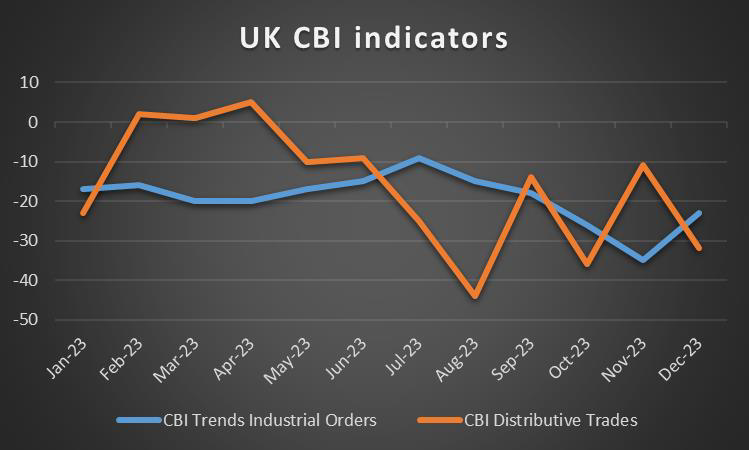

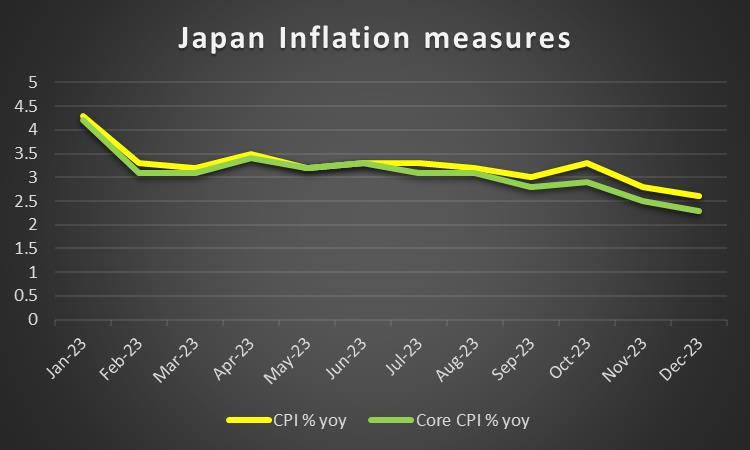

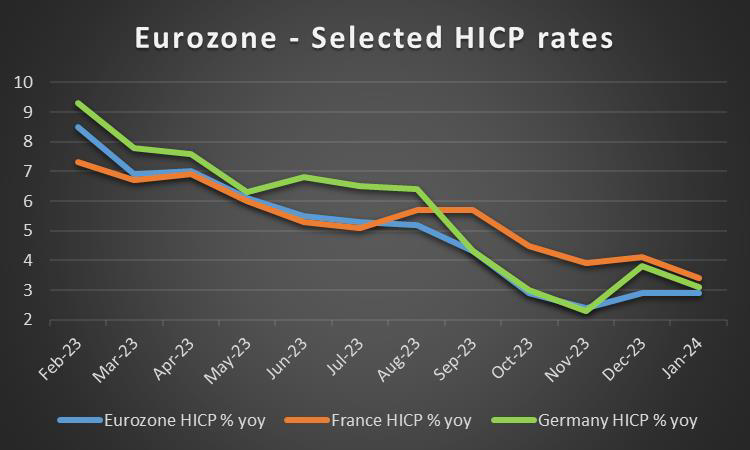

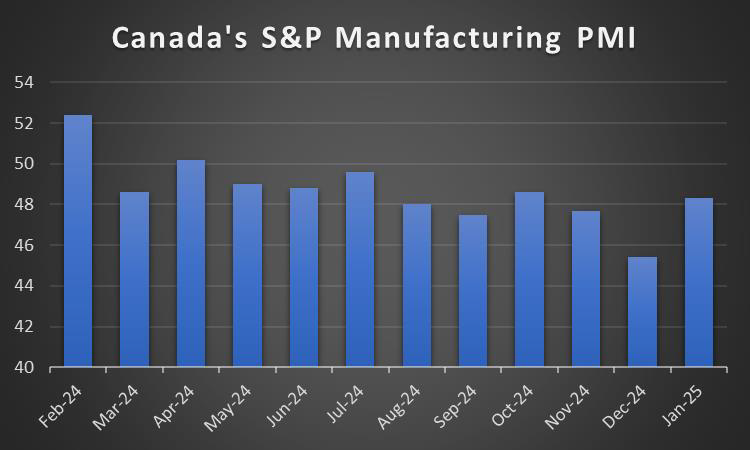

The week is about to draw to a close and we open a window at what next week has in store for the markets. On the monetary front, a number of policymakers from various central banks are scheduled to speak throughout the week and could sway the market’s mood, yet we note from New Zealand, the interest rate decision of RBNZ on Wednesday’s Asian session. As for financial releases, we make a start on a slow Monday, when we get UK’s CBI distributive trades for February, while on Tuesday we note Japan’s CPI rates for January, Germany’s consumer confidence for March and the US durable goods. On Wednesday, we get Australia’s CPI rates for January, Eurozone’s economic sentiment for February and we highlight the release of the revised US GDP rate for Q4. In a packed Thursday, we get Japan’s preliminary industrial output for January, Australia’s CAPEX rate for Q4, and retail sales for January, Turkey’s, Sweden’s, France’s and Switzerland’s GDP rates for Q4, while we also note France’s and Germany’s preliminary HICP rates for February, Switzerland’s KOF indicator for February, Canada’s business barometer for the same month and from the US the consumption rate and Core Price index both being for January. Finally, on Friday, we note the release of China’s manufacturing PMI figures for February, the Czech Republic’s final GDP rates for Q4, Eurozone’s preliminary HICP rates, Canada’s S&P manufacturing PMI figure, the US ISM Manufacturing PMI figure and the US final University of Michigan consumer sentiment, all being for February.

USD – Revised US GDP rates eyed

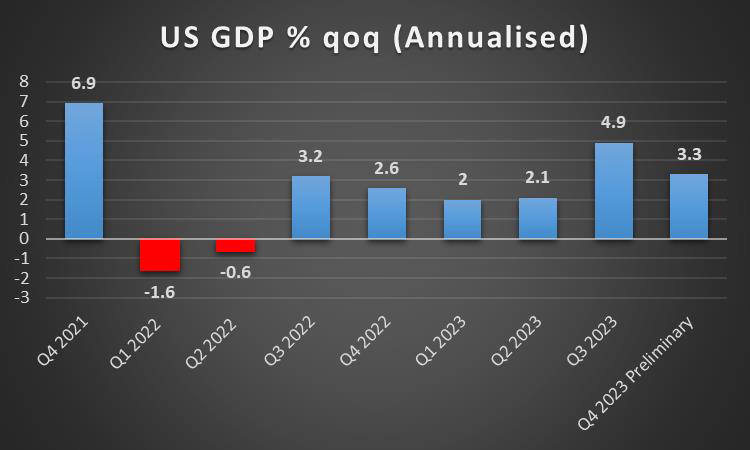

The USD is about to end the week a tad bit lower against its counterparts breaking a six-week winning streak. On a fundamental level, we note the release of the Fed’s January meeting minutes. The bank in its minutes displayed a hesitation to proceed with rate cuts, contradicting the market sentiment yet, failing to excite the markets. It should be noted that the markets’ expectations continue to shift, aligning with the Fed’s narrative of fewer rate cuts and currently FFF imply that the 1market expects the bank to cut rates three maybe four times next year, starting from July onwards. A continuance of the Fed’s narrative for a slower easing of its monetary policy