US stock markets have reversed their trajectory over the past week, retracing to lower ground, as market optimism of a positive earnings season has diminished, following heightened recession fears. In this report we aim to present the recent fundamental and economic news releases that impacted the US stock markets, look ahead at the upcoming events that could affect their performance and conclude with a technical analysis.

US stock markets trade lower following heightened recession fears

Equity markets traded lower following last week’s mixed US financial releases. The Philly Fed Manufacturing Index was indicative of a slowdown in the U.S economy, as the actual figure came in much lower than anticipated, heightening fears of a potential recession. On the other hand, the release of the S&P Manufacturing Index on Friday provided a contradicting view, as the better-than-expected figures downplayed the risks of a recession. The PMI figures, may have provided further support for the Fed to maintain its aggressive interest rate policy, as was the comments by New York Fed President Williams, who stated last Thursday that “inflation is still too high, and we will use our monetary policy tools to restore price stability”. The implications of the Fed continuing its aggressive rate hiking path, could therefore provide further support to the greenback, at expense of the equities market. On the other hand, the equities markets posted greater than expected earnings so far, indicative of a resilient market, keeping equities afloat near their recent two-month highs. Furthermore, Philadelphia Fed President Harker stated that “the Fed is close to where it needs to be on interest rates”, thus contradicting New York Fed President Williams by implying that the Fed may be near or reaching its terminal rate. Philly Fed President Harker’s dovish statement, in combination with the better-than-expected earnings so far, may have mitigated outflows stemming from a stronger greenback. However, the market sentiment rapidly deteriorated on Tuesday following the announcement by First Republic that the bank had experienced a withdrawal of $100 bn in deposits. The unexpected announcement sent shockwaves across the industry, as it renewed fears of another bailout by the FDIC of yet another troubled bank. Due to the heightened banking fears, the equity markets’ sentiment deteriorated, leading to outflows as traders fear that the true impact of interest rates on the banking market is yet to be seen. Lastly, we would also like to make a comment about the US GDP for Q1 and Core PCE rates that are due on Friday. Should the figures further highlight an imminent recession risk, then we may see further deterioration in the equities market, whereas on the other hand, should the data point out expansionary signs, we may see the markets bounce back and erase the losses incurred by the negative sentiment generated in the past week.

The earnings season rollercoaster continues

The Equities season appeared to be gaining traction since last week as high-profile companies were posting greater than expected earnings such as Coca Cola (#KO), Procter & Gamble (#PG), American Express (#AMEX), Microsoft (#MSFT), Google (#GOOGL), Visa (#Visa), Pepsico (#PepsiCo) and 3M(#MMM) tended to boost the equities market. However, as was mentioned in last week’s report, the cracks have resurfaced, with regional banks suffering the brunt impact from last month’s mini banking crisis, coinciding with the Fed’s assessment in last week’s Beige book, which noted that banks, tightened lending standards amid increased uncertainty and concerns about liquidity. On another note, 3M(#MMM), announced on Tuesday that they would be reducing their employee headcount by 6,000. The employee reduction announcement may be a continuation of the restructuring plan by the company, aiming to reduce annual costs by approximately $900 million, which further highlights the company’s commitment at implementing cost cutting measures, to ensure a healthier balance sheet, despite a better-than-expected earnings results. Overall, equities traders may find that the short-term support in the market stemming from positive earnings was rather short-lived, following the bombshell by First Republic. As such we note that despite companies posting better than expected earnings, the bar was set pretty low following the mini-banking crisis and as such does not necessarily mean that equities markets are in the clear.

التحليل الفني

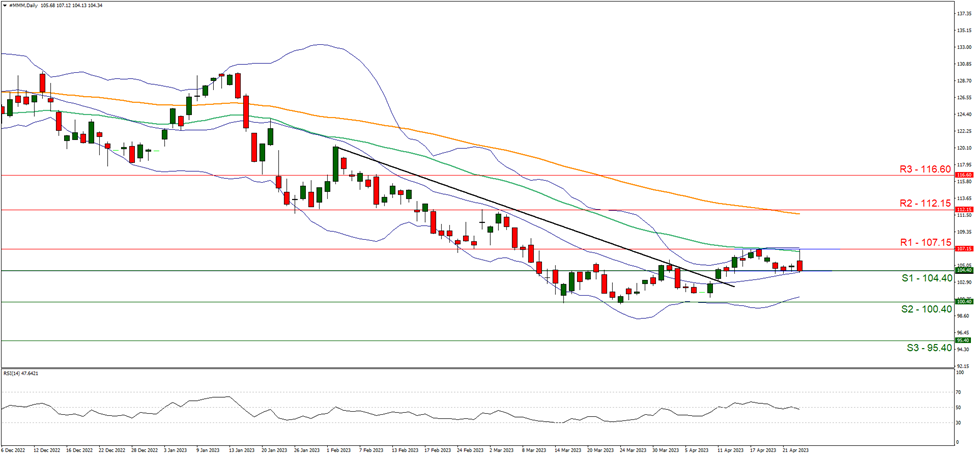

#MMM Daily Chart

Support: 104.40 (S1), 100.40 (S2), 95.40 (S3)

Resistance: 107.15 (R1), 112.15 (R2), 116.60 (R3)

Looking at #MMM Daily chart we observe investors remaining on edge following First Republic’s announcement yesterday, despite a better-than-expected earnings report by 3M. We hold a neutral outlook for 3M should the price action remain between the 104.40 (S1) support and the 107.15 (R1) resistance levels. Supporting our case is the RSI indicator below our daily chart which currently stands near 50 and the formation of a sideways channel since the 12th of April, indicative of indecision surrounding the stock. For a bullish outlook, we would like to see a clear break above the 107.15 (R1) resistance line with the next potential target for the bulls being the 112.15 (R2) resistance barrier. For a bearish outlook we would like to see a clear break below the 104.40 (S1) support level, with the next possible target for the bears being the 100.40 (S2) support line.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

إخلاء المسؤولية:

لا تُعد هذه المعلومات نصيحة استثمارية أو توصية بالاستثمار، وإنما تُعد تواصلاً تسويقيًا. لا تتحمل IronFX أي مسؤولية عن أي بيانات أو معلومات مقدمة من أطراف ثالثة تم الإشارة إليها أو الارتباط بها في هذا التواصل.