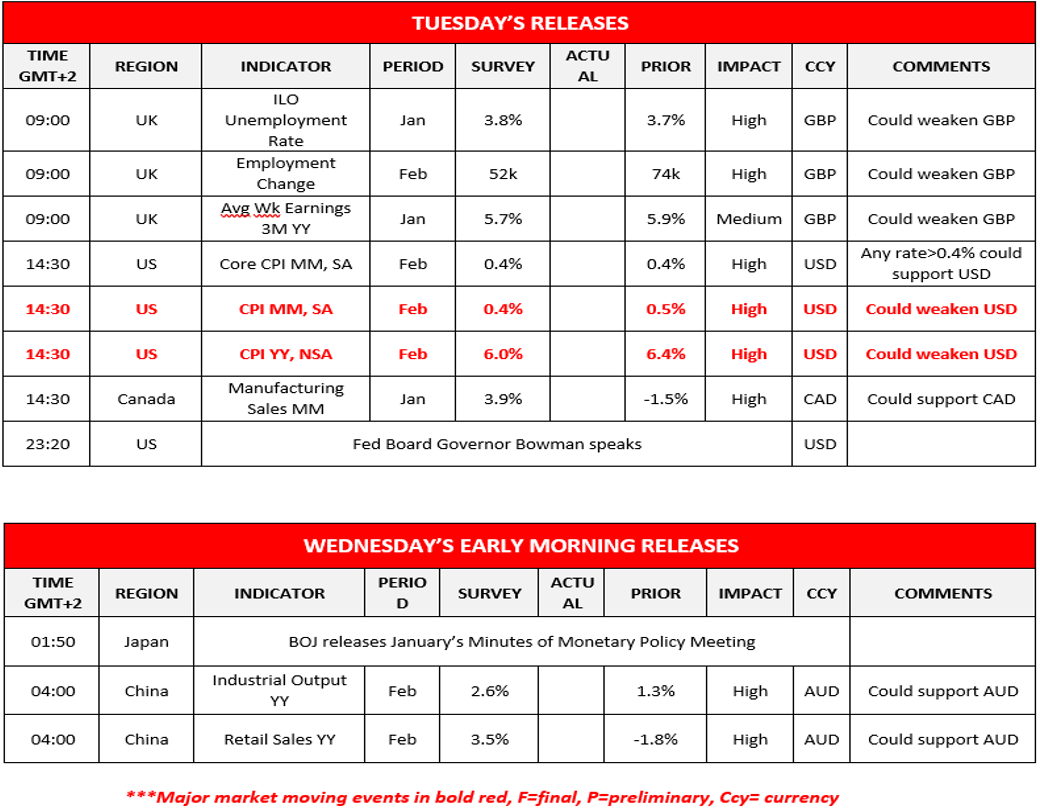

Looking past the Silicon Valley Bank debacle, which continues to ravage the banking sector, the markets will be forced to take crucial incoming inflation data later today. According to forecasts both the mom and yoy CPI rates for February to decelerate and if so, we may see the weakness in the dollar extending further. More specially, the mom CPI rate is foreseen to ease to 0.4%, down from 0.5% of the prior month. Likewise, the yoy CPI rate is also seen easing to 6.0% when compared to the 6.4% rate of the prior month. The results could in a sense come in line with the recent shift in market expectations which become increasingly complacent that the Fed will not pursue more hikes. Market consensus radically changed since last week. Following Powell’s comments the market shifted their outlooks reflecting the hawkish prospects of the Fed, once the door for a larger magnitude hike sprung open. As a result, we saw the market shifting projections and bracing for 50 basis points. As soon as the SVB headlines hit however the market quickly downgraded their projections for the 50 basis points hike and opt for a 25 basis points one as initially expected. After the weekend and the announcement that the Fed, FDIC and the Treasury department decided to step in and ensure that depositors would get back their money we saw a complete 180 degree turn from the market, dismissing the 25-basis points scenario, at least for the time being, and end up pricing in that the Fed would stay on hold in the February meeting.