may provide some support for the USD in the coming week on a monetary level. On a fundamental level, the pre-election period in the US and the tensions between Washington and Moscow on an international level, seem to be preoccupying the markets, yet with little effect until now. On a macroeconomic level, we note an easing in the expansion of economic activity in both the manufacturing and services sector according to the preliminary S&P PMI figures for February, which could be expected, the figures as such are still pretty good if compared to other developed economies. On a macro level, in the coming week we expect market focus to be placed on the revised GDP rate for Q4, and should the rate accelerate if compared to the preliminary release the narrative of the Fed for a soft landing could be enhanced and support the USD.

GBP – Fundamentals to lead

The pound seems about to end the week in the greens against the USD and the JPY, but is stable against the EUR. On a macroeconomic level, we note that economic activity in the UK seems to have expanded at a faster pace in the past month with the services sector being the main engine behind it. On the other hand the market worries tend to remain for the UK manufacturing sector given the narrowed yet still wide pessimism of UK industrialists in the current month, and the contraction of economic activity in February according to the preliminary PMI figure for February. In the coming week, given the lack of releases of high-impact financial data from the UK. On a monetary level, we note the readiness of BoE to proceed with rate cuts even before the CPI rates drop below the bank’s target of 2% yoy, something that was mentioned by BoE Governor Andrew Bailey, before UK lawmakers. Should there be additional signals from Boe policymakers that an easing of monetary policy is nearing, we may see the pound weakening as it could force the pound traders to reposition themselves. For the time being, we note that the market expects the bank to start cutting rates in August and deliver three rate cuts in total within the year. On a fundamental level, we note that the pound remained relatively unimpressed by the widest monthly budget surplus as announced by UK’s finance minister Jeremy Hunt, yet still counts as a plus for the UK economy. The budget surplus may allow the UK finance minister to announce tax cuts in the near future, which in turn may provide some support for the pound.

