With the banking sector under threat and an eventful week slowly drawing to a close we have a look at what next week has in store for the markets. On the monetary front, we highlight the release of the Fed’s interest rate decision on Wednesday as well as BoE’s interest rate decision on Thursday. Also, we note the interest rate decisions of SNB, CBT and Norgesbank on Thursday, while RBA is to release the minutes of its last meeting in Tuesday’s Asian session. As for financial releases we make a start with New Zealand’s trade data for February in Tuesday’s Asian session and continue in the European session with Germany’s ZEW indicators for March, while later on, we get Canada’s retail sales for January and CPI rates for February. On Wednesday we get from the UK the CPI rates for February and the CBI indicators for trends in industrial orders for March while on Thursday we note the release of the weekly US initial jobless claims figure and Eurozone’s preliminary consumer confidence for March. On Friday we note March’s preliminary PMI figures for Australia, Japan, Germany, France, the Eurozone as a whole, the UK and the US while we also note the release of Japan’s CPI rates for February, UK’s retail sales for February as well as the US durable goods orders growth rates for the same month.

USD – Fed’s interest rate decision in focus

The USD is about to end the week slightly lower against its counterparts after a turbulent week. We make a start with the end of last week as Silicon Valley Bank (SVB) crashed causing the USD to lose ground, a tendency which was maintained also on Monday. Yet the decisive steps taken by the Fed seemed to reverse market sentiment, while on Wednesday the transferring of the banking crisis to Europe with Credit Suisse being in the epicenter tended to provide safe haven inflows for the greenback. It should be noted that the USD was on the rise on Thursday despite February’s retail sales growth rate slowing down, as did also the PPI rate for the same month. The main release though of the week may have been February’s CPI rates which failed though to provide a substantial market reaction as they slowed down at a headline level as expected. Nevertheless, the combination of the SVB fallout with the slowing of the headline CPI rates tended to increase the pressure on the Fed to ease its aggressive hawkish approach. The situation now culminates in the Fed’s meeting on Wednesday and its interest rate decision. The market expects the bank to proceed with another 25 basis points rate hike and currently, Fed Fund Futures (FFF) imply a probability of almost 83% for such a scenario to materialise, with the other 17% suggesting that the bank may remain on hold at 4.75%. It’s characteristic of the shift in the market opinion that in the last week, we were discussing the possibility of a 50

basis points rate hike. Yet market attention is expected to also fall on the forward guidance which is to be included in the accompanying statement. Should the bank maintain its confident and aggressively hawkish tone, we may see the USD getting some support as the market’s expectations for the bank to remain on hold and cut rates in Q3, could be shaken and the market will have to reposition itself. Yet to that end also the new dot plot is to be closely watched in order to see, at which level Fed policymakers see the terminal rate and in which time frame. Also the bank’s projections are expected to be closely watched, especially if the bank sees the possibility of the US economy entering a recession. Last but not least, we highlight also Fed Chairman Powell’s press conference later on, as he could sway the market’s opinion. Please note that the Fed and its Chairman in particular seem to be under intense criticism for a lax approach regarding the supervision of commercial banks and some politicians even clearly stated that the Fed was to blame for the fallout of SVB.

GBP – BoE to remain on hold?