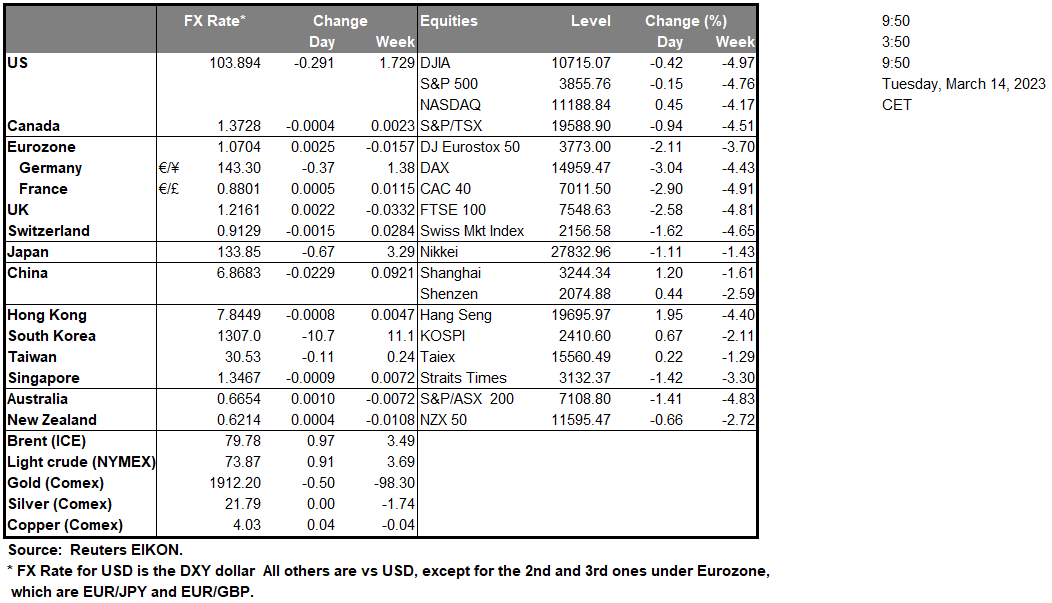

Bond yields were on a free fall mode for the past four days, with the US 2-year yield nose-diving in an extraordinary fashion by more than 100 basis points, from 5.07% peak formed last Tuesday and currently sits below the 4% level. Benchmark US 10-year treasury yield eased towards the 3.5% mark, down by more than 50 basis points for the same period. Signature bank, First Republic, Western Alliance Bancorp, Zions Bancorp and other small-to-medium sized banks, all recorded tremendous declines yesterday, with investors taking action to their hands as worries for a possible spill over scatter in the market. Biden says he will seek stronger regulations for banks, however analysts point out the growing divide between Republicans and Democrats in Congress, will most likely put extra hurdles ahead of the President’s plans. Biden alongside Secretary of Treasury Yellen underscored that SVB is not being bailed out and reassured that creditors will receive their deposits. Gold has gone supernova during yesterday’s session, capitalizing on the huge move into treasury yields and propelled higher by contagion fears, easily clearing past the $1900 level. Since the announcement of SVB’s fallout the precious pivoted from near its $1800’s lows, taking off and soaring by more than $100 dollars within three sessions, recording an incredulous 5.5% gain.

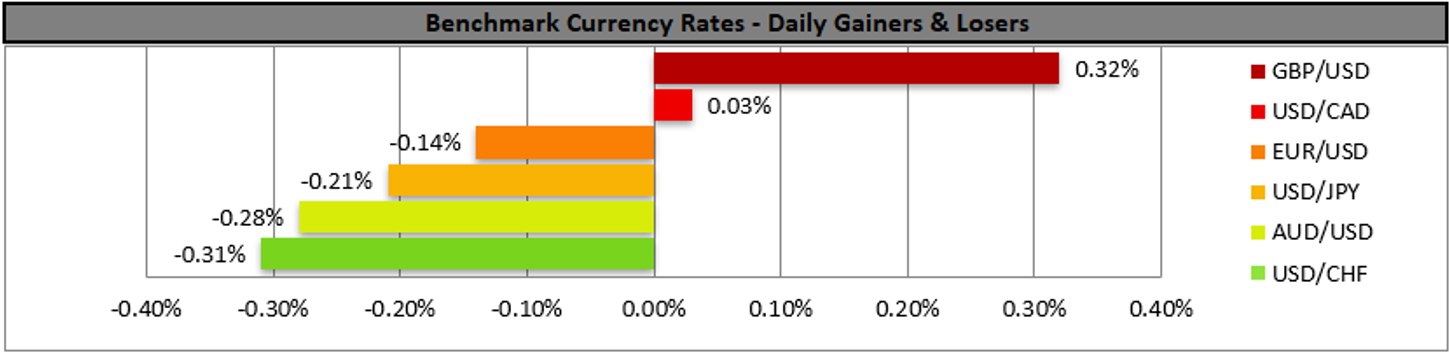

GBP/USD rose breaking the 1.2115 (S1) resistance line, now turned to support. We tend to maintain a bullish outlook for the pair as long as it remains above the upward trendline incepted since the 10th of October. Should the bulls maintain control over the pair, we may see cable breaking the 1.2270 (R1) resistance line and aim for the 1.2465 (R2) level. Should the bears say enough is enough and take over, we may see GBP/USD reversing course, breaking the prementioned upward trendline, the 1.2115 (S1) support line and aim for the 1.1925 (S2). USD/JPY shows some signs of stabilisation between the 134.80 (R1) resistance line and the 131.40 (S1) support line. Given that the USD/JPY’s price action has broken the downward trendline guiding it we switch our bearish outlook initially for a sideways movement bias, yet also note that the RSI indicator remains near the reading of 30, implying that there is still a bearish effect in the market sentiment that could drive the pair lower. Should a selling interest be expressed we may see the pair breaking the 131.40 (S1) support line while should the buyers be in charge, we may see the pair breaking the 134.80 (R1) resistance line and aim for the 138.15 (R2) level.

Other highlights for the day:

We would also like to note UK’s ILO unemployment rate and average weekly earnings for January and employment change for February alongside Canada’s manufacturing sales for January. Also during tomorrow’s Asian session we note, BOJ’s meeting minutes for January and China’s industrial output and retail sales for February.

USD/JPY H4 Chart

Support: 131.40 (S1), 128.60 (S2), 126.35 (S3)

Resistance: 134.80 (R1), 138.15 (R2), 140.60 (R3)

GBP/USD H4 Chart

Support: 1.2115 (S1), 1.1925 (S2), 1.1740 (S3)

Resistance: 1.2270 (R1), 1.2465 (R2), 1.2660 (R3)

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

إخلاء المسؤولية:

لا تُعد هذه المعلومات نصيحة استثمارية أو توصية بالاستثمار، وإنما تُعد تواصلاً تسويقيًا. لا تتحمل IronFX أي مسؤولية عن أي بيانات أو معلومات مقدمة من أطراف ثالثة تم الإشارة إليها أو الارتباط بها في هذا التواصل.