The week is about to end as we open a window to what next week has in store for the markets. We make a start with Sunday as in Japan elections for the House of Councilors will take place. On Monday, we note the releases of New Zealand’s CPI rates for Q2, UK’s house prices by Rightmove for July, Canada’s PPI rates for June and on a monetary level, we get from China PBoC’s interest rate decision. On Tuesday, we get New Zealand’s June trade data while in Australia, RBA is to release the minutes of its July meeting and in the US Fed Chairman Powell is scheduled to speak and on Wednesday we get Euro Zone’s preliminary consumer confidence for July. On a packed Thursday, we get the preliminary PMI figures for July of Australia, Japan, France, Germany, the Euro Zone as a whole, the UK and the US while we also note the release of Japan’s chain store sales for June, Germany’s GfK consumer sentiment for August, UK’s CBI trends in industrial orders for July and CBI Business optimism for Q3, from the US the weekly initial jobless claims figure and Canada’s retail sales, while on a monetary level, we note from Turkey CBT’s interest rate decision and from the Euro Zone we highlight ECB’s interest rate decision and ECB President Lagarde’s subsequent press conference. On Friday we get from Japan, Tokyo’s CPI rates for July, UK’s retail sales for June, Germany’s July Ifo indicators and the US durable goods orders for June.

USD – Fundamentals to lead the greenback

On a monetary level, uncertainty seems to have eased a bit after US President Trump stated that he does not plan to fire Fed Chairman Powell. Nevertheless the US President continued to criticise the Fed Chairman for not favouring an extensive and fast easing of the bank’s monetary policy. Yet the release of June’s CPI rates, showing an intensification of the inflationary pressures in the US economy tends to suggest a possible hardening of the bank’s stance which in turn may result in rates remaining high for longer, thus providing some support for USD. We may see Fede Chairman Powell shedding more light on the bank’s intensions in his speech on Tuesday. A possibly more hawkish tone could provide support for the USD and vice versa.

On a macroeconomic level we have noted the acceleration of the CPI rates for June and it seems that Trump’s tariffs are coming into effect raising prices for consumers. Yet the PPI rates for the same month failed to follow and slowed down. Substantially stronger than expected financial data on Thursday tended to provide support for the USD, as they implied a boost both on the demand side of the US economy as well as on its production side, while the weekly initial jobless claims figure implied a tighter than expected US labour market. The higher-than-expected retail sales for the past month, tends to dissolve any doubts created by the PPI rates for June, In the coming week with few exceptions we have no high impact financial releases on the US calendar, hence we see may the influence of macroeconomic data easing.

On a fundamental level, we note the uncertainty about US President Trump’s tariff intentions, yet the market effect seems to have subsided. It may take substantial developments on the issue to take the markets by surprise and move them. On the other hand, US President Trump’s 1st of August deadline is approaching fast which tends to maintain uncertainty. On a fiscal level, we note that the US Senate passed the cuts in funding foreign aid and public broadcasting which is considered a win for US President Trump. We tend to maintain our worries for the “cut,cut,cut now and ask questions later” Republican approach as mentioned by Democratic Senate leader Schumer, which in turn may weigh on the US economic outlook and thus also on the USD.

Analyst’s opinion (USD)

“As mentioned, given the low number of high impact financial releases from the US on the calendar, fundamentals may lead the greenback in the coming week. Should a more hawkish tone be used by Fed policymakers we may see the USD gaining some ground. On a more fundamental level, the US President is expected to continue to be unexpected and could enhance uncertainty in the markets.”

