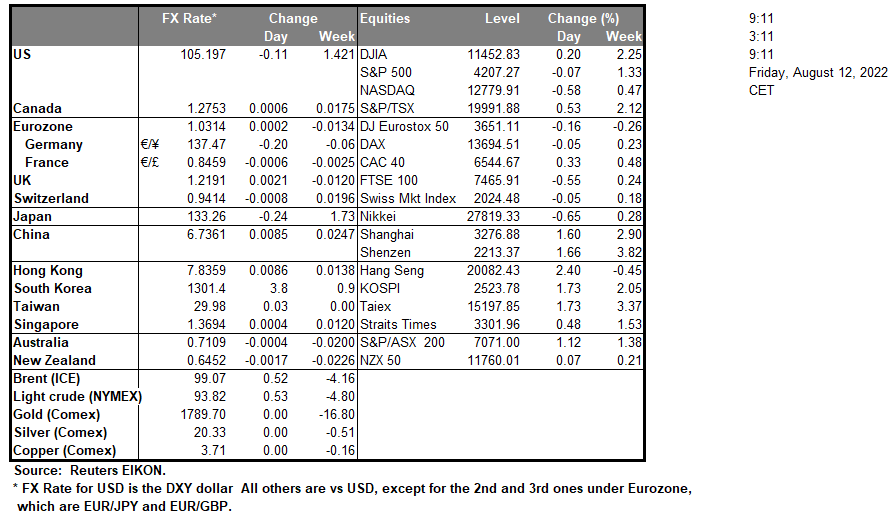

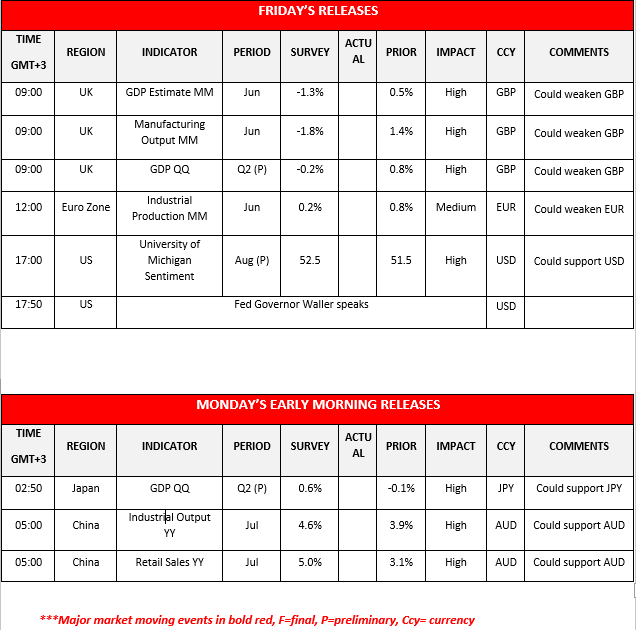

The sterling was roughly flat yesterday against the US dollar but fell however against the euro portraying a clearer picture on the state of UK’s economy ahead of the growth reports. Today we expect the release of the UK’s preliminary quarter on quarter GDP rate for Q2 and the month-on-month GDP rate for June. The quarter-on-quarter GDP rate is expected to drop to -0.2% from 0.8% as well as the June’s month on month GDP rate which is expected to drop to -1.3% from prior 0.5%. Given the above estimates, should the actual rates meet their respective forecasts we may see GBP weakening, giving an end to its short-lived price appreciation against the dollar for the past month. With the results indicating a slump into the negatives both on quarter on quarter and month on month basis, not only highlights the fragility of the UK’s economy but also validates concerns and shortens the time horizon of an impending recession, rather sooner than later. Bank of England’s Chief economist Huw Pill in an interview previously this week acknowledged that hiking interest rates to fight inflation will slow growth, arguing that it is a necessary step towards stabilizing the economy over the long term. With inflation hitting a 40 year-high the BoE is determined to put a stop to the upward spiral of prices, risking in the process, tipping the economy into a recession. Bank of England feels the pressure to keep up with rate hikes as it fears it may fall behind, as it plays catch up with the rate of which the Fed is moving forward. In our view, not only BoE also other central banks around the world are caught lagging behind and we believe that efforts towards synchronisation with the US are to come. On another note, we also would like to highlight China’s year on year Industrial Output and year on year Retail Sales growth rates both for July, to be released on Monday’s early morning session. Expectations for the Industrial output growth rate, point to an increase to the 4.6% from 3.9% level, and Retail sales expectations indicate an increase to 5% from 3.1%. Should the actual rates match the forecasts, we may see the Aussie getting a boost due to the close interlinks of trading activity between China and Australia and given that the release could imply an acceleration of the expansion of economic activity for the Chinese industrial sector and at the same time a rather robust internal market, both of which could boost Australia’s exports.