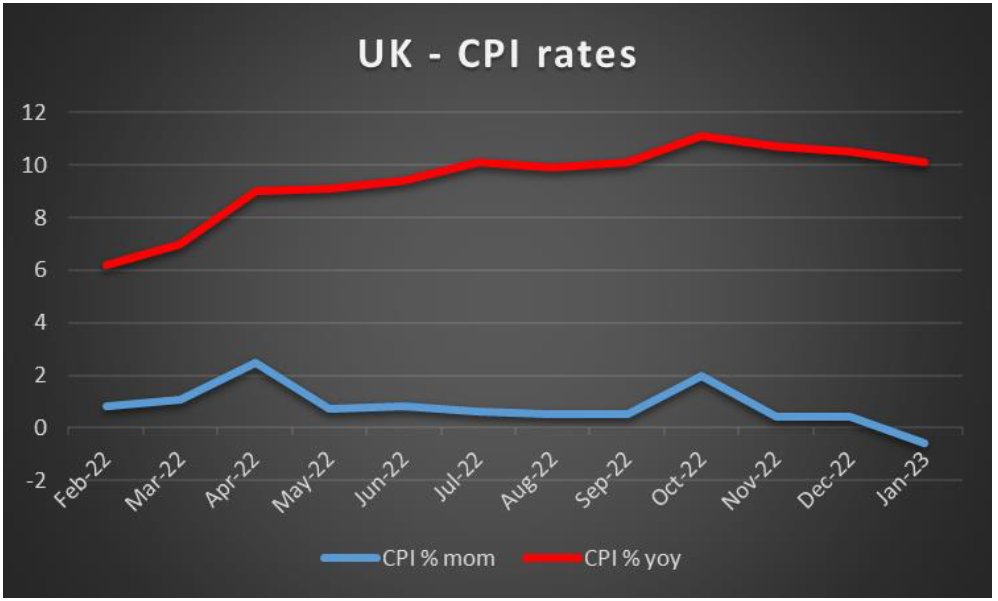

The pound is about to end the week slightly higher against the USD, remains relatively unchanged against the JPY and is clearly gaining for the week against the common currency. On a more fundamental level, we would like to note the optimistic note provided by UK’s finance minister Jeremy Hunt, during the presentation of the spring budget, that the UK economy may be able to avoid a recession this year, which was a breath of fresh air contrasting the pessimistic mood characterizing analysts for the UK economy. On a macro level, we note that the UK employment data for January were better than expected showing a relative tightness of the UK employment market. Exactly this tightness of the UK employment market in combination with the CPI rates is closely watched by BoE in determining its steps ahead. It should be noted that the bank hinted that the bank rate may be nearing its peak. The comment tended to inflate market expectations that the bank may be considering remaining on hold in its next meeting. It’s characteristic that GBP OIS on Thursday, showed a split 50-50 probability between the possibility of the bank hiking rates by 25 basis points and remaining on hold. In any case, the market expects the bank to hike rates by 25 points only one more time whether that is to be in the meeting next or the next one in May and then remain on hold up until the end of the year. Should the bank actually proceed with a 25 basis points rate hike we may see the pound getting some support while failure of the bank to raise its interest rate may result in a weakening of the pound. Also a possible forward guidance implying that the bank has reached its terminal rate or is near, may turn an interest rate hike to a dovish hike and actually weaken the pound. Also we highlight the release of the UK CPI rates for February on Wednesday. Should the headline rates accelerate, we may see the pressure on BoE to hike rates growing while a possible easing of inflationary pressures may also ease the pressure on BoE.