GBP – June’s Inflation jumped unexpectedly

On a macroeconomic level, we note the unexpected jump of the UK CPI rates for June, beyond market expectations, both on a core as well as on a headline level. It’s characteristic that the headline rate accelerated at levels not seen in one and a half years and the release highlighted the intensification of inflationary pressures in the UK economy. On the other hand, the UK employment data for May were mixed, with the employment change figure reaching the stellar 134k while at the same time the unemployment rate ticked up to 4.7%. The rates and figures regardless of how unexpected they were, provided little movement for cable, while the pound continues to gain against the JPY and losing ground against the EUR for the week. In the coming week we may see the CBI releases getting some attention as could the preliminary PMI figures for July, with special interest of pound traders for the services sector. Should the indicators’ readings rise, implying a faster expansion of economic activity could in turn possibly provide some support for the pound. Also the release of the UK retail sales for June next Friday could weigh on the sterling should it show an even deeper contraction of the rate, as it could imply a wider weakening of the demand side of the UK economy.

On a fundamental level, we maintain our worries for the outlook of the UK economy. Especially on a fiscal level, the prospect of the UK Government proceeding with tax rate hikes and spending cuts could weigh on the UK economy. Furthermore, a possible tightening of the UK government’s fiscal policy, could ease inflationary pressures, yet at the same time that would mean hardship for the population. Should market worries intensify over the UK economic outlook, we may see them weighing on GBP.

On a monetary level, we note that the market’s expectations for BoE to proceed with a rate cut in its next meeting, remain even after the unexpected acceleration of the CPI rates for June. Furthermore GBP OIS imply that the market expects the bank to proceed with another rate cut, if not in the November meeting, then in December. Hence the market’s expectations continue to lean on the dovish side and should we see BoE policymakers actually expressing views that may be deemed as more hawkish than what the market expects, we may see the pound getting some support.

Analyst’s opinion (GBP)

“Financial releases may continue to feed interest in the coming week for the pound but monetary policy market expectations for BoE to continue ease its monetary policy further could weigh on the pound. Also on a fundamental level, worries for the UK macroeconomic outlook could weigh on the pound.”

JPY – House of Councillors elections make JPY nervous

On a fundamental level, the election of the House of Councillors in Japan on Friday may prove to be critical for the stability in the Japanese political scene. The ruling coalition is reported to be facing tough opposition in the elections for Japan’s upper House and may lose the majority. In such a scenario we may see the JPY weakening as the political outlook of Japan becomes uncertain. A possible win of the opposition may add more pressure on BoJ to keep rates unchanged in contrast to the bank’s efforts to tighten its monetary policy. It should be noted that the elections take place in the midst of US President Trump’s trade wars at which the US has targeted Japanese products entering US soil with higher tariffs. Trump’s tariffs tend to maintain the risks for growth of the Japanese economy on the downside thus any escalation could possibly weigh on JPY.

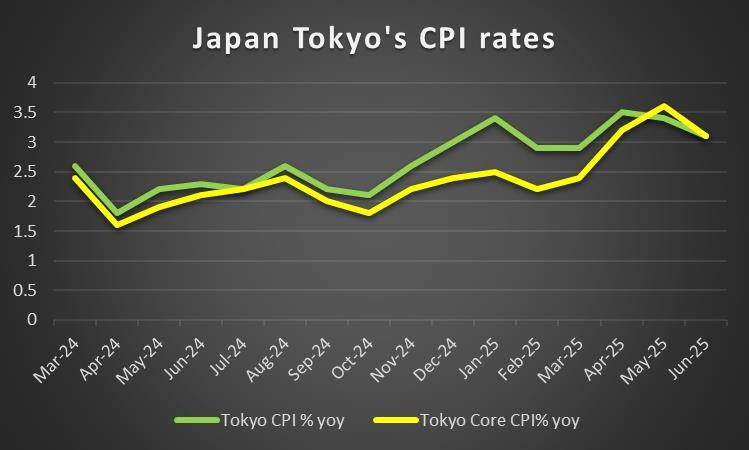

On a macro level, we note the trading surplus for June and the improvement of the machinery orders growth rate for May, yet the main release for the week, may have been June’s CPI rates. The slowdown of Japan’s CPI rates for the past month both at a headline as well as at a core level, which may be contradicting BoJ’s narrative and seems to have dissolved currently the market’s expectations for a rate hike at end of the year. In the coming week we note the release of the preliminary PMI figures for July but also note the release of Tokyo’s CPI rates also for July, which could serve as a preview for inflationary pressures in the Japanese economy as a whole.

