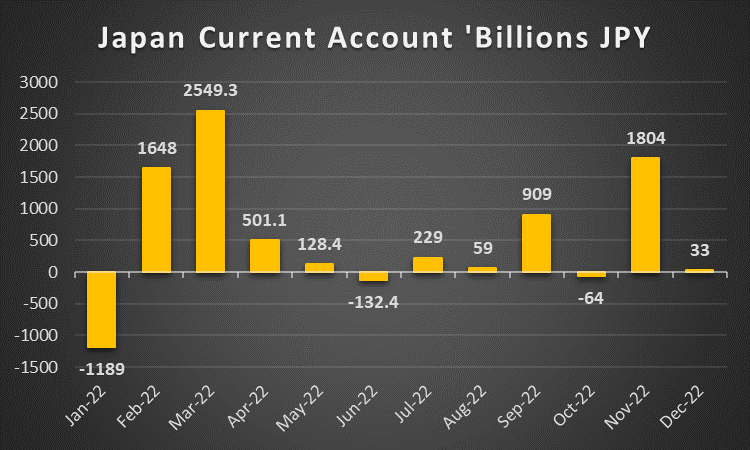

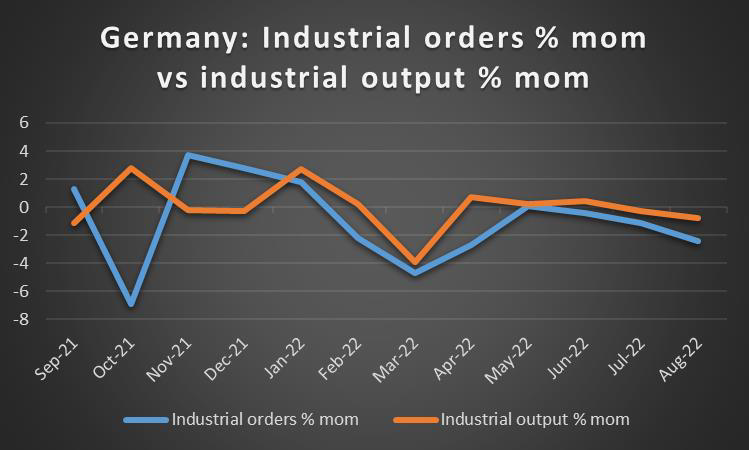

It’s been an interesting week with a number of releases and events swinging the markets and as it is about to end, we have a look at what next week has in store for the markets. On the monetary front, we note RBAs’ interest rate decision on Tuesday, while we also note the interest rate decisions of Canada’s BoC on Wednesday and Japan’s BoJ in Friday’s Asian session. Also on a monetary level, we highlight the testimony of Fed Chairman Jerome Powell before the Senate on Tuesday. As for financial releases, we would note on Monday the release of Switzerland’s CPI rate for February, Eurozone’s Sentix index for March and the US factory orders growth rate for January. On Tuesday we get Australia’s and China’s trade data for January and February respectively and Germany’s industrial orders growth rate for January. On Wednesday we make a start with Japan’s current account balance for January, Germany’s industrial output for the same month, Eurozone’s revised GDP rate for Q4 and Canada’s trade data for January. On Thursday we note the release of Japan’s revised GDP rate for Q4, China’s inflation metrics for February, Sweden’s GDP rate for January and the US weekly initial jobless claims figure. On Friday we get UK’s GDP and manufacturing output growth rates for January, Norway’s CPI rates for February, the Czech Republic’s CPI rates for the same month, Canada’s employment data for February and highlight the release of the US employment report for February with its NFP figure.