JPY – CPI rates at the end of the week

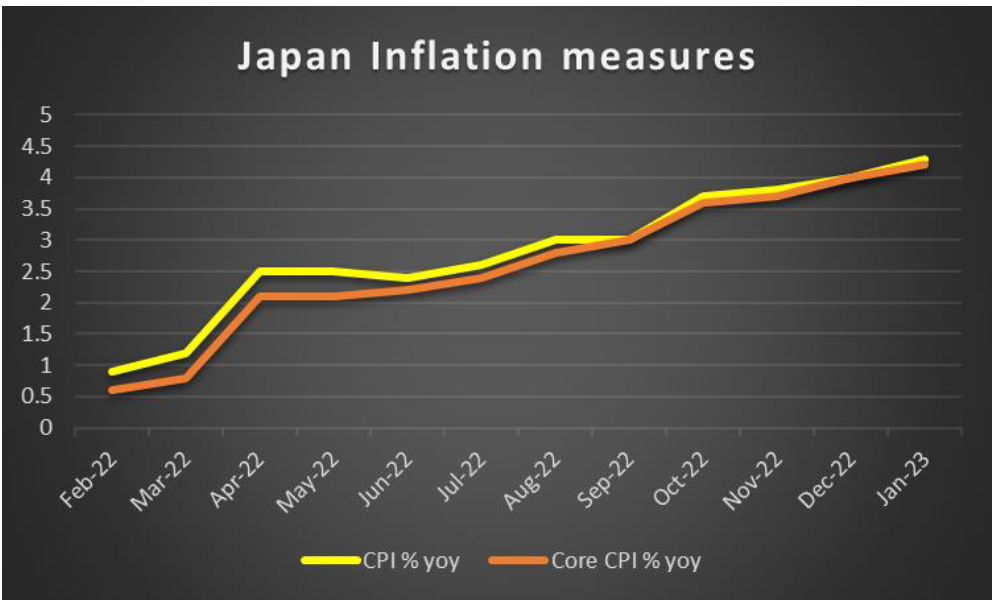

JPY is about to end the week higher against the USD, EUR and GBP in a sign of broader strength for the Japanese currency. It should be noted that on a fundamental level, the reflexes of JPY’s second nature as a safe haven were activated in the past week as the banking crisis in the US and Europe tended to alarm traders. Should that be the case in the coming week as well and should market worries start easing we may see the Japanese currency slipping and vice versa. Also on a political level, we note the improvement of the Japanese-South Korean relationships, while we also note the firing of long-range missiles for N. Korea ahead of the meeting of the heads of the two prementioned states. On a monetary level, it should be noted that BoJ remained in an ultra-loose monetary policy mode, defending the correctness of the policy over the past years. It was characteristic that even on Thursday’s Asian session outgoing BoJ Governor Kuroda defended the bank’s dovish policy as he was reported stating that “the Bank has enacted an effective and sustainable policy”. Overall the bank’s dovish policy tends to be a drag of JPY, given that widening monetary policy differentials with other central banks are weighing on the Japanese currency. Mr. Kuroda is to leave office on the 8th of April, yet we have doubts that his successor, Mr. Ueda is about to radically change the bank’s general direction, in the short term at least. On a macroeconomic level, we highlight the release of Japan’s CPI rates for February on Friday next week and a possible acceleration of the rates could enhance the pressure on BoJ to at least tweak its ultra-loose monetary policy. Also, we would note the wide acceleration of the machinery orders growth rate for January implying a greater degree of confidence on behalf of Japanese companies to actually invest in the economy, while the narrowing of the trade deficit for February tended to imply that the Japanese economy suffered less from its international trading transactions. Both releases were noted as positives for JPY.