JPY – CPI rates in focus

JPY seems about to end the week lower against the relatively weak USD and is also losing ground against the EUR and GBP, in a sign of wider weakness. We note that on a macroeconomic level, we note that the acceleration of the machinery orders growth rate for December, implied an increased trust on behalf of Japanese businesses in the outlook of the Japanese economy, yet on the other hand the wide trade deficit underscored how wealth escaped the Japanese economy from its international trading transactions. Furthermore, the wider contraction of economic activity in the crucial Japanese manufacturing sector for February tended to darken the outlook of the Japanese economy. In the coming week, we highlight the release of the headline and core CPI rates for January and a possible continuation of the easing of inflationary pressures in the Japanese economy, may weigh on the JPY as the expectations for a normalization of BoJ’s ultra-loose monetary policy will be contradicted. The bank is expected by the market to hike rates for the first time in decades, in April and the bank to continue and deliver another two rate hikes by the year’s end. Yet such a scenario does not seem to be providing support for JPY at the current stage. Practically the bank seems to be between the hammer and the anvil, on the one hand it is pressured to normalise its monetary policy by hiking rates, as it is considered the main factor behind the weak yen, given interest rate differentials with other central banks, and on the other hand, the bank’s policymakers do not seem to be convinced that inflation is high in a sustainable manner. On a fundamental level, we note JPY’s dual nature as a national currency and a safe haven instrument and should we see a more risk on market approach, we may see the Yen suffering outflows. Yet we note that JPY remains in relatively very low levels, hence another market intervention by Japan to the Yen’s rescue cannot be excluded.

EUR – Inflation measures to move the EUR

The EUR seems able to gain against the USD and JPY for the week, yet remains stable against the pound. On a macroeconomic level, we note that the Eurozone as a whole was able to narrow the contraction of economic activity across sectors. Yet, Germany’s manufacturing sector seems to have suffered a widened contraction of economic activity in February, which tends to maintain the worries for a possible recession in the Eurozone afloat. Also, the acceleration of the HICP rate for January was practically confirmed despite a tick down if compared to the preliminary release, which in turn tends to maintain the pressure on the ECB to delay any possible rate cuts. For the time being, we note that the market seems to be pricing in the bank to deliver its first rate cut in June and hike rates three times in total within the year, which seems a bit realistic as the worries for a possible recession in the Eurozone may be adding pressure on the bank to ease its tight monetary policy. Yet some of the bank’s policymakers seem to be in now rush to start cutting rates and it’s characteristic that Governing Council member Pierre Wunsch implied that the market may be getting ahead of itself. On a fundamental level, Trump’s statements for NATO and Putin tended to rattle Europeans yet seemed to have little effect on the market. The war in Ukraine seems to be weighing in Putin’s favor, also posing another question for the Eurozone’s post-war relationship with Russia, yet in our opinion, it’s too early to worry about this scenario. In the coming week, we expect the highlight for EUR traders to be the release of February’s preliminary HICP rate and a possible slowdown may ease market worries for inflation in the Eurozone and allow the common currency to slip, yet even a slight acceleration may take the markets by surprise, intensify market worries for a prolongment of the ECB’s tight monetary policy and may provide asymmetric support for the common currency.