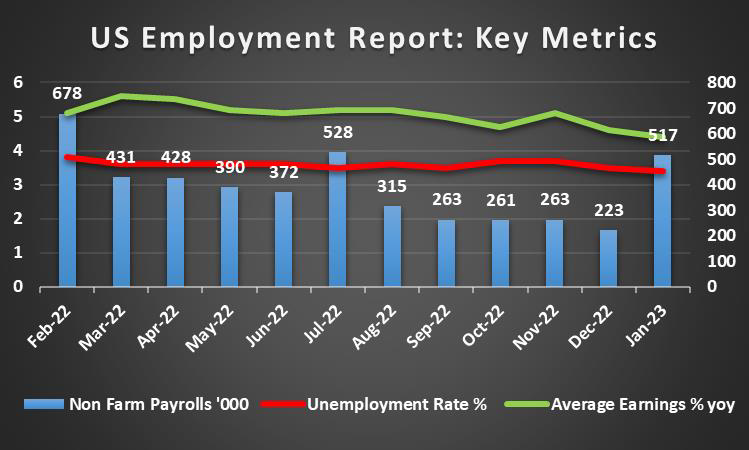

USD – US employment report to catch trader’s attention

The USD ended February higher against its counterparts yet seems to edge lower for the week, ending a winning streak of five consecutive weeks in the greens. On a monetary level, the market worries about the Fed’s hawkish intentions seem to remain ever-present and we note that Fed policymakers maintained their hawkish tone over the week. It’s characteristic that Minneapolis Fed President Kashkari called for more aggressive interest rate hikes in order to curb inflationary pressures in the US economy. On a macroeconomic level, we highlight the acceleration of January’s core PCE price index growth rate, which exactly underscored the persistent inflationary pressures in the US economy. On the production side, we note that the ISM manufacturing PMI figure improved for the month of February, yet rose less than expected, remaining below the reading of 50 and implying a continuous four-month contraction of economic activity for the US manufacturing sector. Also, there seemed to be a lack of confidence on behalf of US businesses to actually invest in the US economy as shown by the contraction of the durable goods orders growth rate for January. On the demand side of the US economy, we note the more pessimistic outlook on behalf of the average US consumer as implied by February’s consumer

confidence indicator. Overall the financial data tend to maintain our worries for the US economy, given the Fed’s hawkish intentions. In the coming week, we note Fed chairman Powell’s testimony before Congress, while we highlight the release of the US employment report for February on Friday. Should the data show a tight US employment market, we may see the USD getting some support as the Fed’s hawkish stance could sharpen even further.

GBP – GDP rates eyed at the end of the week

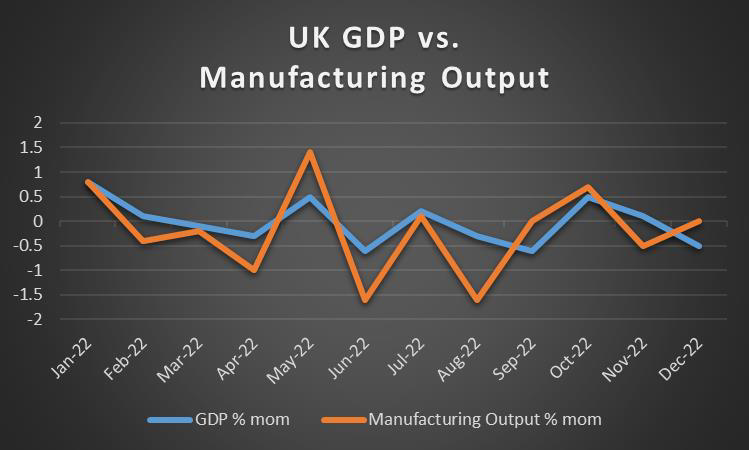

The pound is about to end the week near the same levels it began against the USD and JPY yet is losing ground against the EUR. On a fundamental level, we highlight the agreement made between the EU and the UK. As was expected, UK PM Sunak with EU chief Von der Leyen sealed a decisive breakthrough in the Brexit agreement, regarding Northern Ireland’s trading agreements. The “Windsor Framework” as it was called by UK PM Sunak, would include a lowering of the trade barriers between Northern Ireland and Great Britain, allow for the European Court of Justice to maintain oversight, Northern Ireland to have a “veto” on new EU laws and key taxation rules are to be amended, while the approval of the deal is still pending with Northern Ireland’s Unionist Party (DUP) playing a key role. Overall, the deal seems to be getting support and tends to highlight the simplification of the trading arrangements of the UK with the EU, which in turn supported the GBP but also in general could provide some support for UK assets. On a macroeconomic level, we note that the nationwide house prices growth rate marked another contraction, a result possibly also of BoE’s monetary policy tightening. In the coming week we expect the attention of pound traders to turn towards the release of the GDP rates for January and should there be an acceleration we may see the pound getting some support. On a monetary policy level, we highlight the comments of BoE Governor Bailey as he practically stated that the bank may have reached its terminal interest rate, yet that would come into contrast with BoE MPC member Catherine Mann, who supported the idea that more rate hikes are necessary. Overall, the struggle within BoE’s balance of power seems to be shifting slowly but steadily away from the hawkish side, which could weaken the pound.