On a monetary level, we note the market’s expectations for BoJ to keep its policy unchanged in its next meeting at the end of July and as mentioned above expects the bank ot maintain rates unchanged until the end of the year, implying that the market’s hawkish expectations have been erased. Analysts tend to note the possibility that the bank may revise upwards its forecast for inflation, which may renew the possibility of a rate hike at the end of the year. Yet the bank’s hawkish intentions seem to fail to clip the dynamic of JPY bears.

Analyst’s opinion (JPY)

“It should be noted that the Japanese currency is losing ground across the board for weeks now and JPY fundamentals seem to continue to feed the bears. We highlight the House of Councillors elections on Sunday as a key risk event for JPY. Also the second issue that could move the JPY would be Trump’s trade wars and a possible escalation of the tensions in the US-Japanese trade relationships could weigh on JPY .”

EUR – ECB’s interest rate decision in focus

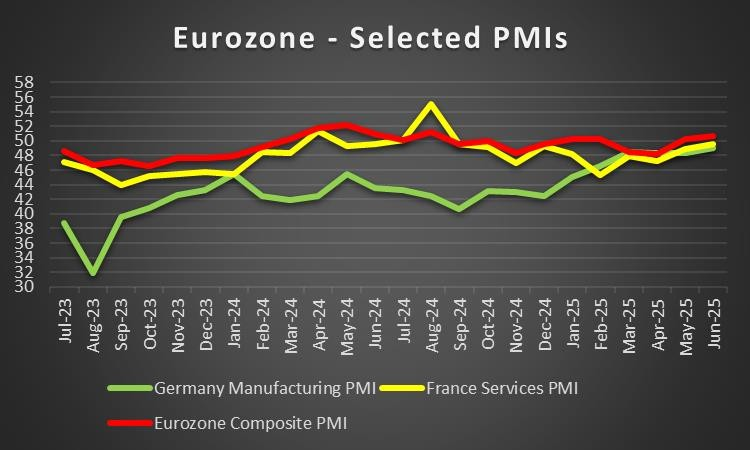

On a macro level for the EUR, we note the improvement of Germany’s ZEW indicators for July, a release that noted the improvement both on the outlook but also the conditions on the ground for the largest economy in the Euro Zone. We also note the verification of the acceleration of June’s HICP rate, which nevertheless remains at the ECB’s inflation target of 2.00%yy. In the coming week, we highlight the release of the preliminary PMI figures for July of the Euro Zone, Germany and France, with Germany’s manufacturing sector being the most interesting. Overall should we see the PMI indicators rising implying an improvement of economic activity in the Zone we may see the EUR getting some support as the release would brighten the macroeconomic outlook of the Zone.

The main event for EUR traders in coming week’s calendar may be ECB’s interest rate decision next Thursday. The bank is widely expected to remain on hold and currently EUR OIS imply a probability of 95.2% for such a scenario to materialise. EUR OIS also currently implying that the market expects the bank to cut rates one more time this year, in the October meeting. Hence we may say that a slightly dovish inclination of the market’s expectations exist and market attention may turn towards the bank’s forward guidance. Should the bank maintain a dovish tone in the accompanying statement and ECB President Lagarde’s following press conference, it could enhance the market’s expectations for further easing of the bank’s monetary policy and thus weigh on the common currency. On the flip side, a hawkish tone implying that the bank is prepared to keep rates at their current levels for longer, contradicting the market’s expectations we may see the EUR getting some support.

