The week is about to draw to a close and we open a window to what next week has in store for the markets. On a monetary level, we make a start on Tuesday with BoJ’s interest rate decision and continue with Bank of Canada on Wednesday and on Thursday we have a bonanza of interest rate decisions, from Norgesbank, the Central Bank of Turkey and the ECB. As for financial releases, after a relatively quiet Monday, we note on Tuesday the release of Australia’s Business indicators for December, Eurozone’s preliminary January consumer confidence and New Zealand’s CPI rates for Q4. On Wednesday, we note the release of the preliminary PMI figures of Australia, Japan, France, Germany, the Eurozone and the US for January, while we also get Japan’s trade data for December. On Thursday, we get Germany’s January Ifo indicators, Canada’s Business Barometer for January, and from the US we get December’s durable goods orders for December and weekly initial jobless claims figure, while we highlight the release of the preliminary US GDP advance rate for Q4. Finally, on Friday, we note the release of Japan’s Tokyo CPI rates for January, Germany’s GfK consumer sentiment for February and from the US the consumption rate and the Core PCE Price index growth rates, both being for December.

USD – US GDP rate to be the highlight

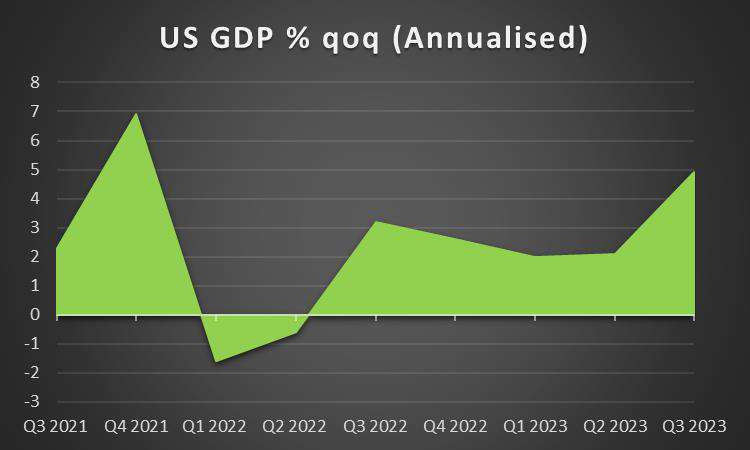

The USD is about to end the week, well in the greens against its counterparts. On a macroeconomic level, the US manufacturing sector seems to be suffering, given the contraction of economic activity implied by the release of the NY and the Philadelphia indexes for January. Also, the industrial production growth rate for December slowed down showing anemic growth for the sector. Furthermore, the construction sector also seems to have suffered a contraction of economic activity in the past month given the drop of the number of housing starts and building permits. On the other hand, the retail sales growth rate for December accelerated beyond market expectations, implying a resilience of the demand side of the US economy, while it may be also able to feed inflationary pressures. In turn, given the resilience of inflationary pressures in the US economy, the Fed may more decisively maintain rates at their current levels for a longer period of time than what the market expects. Please bear in mind that currently the market expects the bank to deliver six rate cuts in the current year starting from the March meeting onwards. Yet Fed policymakers tend to repeat the message that the bank may opt to delay any rate cuts. It’s characteristic that Fed Board Governor Waller was quoted stating that “however, … I see no reason to move as quickly or cut as rapidly as in the past”. Overall the continuous persistence of the Fed policymakers that rate cuts should be delayed beyond the market’s expectations seems to provide some support greenback. On a more fundamental level, we may see the wider uncertainty on a global level, providing some support for the USD yet that seems to remain at weak levels for now and we highlight as the next big test for the USD the release of the preliminary GDP rate for Q4 2024.