JPY – BoJ’s interest rate decision in focus

JPY is remain relatively stable against the USD and JPY for the week and is clearly losing ground against the EUR. We note on a macroeconomic level, that the preliminary industrial production growth rate suffered a substantial contraction for January, far wider than the market’s expectations which tends to intensify our worries for Japan’s economic outlook, also given the importance of the manufacturing sector for the Japanese economy. Yet the demand side seems to remain robust, given that the retail sales growth rate for the same month accelerated beyond market expectations, thus may continue feeding inflationary pressures, something that was evident in the release of Japan’s headline and core CPI rates for January, last Friday. On the contrary, the slowdown of Tokyo’s CPI rates for February tend to suggest an easing of inflationary pressures. Please note that in the coming week, a number of high-impact financial data is to be released and could provide more clarity. On a monetary level, we highlight the release of BoJ’s interest rate decision on Friday’s Asian session. The bank is expected to remain on hold, keeping rates at -0.10%, with no surprises being probable. It’s characteristic that currently, JPY OIS imply a probability of 90% for such a scenario to materialise. Yet the bank, given the change of leadership it is about to undergo, please bear in mind that it’s the last meeting before Mr. Ueda and his team take over, may be inclined to surprise the markets. In such a case, we may see BoJ tweaking its ultra-loose monetary policy once again by widening its Yield Curve Control bands, which could be a hawkish surprise for JPY traders and could provide substantial support for the Yen. Yet the base scenario for now, is that the bank is to remain substantially dovish in its accompanying statement once again which could weigh on JPY somewhat.

EUR – ECB’s hawkishness got a stimulant

EUR is about to end the week stronger against the USD, JPY and GBP, in a sign of a broader strength. On a macroeconomic level, we note that Eurozone’s economic sentiment for February failed to improve, while the area’s unemployment rate ticked up for January, both being categorised in the negatives for Eurozone’s economy. The main release, that shook the common currency was the preliminary HICP rates for February. In France, Germany and Spain, we saw an acceleration of inflationary pressures that inevitably prevented Eurozone’s headline rate to slow down substantially on a year-on-year level. It’s characteristic that the

area’s preliminary core HICP rate for February, which excludes food and energy prices, accelerated beyond market expectations reaching new all-time highs which seems to come in direct contradiction with ECB’s chief economist Lane’s comments that the bank has started winning the war on inflation. On a monetary level, given the acceleration of Eurozone’s inflationary pressures, we may see its hawkishness being galvanized. It was characteristic that ECB President Christine Lagarde stated on Thursday that more rate hikes are possible after the March meeting. Such intentions were also expressed by Germany’s Bundes Bank (BuBa) President Nagel the day before. The statements are locking in a 50-basis points rate hike in the bank’s March meeting and tend to foreshadow more 50-basis points rate hikes to come. Currently, the market seems to expect the bank to reach a terminal rate of 4% by mid-June. Should the bank proceed with more substantial rate hikes beyond March, we may see the possible adverse effects on Eurozone’s economy widening.

