Yet given the unpredictability of US President Trump we also advise traders to expect the unexpected. US stock markets remained in a sideways motion over the past week despite some support provided on Thursday. Overall the US equity markets tended to display a wait and see behavior amidst wide uncertainty, which was only interrupted on Thursday as there were some signs of an easing inflation in the release of the US PPI rates. As for gold’s price, the upward motion seems to have no end as the precious metal’s price is about to end the week in the greens for a seventh consecutive time and seems to be constantly reaching new record high levels.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.