GBP – Fundamentals to lead the way

The pound is about to end the week lower against the USD yet higher against the JPY and EUR. On a macroeconomic level, we note the acceleration of the House Prices growth rate for January as good news for the UK real estate sector. Furthermore, we also note the release of UK’s employment data which tended to provide some support for the pound on Tuesday. For November, the unemployment rate remained stable at 4.2% yet the employment change figure, jumped beyond market expectations reaching 73k. Also, we note that the claimant count for December dropped while as a word of caution please bear in mind that Her Majesty’s Revenue and Customs Payroll change fell deeper into the negatives. Overall though the UK employment data tended to imply a relative resilience of the UK employment market, which may feed inflationary pressures in the UK economy. On the inflationary front, we note that the headline CPI rate for December, unexpectedly accelerated to 4.0% yoy if compared to 3.8% yoy in November, despite the downward tendencies of the PPI rates for the same month. On a monetary level, the acceleration of the CPI rates is expected to add pressure on BoE to maintain rates at high levels for a longer period, a scenario that may also be allowed by the tighter-than-expected UK employment market. Yet the market sees that the bank may be forced to expedite any rate cuts given the bleak economic outlook of the UK. It should be noted that the market given the acceleration of the CPI rates for December prices in 4 rate cuts to be delivered by BoE in 2024, starting from June onwards. As for next week, given the low number of high-impact financial releases expected from the UK we may see fundamentals leading the way for the sterling.

JPY – BoJ’s interest rate decision in focus

JPY is about to end the week in the reds against the USD, EUR and GBP in a sign of broader weakness. On a fundamental level, we note the relative uncertainty in geopolitics, which may provide some inflows for the Yen, should market worries intensify in the coming week, given its status as a safe haven. On a macroeconomic level we note that the machinery orders growth rate for November marked a wide contraction, implying a lack of confidence on behalf of Japanese businesses to actually invest long term in the Japanese economy. On the inflationary front, corporate goods prices for December slowed down on a year-on-year level, maybe not as much as was expected, while the CPI rates for the same month also slowed down both on a headline as well as on a core level. The slowdown of the CPI rate tends to justify BoJ’s hesitancy to normalise its ultra-loose monetary policy settings, currently in place. Hence as the main event for JPY traders in the coming week, we highlight the release of BoJ’s interest rate decision on Tuesday. The bank is widely expected to remain on hold at -0.10% and currently JPY OIS imply a probability of 92.6% for such a scenario to materialise. We tend to expect the bank to maintain its dovish tone given the slowdown of the CPI rates which in turn may weaken JPY further. To expect a tweak in the bank’s dovish tone, we would require a relative stabilisation of the CPI rates in order to show that it is sustainable, something that does not seem to be the case, at least not yet. On the other hand, the market expects the bank to deliver its first rate hike in decades in the June meeting, and should the bank want to start preparing the markets for such a scenario, we may see BoJ allowing for some hawkish innuendos to escape.

EUR – ECB’s interest rate decision in the epicenter

The EUR is about to end the week lower against the USD and GBP, yet gains ground against the JPY. On a fundamental level, we tend to maintain our worries about the political outlook of Germany, given the protests of farmers but also the rise of the AfD. The recent scandal of a conspiracy for the deportation of two million immigrants may have been ringing the alarm for Germany politically, yet the far-right movement seems to remain strong and the elections are nearing. On a macroeconomic level, we make a start by noting that Eurozone’s industrial production suffered an even deeper contraction for November, being another signal of the sufferings of the sector. Furthermore, the outlook for Germany tended to be more optimistic in January, yet conditions on the ground for the largest economy in the Eurozone, seem to have deteriorated slightly. We also note that the acceleration of the Eurozone’s HICP rate for December was confirmed, a scenario that may force the ECB to keep a harsher rhetoric in its coming meeting on Thursday. The bank is widely expected to remain on hold keeping the refinancing rate at 4.5% and the deposit rate at 4.00%. It’s characteristic that EUR OIS imply a probability of 96% for such a scenario to materialise, which more or less tends to set the interest rate part of the decision as an open and shut case. Market focus is then expected to shift towards the release of the accompanying statement and a bit later towards ECB President Lagarde’s press conference. Please note that the market expects the bank to deliver six rate cuts in the current year, starting from April onwards. Yet, given President Lagarde’s recent statements it seems that the bank is orienting itself towards starting to cut rates by the summer, but at the same time seems ready to take its time to proceed with the first rate cut, as it wants to be more certain that inflation has returned to target. On the other hand, the Eurozone is facing a recession, which in turn increases the pressure on the bank to start cutting rates rather sooner than later. It will require a very fine balance in the accompanying statement and President Lagarde’s press conference in order not to affect the common currency and it may be difficult for such a fine balance to be achieved on Thursday. Should the bank seem to be in more of a hurry to start cutting rates, we may see the EUR weakening and vice versa.