EUR – March’s preliminary PMIs center stage

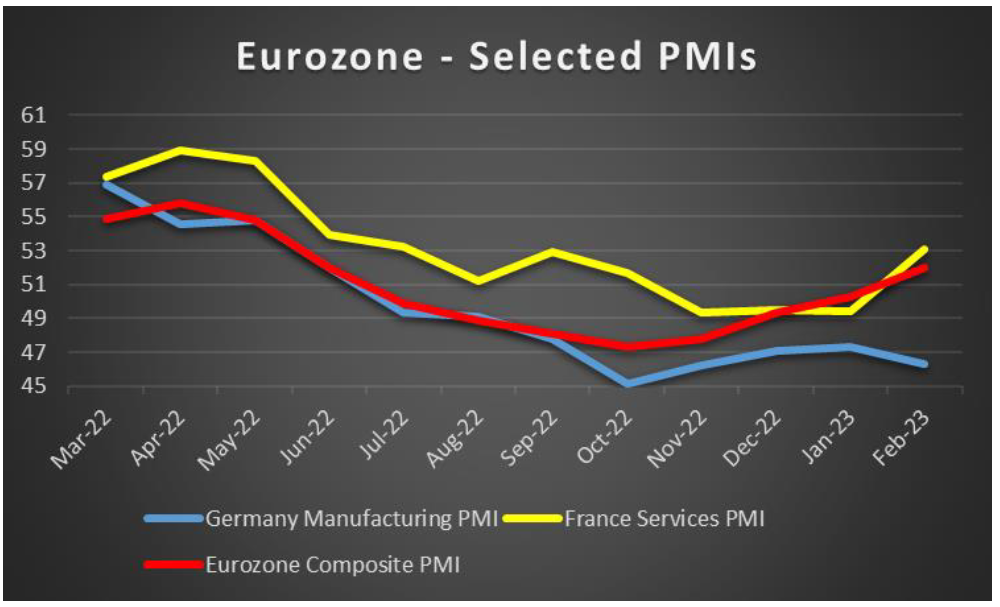

The euro ended the week lower against the USD but also against the GBP and JPY in a sign of a broader weakness. It should be noted that the EUR was weakened on a fundamental level, by the unfolding banking mini-crisis with Credit Suisse on Wednesday. Yet the assistance provided by SNB to the Swiss bank of about $54 billion, tended to avert market worries for a possible overspill also to European systemic banks such as Deutsche bank. On a monetary level, we note ECB’s interest rate decision to hike rates by 50 basis points despite risking overstraining trading conditions for a sensitive banking sector. Yet the bank’s interest rate decision was on the one hand accompanied also by a statement on behalf of the ECB to provide liquidity if and to the degree needed. Also, the rate hike was accompanied by a certain degree of uncertainty about the bank’s future moves. In contrast to the February meeting which explicitly stated that the bank planned to proceed with a 50 basis points rate hike, today’s forward guidance highlighted the need for the bank to preserve a data-dependent case-by-case approach, given the relative uncertainty surrounding Eurozone’s financial environment. It should be noted that the acceleration of the HICP rates for Germany, France and Spain showcased that inflationary pressures remain strong and increased the pressure on the bank to proceed with more rate hikes on Thursday. For the time being, we note that the market seems to be timidly pricing-in a 25 basis points rate hike for the bank’s May meeting. On a more macroeconomic level, we note the Eurozone’s industrial production growth rate for January, accelerated beyond expectations sending a positive note for economic activity in the trading bloc. Yet in the coming week a more decisive and fresher indication is to be released as the preliminary PMI figures for March are due out on Friday.

AUD – Fundamentals to take over

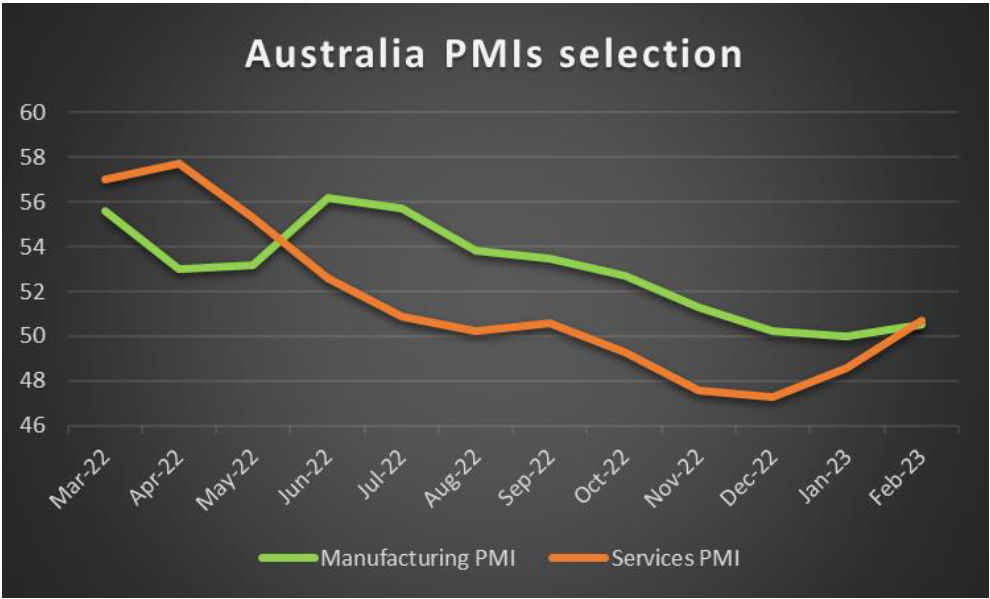

AUD seems about to end the week slightly higher against the USD. On the monetary front, we note that market expectations for RBA to remain on hold seem to be weighing on the Aussie, given also the fallout of SVB, yet Australia’s central bank may be focusing mostly on the domestic data to make its decisions. We highlight the tight employment market of Australia given the better-than-expected unemployment rate and employment change figure, for February. Exactly the tightness of the employment market could be one of the factors boosting RBA’s ahead of the bank’s interest rate decision early in April. On the other hand, business confidence and

business conditions seem to have deteriorated a bit in February. On the other hand, Chinese data showed that economic activity growth rates for February in the industrial sector accelerated, yet were below market expectations, while the urban investment and retail sales growth rates for the same month were also in the greens. Overall, it seems that the Chinese industrial sector got off with a good reopening and is supported also by strong internal demand, which may act as a pillar for the continuance of growth in the Chinese economy and Aussie traders are to keep a close eye on developments as improvement of economic activity in China could imply a greater degree of exports of Australian raw materials. Overall though given the lack of high-impact financial releases we expect fundamentals to be in the driver’s seat regarding the Aussie’s direction in the coming week. Any possible deterioration of the US-Sino relationships could weigh on the Aussie given Australia’s close economic ties to China. Should the overall market sentiment turn more risk-averse we may see AUD slipping as it is considered a higher-risk trading instrument given its second nature as a commodity currency and vice versa.