GBP/USD retraced after it briefly challenged the 1.2276 (R1) resistance level, failing to advance further. We hold a sideways bias for the future price action for cable as we observe an ascending triangle pattern being formed. Should the bulls take over, we may see the price action breaking above the 1.2276 (R1) line and move close to the 1.1937 (R2) level. Should the bears reign over, we may see the break below the ascending trendline, the break of the 1.2069 (S1) and a move near the 1.2378 (S2) level.

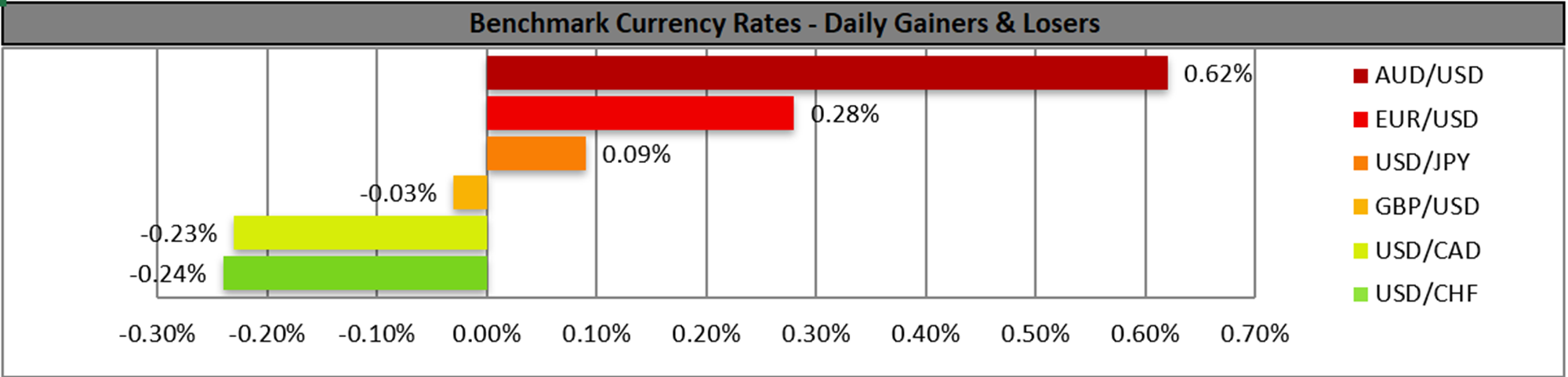

AUD/USD extended its uptrend, initiated since the 14th of July and is currently approaching the 0.7132 (R1) resistance line. We hold a bullish outlook bias for the continuation of the Aussie dollar price action. Supporting our case is the RSI indicator which shows the positive momentum with a reading of 65, edging closer to the 70 overbought threshold. Should the buyers pile in, we may see the price break above the 0.7132 (R1) level and head for the 0.7197 (R2) level. Should sellers overwhelm, we may see the break below the ascending trendline, the break of the 0.7034 (S1) base and move near the 0.6962 (S2) support level.

Other highlights for the day:

Today we also highlight the releases of, UK’s MoM Manufacturing Output for June, Eurozone’s MoM Industrial production for June and for the US the University of Michigan consumer Sentiment and Fed Governor Waller’s speech. During Monday’s Asian session we note Japan’s QoQ GDP rate for Q2.

GBP/USD H4 Chart

Support: 1.2069 (S1), 1.1937 (S2), 1.1778 (S3)

Resistance: 1.2276 (R1), 1.2378 (R2), 1.2483 (R3)

AUD/USD H4 Chart

Support: 0.7034 (S1), 0.6962 (S2), 0.6886 (S3)

Resistance: 0.7132 (R1), 0.7197 (R2), 0.7268 (R3)

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

إخلاء المسؤولية:

لا تُعد هذه المعلومات نصيحة استثمارية أو توصية بالاستثمار، وإنما تُعد تواصلاً تسويقيًا. لا تتحمل IronFX أي مسؤولية عن أي بيانات أو معلومات مقدمة من أطراف ثالثة تم الإشارة إليها أو الارتباط بها في هذا التواصل.