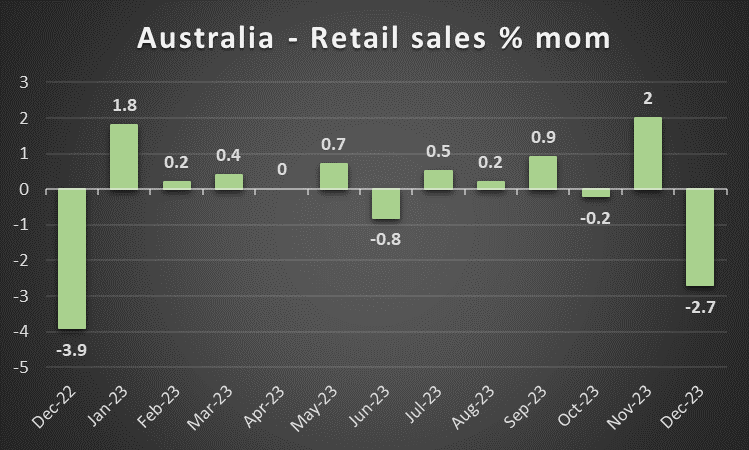

AUD – CPI, CapEx and retail sales

AUD is about to end the week stronger against the USD for the third week in a row. On a fundamental level, we note that the Aussie’s commodity currency nature tends to make it sensitive to the market sentiment, hence should the market sentiment remain positive, we may see the Aussie being supported and vice versa. Yet no fundamentals regarding AUD would be complete without a reference to the situation in China, given the close Sino-Australian economic ties. For the time being, we note the difficulties faced by China in its efforts to regenerate its economy. In the coming week, we note the release of China’s NBS and Caixin manufacturing PMI figures for February on Friday and should the indicators continue to signal that Chinese factories are struggling to increase economic activity, we may see the Aussie weakening. On a monetary level, we note the release of RBA’s February meeting minutes. In the document, the bank appears to have considered two possibilities, with one being to remain on hold and the other being a potential 25 basis point rate hike. The consideration by the bank to potentially raise rates by 25 basis points, implies that the bank may have not reached its terminal rate. As such, the possibility of the bank raising rates in the future could potentially provide support for the Aussie in the long run. On a macroeconomic level, we note the acceleration of the wage prices index for Q4, which may imply that the labor market may continue feeding inflationary pressures in the Australian economy, while for next week, we highlight the release of the CPI rates for January and a possible acceleration may add more pressure on RBA to remain hawkish, thus supporting the Aussie. In a similar manner, a possible acceleration of the retail sales growth rate for January may imply that consumption in the Australian economy has not been curbed adding inflationary pressures.

CAD – GDP rates to move the Loonie

The Loonie is about to end the week near the same levels as it began against the weakening USD, implying also a weakness on behalf of CAD. On a fundamental level, we note the sensitivity of the CAD to the market sentiment as a commodity currency and the improved market sentiment may have been among the few factors supporting the CAD this week. Also, the positive correlation of the CAD with oil prices cannot be neglected, given Canada’s status as a major oil-producing economy. Oil prices this week tended to remain rather stable amidst conflicting fundamentals, failing to support the CAD. Yet should market worries for a tight supply side of the oil market intensify in the coming week, we may see the CAD getting some support as well. On a monetary level, we note the market’s expectations for the BoC to start cutting rates in June and proceed with three rate cuts in the year. It’s characteristic that economists in Canada, now are expecting the bank to start stopping its quantitative tightening earlier than initially anticipated, in an additional sign of monetary policy easing. Should there be more signals in that direction we may see them weighing on the Loonie. On a macroeconomic level, we note the slowdown of CPI rates both on a core and headline level in January. The slowdown brought the CPI rates in the upper level, but within the bank’s inflation target of 2%±1% and tends to intensify market expectations for a possible earlier rate cut thus weighing on the Loonie. In the coming week, we switch our focus from inflation to growth and highlight the release of the GDP rate for Q4. We note that should the recession characterizing Canada’s economy deepen even further, we may see the release weighing on the CAD.

General Comment

Overall in the coming week in the FX market, we expect volatility to be maintained yet may become more versatile, as high-impact financial releases are stemming from various economies. On the other hand, US stock markets rallied yesterday with all three main stock market indexes, namely the Dow Jones, Nasdaq and S&P 500, uniformly rising and reaching record high levels. The rally was at least partially underpinned by NVIDIA’s meteoric rise yesterday after the better-than-expected readings in its Q4 earnings report. Should the positive market sentiment be maintained we may see US stock markets being supported. Also, note that the earnings season seems to be drawing to a close, which may ease market interest in US stock markets somewhat. Furthermore, also gold’s price seems to have stabilized after two weeks of consecutive losses. It should be noted that on the one side, the relative inactivity of the USD tended to support gold prices, yet on the flip side the rise of US yields tended to weigh on the precious metal’s price. Last but not least a small comment for New Zealand’s RBNZ interest rate decision. The market has priced in the bank remaining on hold at 5.5% by 69.6% currently, according to NZD OIS, with rest implying that a rate hike is also possible.

There seem to be some hawkish expectations in the market for the bank, hence should the bank actually remain on hold as expected, we would turn our attention towards the accompanying statement and a possible less hawkish tone than what the market expects could disappoint traders and thus weaken the Kiwi.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

إخلاء المسؤولية:

لا تُعد هذه المعلومات نصيحة استثمارية أو توصية بالاستثمار، وإنما تُعد تواصلاً تسويقيًا. لا تتحمل IronFX أي مسؤولية عن أي بيانات أو معلومات مقدمة من أطراف ثالثة تم الإشارة إليها أو الارتباط بها في هذا التواصل.