CAD – Inflation data to swing the Loonie

The CAD is about to end the week slightly stronger against the USD. On a macroeconomic level, we note that Canada’s employment data for February were better than expected as the employment change figure dropped yet not as much as expected and the unemployment rate managed to remain unchanged at 5.0%, one of the lowest levels, for a third consecutive month. We also note that the House starts for the same month increased showing increased economic activity for the Canadian construction sector. The string of positive news for the past few days was completed by the acceleration for both the manufacturing and the wholesale sales growth rates, both being for January. The better-than-expected data mentioned, could provide support for BoC’s confidence, yet any hawkish move seems to be out of the picture for the bank currently. On the contrary, the uncertainty created by the SVB fallout tends to raise some dovish concerns about a possible ripple effect on the Canadian economy and thus is advising caution. We intend to keep a close eye on the release of Canada’s CPI rates next week and a possible slowdown of the rates implying also an easing of inflationary pressures in the Canadian economy may enhance voices requesting a rate cut yet we tend to maintain rather solid expectations for the bank to remain on hold at 4.5% in its mid-April meeting. Also on a more fundamental level, we would like to note the wide drop of oil prices over the past few days which may have prevented the CAD from making further gains against the USD. It should be noted that the uncertainty created by the shaky banking sector tended also to undermine market expectations for oil demand and should oil prices continue to drop or even remain on rather low levels we may see it weighing on the Loonie as well, given that Canada is a major oil producing country and the CAD is considered as having a positive correlation with oil prices.

General Comment

As a closing comment we note that we leave behind us a turbulent week where the markets neared the possibility of a meltdown, yet for the time being the worst seems to have been avoided. Nevertheless, we still consider the situation as fragile and the possibility of deterioration cannot be excluded. In the coming week, we may see the USD maintaining the initiative over other currencies in the FX market, given that the Fed’s interest rate decision bears still some degree of uncertainty and the stakes are high. Yet at certain points during the week, there are opportunities available for other currencies to shine as well allowing for a nice blend of trading opportunities. We would like to make a small comment though also for the interest rate decisions mentioned earlier. In Switzerland, SNB is expected by the market to hike rates again by 25 basis points despite the recent turmoil created in the banking sector by Credit Suisse. Given that inflationary pressures have been on the rise in the land of the Alps, such a move could be understood as inflation is above target and rising and thus a rate hike could provide further support for the Swiss Franc. Further to the south, in Turkey, the Turkish central bank, CBT is expected by a number of analysts to remain on hold at 8.5% given that the bank had proceeded with a 50 basis points rate cut in the February meeting and inflation despite being at high levels of 55% yoy seems to be easing over the past four months. Nevertheless, we would not exclude the possibility of another 50 basis points rate cut which could weigh on the Turkish Lira. Last but not least let’s not forget that at the northern tip of Europe, some analysts expect Norgesbank to remain on hold at 2.75% after consecutive hikes up until December and standing pat in January. Yet in the last meeting the bank stated that future developments will depend on economic developments and inflation seems to remain stubbornly high hence a 25 basis points rate hike may be warranted and Norgesbank Governor Ida Wolden Bache’s comments that “the policy rate will most likely be raised in March” tends to highlight this scenario, which may provide some support for the NOK.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

إخلاء المسؤولية:

لا تُعد هذه المعلومات نصيحة استثمارية أو توصية بالاستثمار، وإنما تُعد تواصلاً تسويقيًا. لا تتحمل IronFX أي مسؤولية عن أي بيانات أو معلومات مقدمة من أطراف ثالثة تم الإشارة إليها أو الارتباط بها في هذا التواصل.