AUD – RBA’s interest rate decision in the epicenter

AUD seems about to edge just a bit lower against the USD for the week. On a macroeconomic level, we note that we had some positive news from Australia, as the retail sales growth rate for January, was able to escape the negative territory and accelerated beyond market expectations, showing a strong demand side of the Australian economy, while the current account balance for Q4, was able to get rid of the minus sign and widen substantially, implying that the Australian economy benefited from its interaction in the international payment system. On the other hand, we note that the Australian economy grew at a slower pace than expected for Q4, which tends to weigh and may also cause second thoughts among RBA policymakers regarding the hawkish intentions. We also note the wide contraction of the building approvals growth rate, which may have also been a result of RBA’s monetary policy tightening. On the monetary level, we note RBA’s interest rate decision on Tuesday’s Asian session. The bank had already expressed its intentions for further rate hikes and the market expects the bank to deliver a 25 basis points rate hike in its next meeting. Characteristically, AUD OIS imply a probability of 75.3% for the bank to raise its cash rate from 3.35% to 3.60%. Should the bank actually deliver the expected rate hike we may see the Aussie getting some support as the other 25% of the OIS, expecting the bank to remain on hold, will have to reposition itself. Yet in such a case attention is expected to fall on RBA Governor Lowe’s accompanying statement. Should the bank maintain a confident, hawkish tone, foreshadowing more rate hikes to come, we may see the bullish effect on AUD intensifying as the market’s expectations for the bank’s hawkish intentions are to be verified. On a more fundamental level, news from China, seem to be pretty good as China’s reopening supports the economic activity of the manufacturing sector. It was characteristic that both the NBS and Caixin PMI figures rose above 50, with the NBS reading surpassing 52 and showing that economic activity expanded at the fastest pace in more than a decade, raising hopes that the positive effect could overspill to the global economy. Attention now turns also toward China’s National People’s Congress annual legislative meeting and any measures that are to be taken to boost the Chinese economy in the current year could improve the market sentiment further.

CAD – BoC to remain on hold?

The CAD seems about to edge slightly lower against the USD for the week. On a macroeconomic level we note that Canada’s GDP rate slowed down beyond market expectations for Q4 and on a year-on-year level reached the stagnation levels of 0% for Q4, while on a month-on-month level, it even ticked down to the negatives. The release could enhance BoC’s intention to pause rate hikes. Hence, on the monetary front, we highlight BoC’s interest rate decision on Wednesday. The market expects the bank to remain on hold, keeping its rate at 4.5% and it’s characteristic that CAD OIS imply a probability of 97.4% currently, for such a scenario to materialize. Should the bank remain on hold as expected we may see the market’s attention turning towards the accompanying statement and the document is expected to be scrutinized, in search of further clues regarding BoC’s intentions. Should the document solidify the market’s expectations that the bank has reached its terminal level of interest rates and no more rate hikes are to be expected, we may see the CAD slipping and vice versa. On a more fundamental level, we also highlight the possible effect that oil prices may have on the Loonie. WTI prices for the week seem to be edging higher. On the one hand, the market’s anticipation for a widening of economic activity in China is expected to boost oil demand and thus may have a bullish effect on oil prices. On the other hand, though, the US oil market is still characterised by a slack, which allows for its oil reserves to rise even further and tends to keep oil bulls at bay. Hence we would highlight these two issues as the main ones to keep an eye out for in the next week regarding oil. Should oil prices get additional support we may see the Loonie benefiting as well. Also, we highlight at the end of the week Canada’s employment data for February and should the release show a tight employment market, we may see the CAD gaining some ground.

General Comment

Overall and as a closing comment, we expect the USD to regain some of the initiative over other currencies, given that the frequency and gravity of US releases and events increases. We may see the influence of the greenback being on the rise, yet that may also increase volatility. Nevertheless, there are still a high number of high-impact financial releases, stemming from outside the US which may allow for other currencies to steal the spotlight from the USD at certain points during the week and thus create a more balanced mixture of trading opportunities. At this point, we would like to note that US yields rose substantially over the week with the 2-year yield surpassing 4.80%, a level not seen since 2007. Should the US yield curve inversion steepen further, we may see the USD enjoying further safe haven inflows. US stock markets on the other hand, seem about to edge a bit lower for the week. The market worries for a possible overtightening of the Fed’s monetary policy tended to weigh on US stock market sentiment and thus put them under pressure. In the coming week, we expect investors to continue to navigate through the Fed’s intentions and the earnings releases due out. On the other hand, we have to note that most of the high-profile companies have already released their earnings reports and the number of earnings releases due out next week as such, is expected to be reduced in comparison to the past weeks. Thus their effect on US stock markets and the general market sentiment is expected to slowly start fading away. As for gold’s price, we note that the precious metal’s price was able to halt the downward motion characterizing it over the past two weeks. The negative correlation between gold and the USD seems to be maintained despite its disproportionality, hence we highlight the testimony of Fed Chairman Powell before Congress next week as well as the release of the US employment data for February on Friday as key events for the shiny metal’s direction.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.