On a fundamental level we note the instability of the French political scene as French PM Bayrou is about to introduce measures improving productivity, including the scrapping of two national holidays. France is facing tough choices as the country is running a budget deficit of 5.8%, while the EU’s limit is 3% and the country’s national debt has surpassed its GDP. The issue tends to be considered as bearish for the common currency at the time and any intensification of the market’s worries about it could weigh on the EUR. Another issue that tends to tantalise EUR traders would be the US 30% tariffs on European products, announced by US President Trump. The EU Commission seems to be mulling countermeasures of EU tariffs on US products entering the EU, which are to focus on manufacturing products such as aircraft, a development that could adversely affect Boeing. For the time being the EU Commission seems to be pausing any thoughts for countermeasures as Germany’s Chancellor Merz is advising caution. In general any escalation in the frictions of the US-EU trade relationships could weigh on the EUR and vice versa.

Analyst’s opinion (EUR)

“We highlight the release of ECB’s interest rate decision as the key event for EUR traders in the coming week and a possible hawkish tone could provide substantial support for the EUR. On a fundamental level, the instability in the French political scene could weigh on the EUR as could also any intensification of the frictions in the US-EU relationships. On a macro level we may see the release of the preliminary PMI figures for July generating substantial interest among EUR traders.”

AUD – Easing of Australia’s employment market weighed on AUD

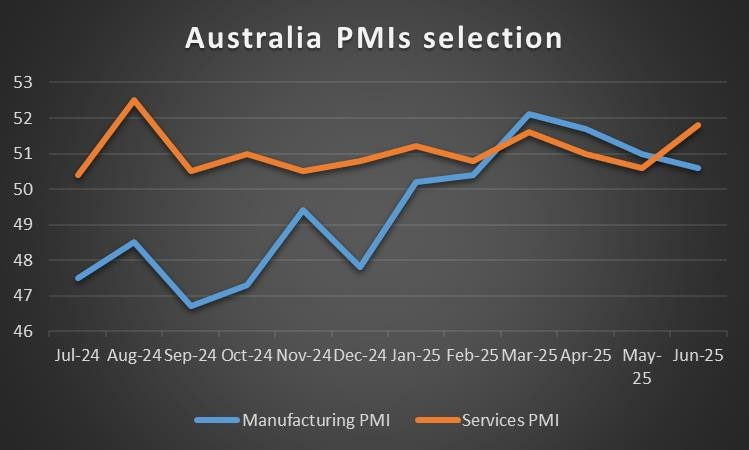

On a macro level, the main event for Aussie traders in the past few days was the release of Australia’s employment data for June. The employment change figure despite rising marginally, failed to reach the market’s expectations, negatively diverging substantially, while at the same time the unemployment rate rose to 4.3% if compared to May’s 4.1%. Overall the data implied an easing of the Australian employment market, which in turn may add pressure on the RBA to ease its monetary policy and understandably weighed on AUD. In the coming week we note the release of the preliminary PMI figures for July which could generate some interest among Aussie traders.

On a fundamental level, Trump’s trade war against China tends to weigh on the Aussie given also the close Sino-Australian economic ties. It should be noted that Chinese data releases over the past few days were mixed, as China’s trade surplus widened and the industrial output growth rate accelerated, yet the urban investment growth rate and retail sales growth rates slowed down implying an easing in economic activity of the chinese construction sector and the demand side of the Chinese economy, all being for June. Also the GDP rate for Q2 slowed down yet remained above 5%. Yet US President Trump’s trade wars tend to weigh on the Aussie given also the markets’ perception that the AUD is riskier asset in the FX market given its commodity currency nature.

On a monetary level, we note that despite RBA’s latest interest rate decision to remain on hold, the market seems to expect the bank to deliver three rate cuts until the end of the year, a signal of substantial dovish expectations for the bank’s policy. Coming Tuesday we note the release of RBA’s July meeting minutes and should the document show dovish intentions by the bank’s policymakers we may see the Aussie losing ground, while should they seem prepared to delay further any rate cuts, we may see the Aussie getting some support as the market may have to readjust its dovish expectations. We also note RBA Governor Bullock’s speech next Thursday where she is expected to provide more clarity for the bank’s intentions.

Analyst’s opinion (AUD)

“There are only few financial data from Australia that could affect the Aussie in coming week’s calendar. On a monetary level, a more dovish stance by RBA could weigh on the Aussie, as could any intensification of uncertainty at a global level.”