AUD – Market sentiment to move the Aussie

AUD is about to end the week lower against the USD for a third consecutive time and we note that this week’s drop seems to be the widest of the three. On a macroeconomic level, we note that Australia’s employment data for December disappointed Aussie traders as despite the unemployment rate remaining unchanged at 3.9%, employment change fell deeper in the negatives, reaching -65.1k implying another crack in the tightness of the Australian employment market. The release could milden any hawkish tendencies of the RBA and for the time being, AUD OIS imply that the market seems to be pricing in only one rate cut of 25 basis points in 2024 and that is to be delivered in the fall. On a deeper fundamental level, we note the release of the Chinese data in the past few days which was encouraging for Aussie traders. It’s characteristic that China’s GDP rate for Q4 accelerated, maybe a bit less than expected, yet nevertheless indicated that the Chinese economy grew at a faster pace than in Q3. At the same time, we had better-than-expected growth rates for China’s industrial output and Urban investment for December, which could support further growth in the coming quarter. On the other hand, the demand side of the Chinese economy seems to be easing, forcing Chinese factories to increase their dependency on exports. On an even deeper fundamental level, we note that in Taiwan, DPP won the presidential elections, yet failed to secure a majority in the legislative body, overall though China seems not to intend an escalation in their relationship currently, which may have been another positive.

CAD – BoC to stand pat

The Loonie is losing ground against the USD for the third week in a row. On a macroeconomic level, the housing starts figure for December came in higher than expected at 249.3k versus the expected figure of 243k, which could temporarily aid inflationary pressures. Yet, such an effect does not appear to have aided the Loonie, as it is a secondary indicator compared to the CPI rates. We note that December’s CPI rates were released on Tuesday. The release tended to send out mixed signals as the headline CPI rate accelerated, yet at a core level, inflationary pressures tended to ease. We note that the CPI rates are within the bank’s target range of 2.00±1.00%, at a core level, yet we also expect the bank to require more and more consistent evidence that inflationary pressures have eased further. On a monetary level, we note BoC’s interest rate decision which is set to be released next Wednesday, with CAD OIS currently implying an 84% probability for the bank to remain on hold. A view we tend to agree with, yet we would go as far as to hypothesize that the bank in its accompanying statement, may adopt a more hawkish tone and could warn the market participants that a single financial reading may not be convincing, which in return could support the Loonie. The market though is currently expecting the bank to deliver four rate cuts in the current year. Should the bank intend to start preparing the markets for a possible easing of its monetary policy, we may see it adopting a less hawkish tone, which in turn may verify the market’s suspicions and thus weaken the CAD. On a fundamental level, we note that oil prices remained near the same levels as the week began, yet a possible rise in oil prices, possibly due to the tensions in the Middle East and the Red Sea, may provide some support for the CAD in the coming week.

General Comment

In the coming week, we expect the USD to maintain the initiative over other currencies in the FX market mostly due to the release of the preliminary US GDP Rate for Q4. Yet given the interest rate decisions scheduled next week we may see the EUR, JPY and CAD escaping the USD’s sphere of influence at some points. Furthermore, the preliminary PMI figures may also provide a chance for some currencies to set their course. US stock markets seem to be sending mixed signals and some signs of hesitation, as the Fed’s message for a lower number of cuts starting at a later stage, slowly sinks in. Releases of earnings reports are still expected to keep the interest of equity traders alive and in the coming week we note the earnings reports of General Electric (#GE), Netflix (#NFLX), Johnson & Johnson (#JNJ), Procter & Gamble (#PG), Verizon (#VZ), Lockheed Martin (#LockheedMT) on Tuesday, Tesla (#TSLA), Louis Vuitton (#LVMUY), AT&T (#T), IBM (#IBM), Xerox (XRX) on Wednesday, Intel (#INTC), Visa (#V), Starbucks (#SBUX) on Thursday and on Friday Caterpillar (CAT), American Express (AXP), Colgate-Palmolive (CL). Furthermore, we note that the Fed’s message seems to have pushed US yields higher in the past week, understandably weighing on US equities markets and gold’s price, given also that the precious metal is not interest-bearing in contrast to US bonds. It should be noted that the negative correlation of the USD to gold’s price was maintained in the current week and should the USD strengthen further, we may see the gold’s price searching for lower grounds.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

إخلاء المسؤولية:

لا تُعد هذه المعلومات نصيحة استثمارية أو توصية بالاستثمار، وإنما تُعد تواصلاً تسويقيًا. لا تتحمل IronFX أي مسؤولية عن أي بيانات أو معلومات مقدمة من أطراف ثالثة تم الإشارة إليها أو الارتباط بها في هذا التواصل.