CAD – May’s retail sales of interest for Loonie traders

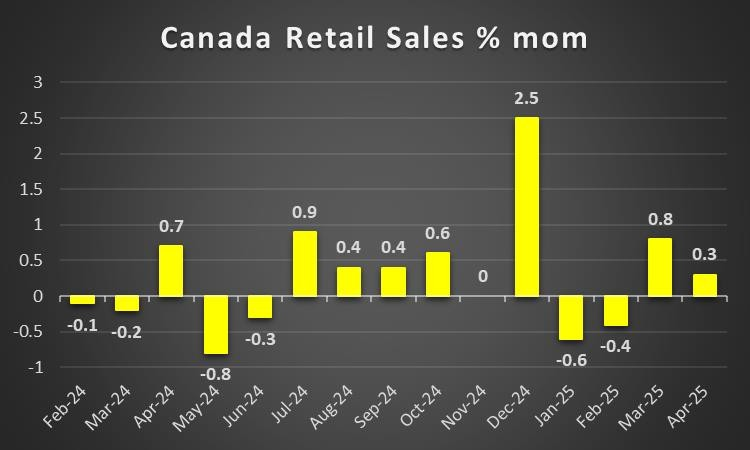

On a macroeconomic level, we highlight the acceleration of Canada’s CPI rates for June both on a headline as well as on a core level, with the headline rate being at tolerable levels and the core rate being a bit more worrisome. A positive surprise was the unexpected rise in the number of House starts for June and Canada’s business barometer for July. In the coming week, we highlight the release of Canada’s May retail sales. Should we see the rate accelerating we may see the Loonie getting some support as the release would imply a strengthening of the demand side of the Canadian economy. Also we note the release of June’s PPI rates and an intensification of inflationary pressures at a producers’ level could provide some support for the CAD.

On a fundamental level, the tensions in US-Canadian trade relationships tend to be a bearish factor for the Loonie. Given also the announcement of US President Trump that the US is to impose 35% tariffs on Canadian products beginning August 1st and Canadian PM Carney’s statement that any trade deal between the US and Canada is unlikely not to include any tariffs the issue becomes even more important and its characteristic that the Looney has been weakening against the USD over the past two weeks. Any intensification of the tensions in the US-Canadian trade relationships could weigh on the Loonie and vice versa. Also oil prices seem to be breaking a two week winning streak, which in turn may not weigh as such on the CAD yet in any case does not bode well for the Loonie, given Canada’s status as a major oil producing economy.

On a monetary level, the acceleration of Canada’s CPI rates for June tends to take out of the picture a possible rate cut by BoC in its next meeting, end of July, as the CPI rates advise caution. Yet the market currently expects the bank to proceed with a rate cut at the end of year. There seem to be no planned speeches by BoC policymakers in the coming week, yet should the market’s expectations for the Bank to maintain rates at the current stage for longer intensify, we may see the Loonie getting some support.

Analyst’s opinion (CAD)

“US-Canadian trade relationships may prove to be the main driver for the Loonie in the coming week, and any intensification of the tensions could weigh on the Loonie. On a macro economic level, we note the release of Canada’s retail sales for May and a possible acceleration of the rates could provide some support for the CAD.”

General Comment

Overall in the FX market, the USD may relent some of the initiative to other currencies, as the high impact financial releases stemming from the US are reduced. Nevertheless, US President Trump’s intentions and Fed Chairman Powell’s speech could maintain substantial interest of the markets in US developments. Yet we get a number of high impact financial releases and monetary policy events that may allow for a more balanced mix to emerge. As for US stock markets we note that the earnings season is in full swing and some bullish tendencies are being observed. In the coming week, we note the release of the earnings reports of Verizon, Coca-Cola, Philip Morris, Google’s Alphabet, Tesla, IBM, AT&T and Intel. As for gold’s price we note the continuation of tis sideways motion with its negative correlation with the USD being inactive currently.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.